111 NE 1st ST

Miami, Florida 33132

USA

Is the Buy Now, Pay Later (BNPL) industry the future of consumer finance?

BNPL has experienced explosive growth in recent years, and its global transaction volume is projected to reach $680 billion by 2025.

This surge is fueled by younger consumers seeking flexible payment options and merchants aiming to boost sales.

Our exploration of BNPL statistics and trends answers this question, offering insights into this transformative finance development that redefines spending behaviors across generations.

Data Sources and Methodology

This article compiles verified studies to provide a comprehensive overview of the BNPL statistics. Our research process includes:

Data Collection:

- Primary sources: Industry surveys, government databases

- Secondary sources: Academic publications, reputable industry reports

- Time frame: Data collected spans from 2022 to 2032

Key Data Providers:

Analysis Approach:

- Cross-referencing multiple sources to ensure accuracy

- Prioritizing the most recent data available

- Applying relevant analysis techniques, e.g., trend analysis, comparative analysis

Limitations:

- Market dynamics in BNPL can shift rapidly; readers should consider the publication date of this article.

We strive for accuracy and transparency in our reporting.

However, some data points may have changed since publication.

Key Takeaway

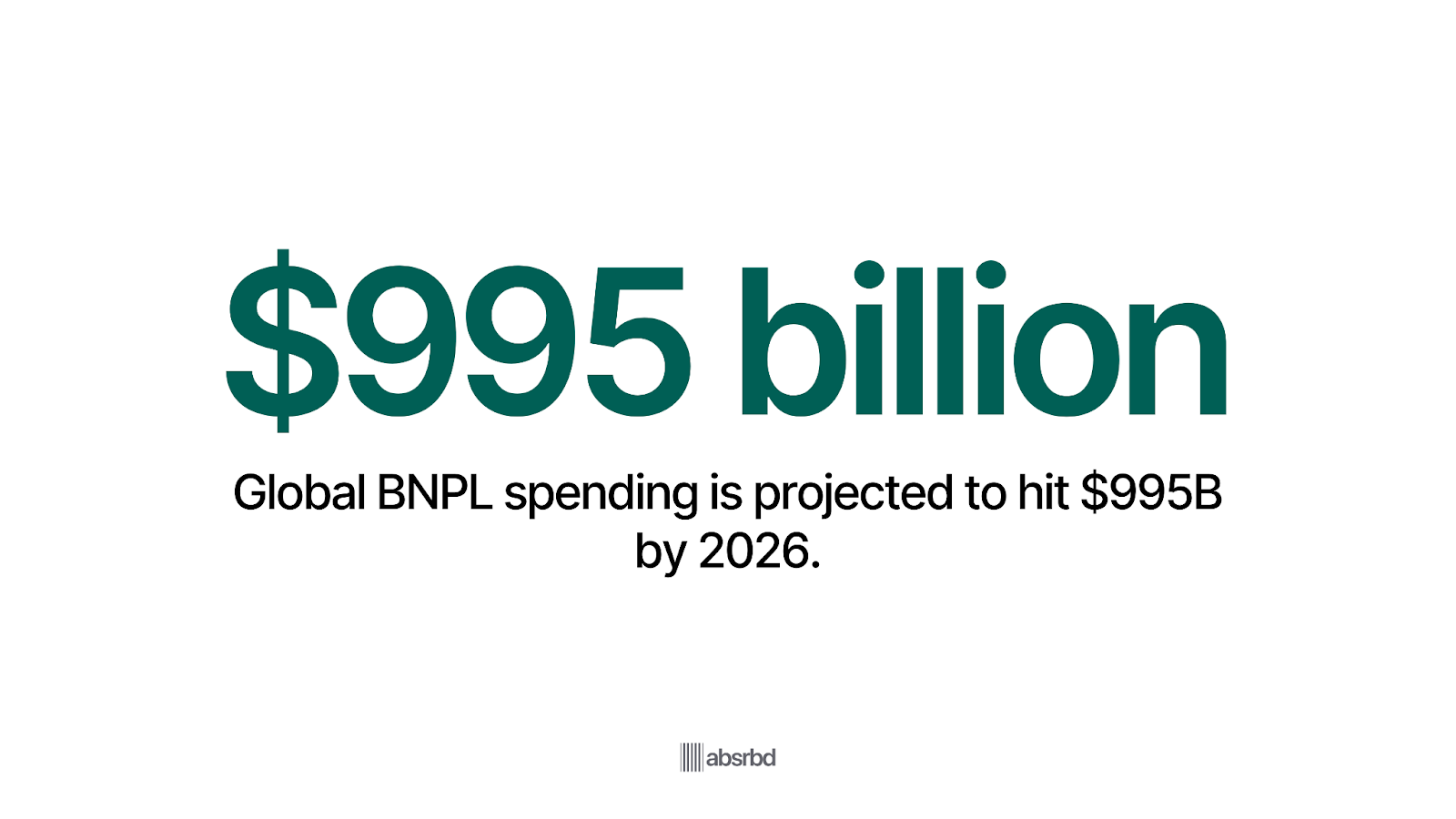

- Global BNPL spending is on track to hit USD 995 billion in 2026, redefining digital credit.

- BNPL transaction value will exceed USD 565 billion by 2026, nearly doubling since 2023.

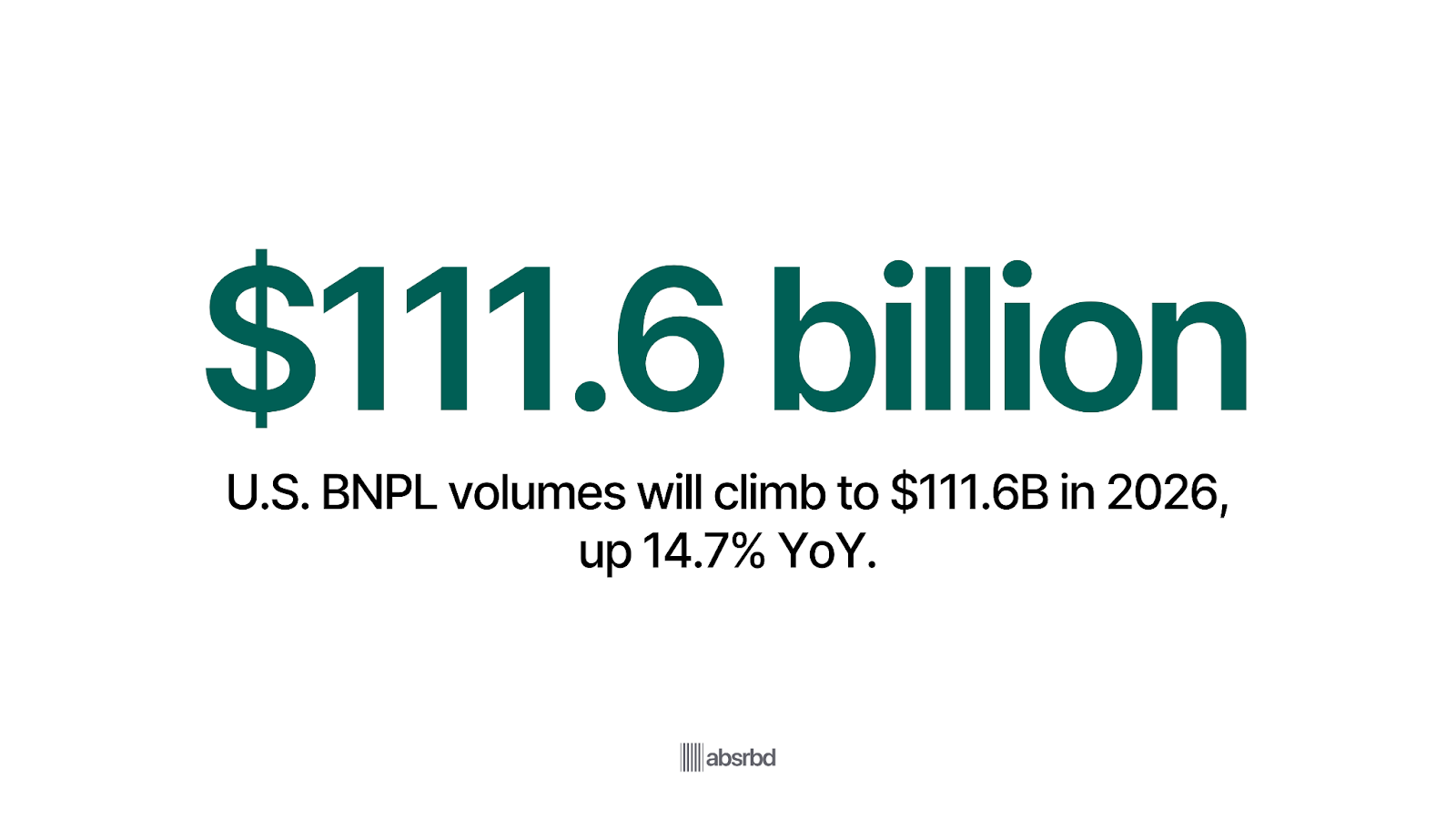

- The U.S. BNPL market is set to reach USD 111.6 billion, up more than 14% year on year.

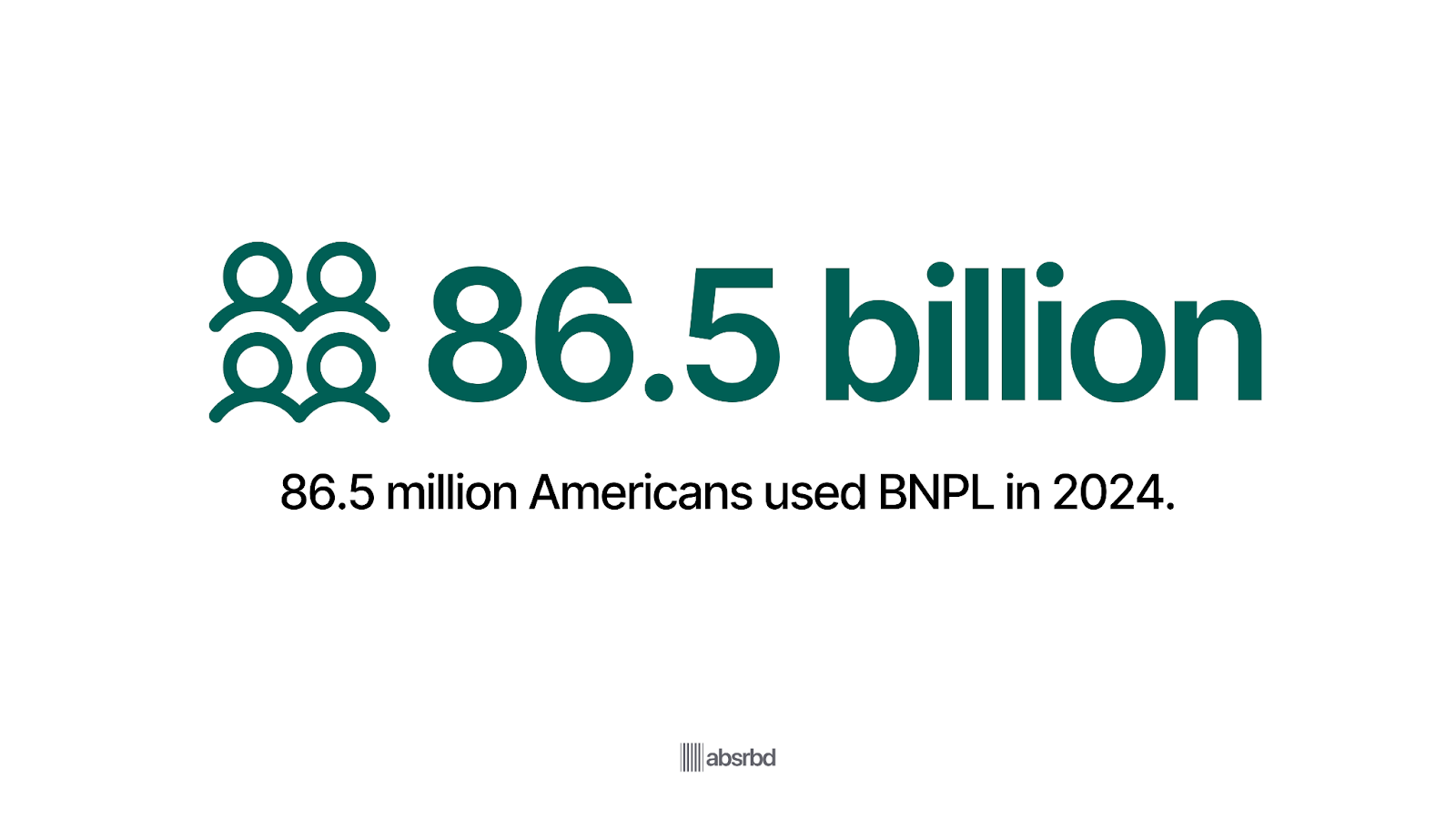

- Over 86 million Americans now use BNPL, making it a mainstream payment choice.

- BNPL already powers one in every twenty global e-commerce transactions.

- Nearly four in ten BNPL users missed at least one payment last year, signaling mounting financial strain.

- BNPL adoption among older adults in the UK has doubled, proving it’s not just for Gen Z.

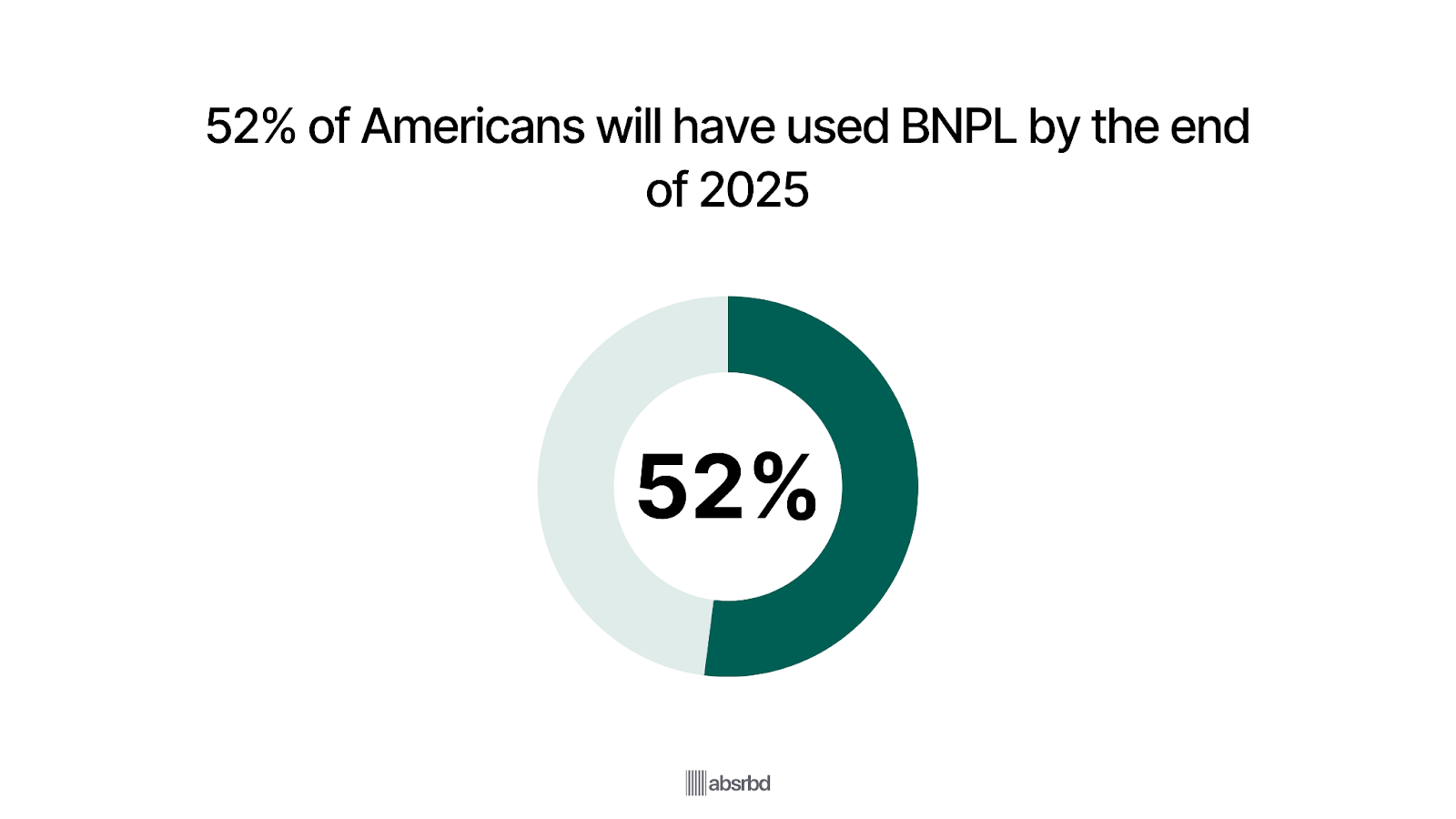

- More than half of U.S. consumers will have used BNPL by the end of 2025.

- Over 2 billion BNPL transactions took place globally in 2023 — and the pace is still accelerating.

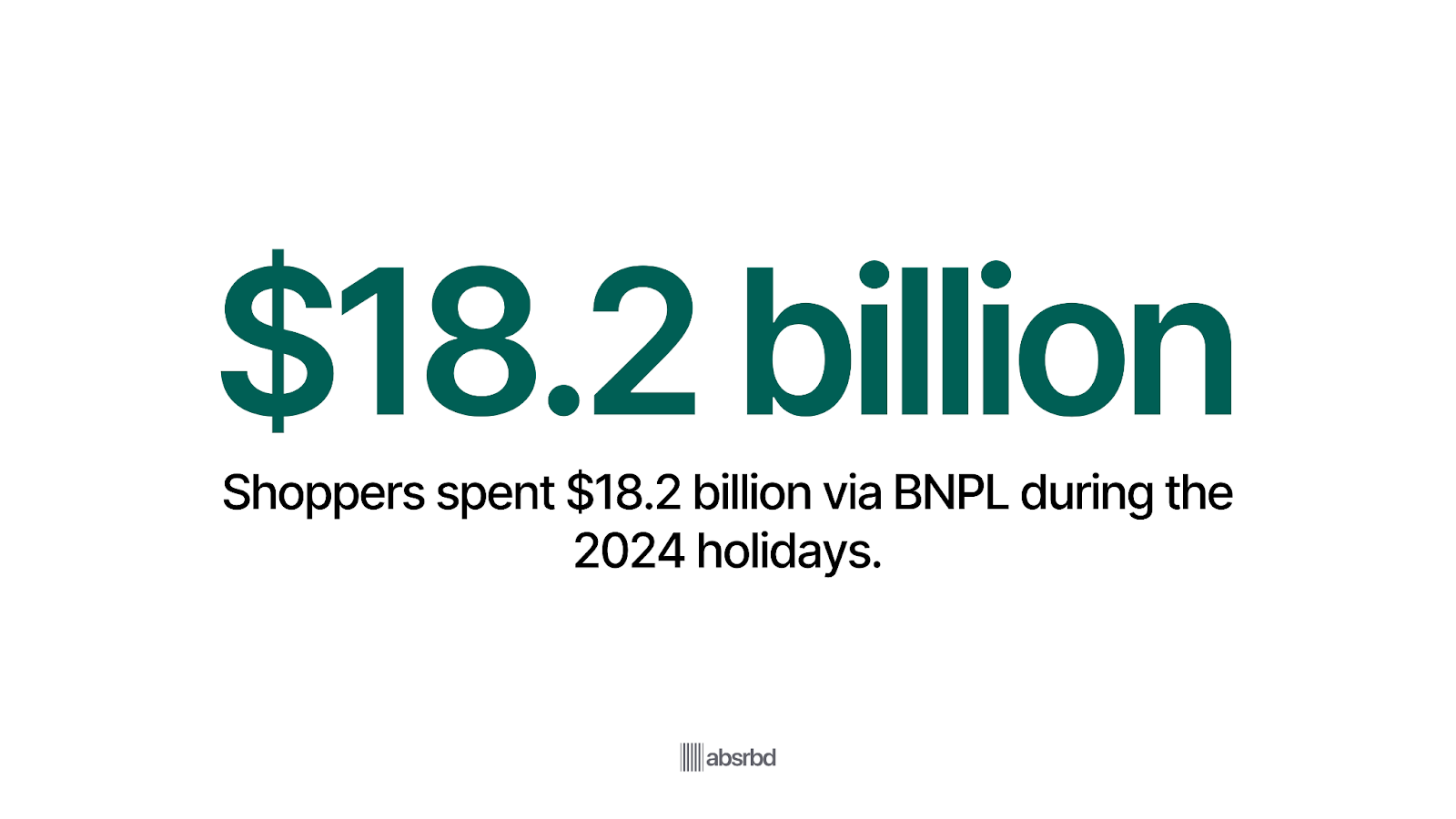

- BNPL drove USD 18.2 billion in holiday sales in 2024, shaping how people shop seasonally.

Overview of BNPL

Buy Now, Pay Later BNPL isn’t new, installment plans have existed for decades, but the modern digital model took shape in the mid-2010s, led by players like Klarna, Afterpay, and Affirm.

The concept surged globally between 2019 and 2021, driven by the e-commerce boom and consumer demand for flexible, interest-free payments.

In 2026, BNPL is changing how consumers pay, making it easier to manage purchases through smaller, scheduled payments. The model now spans retail, travel, healthcare, and everyday spending, with major banks and payment networks entering the space.

Global BNPL spending is projected to grow to USD 995 billion by 2026 Payments Dive, while total transaction value will reach USD 565.8 billion Doofinder.

In the U.S. alone, BNPL volume is forecast to hit USD 111.6 billion in 2026 Oberlo. Usage is rising globally: over 86 million U.S. consumers used BNPL in 2024, and adoption is expected to grow steadily through 2026 Digital Silk.

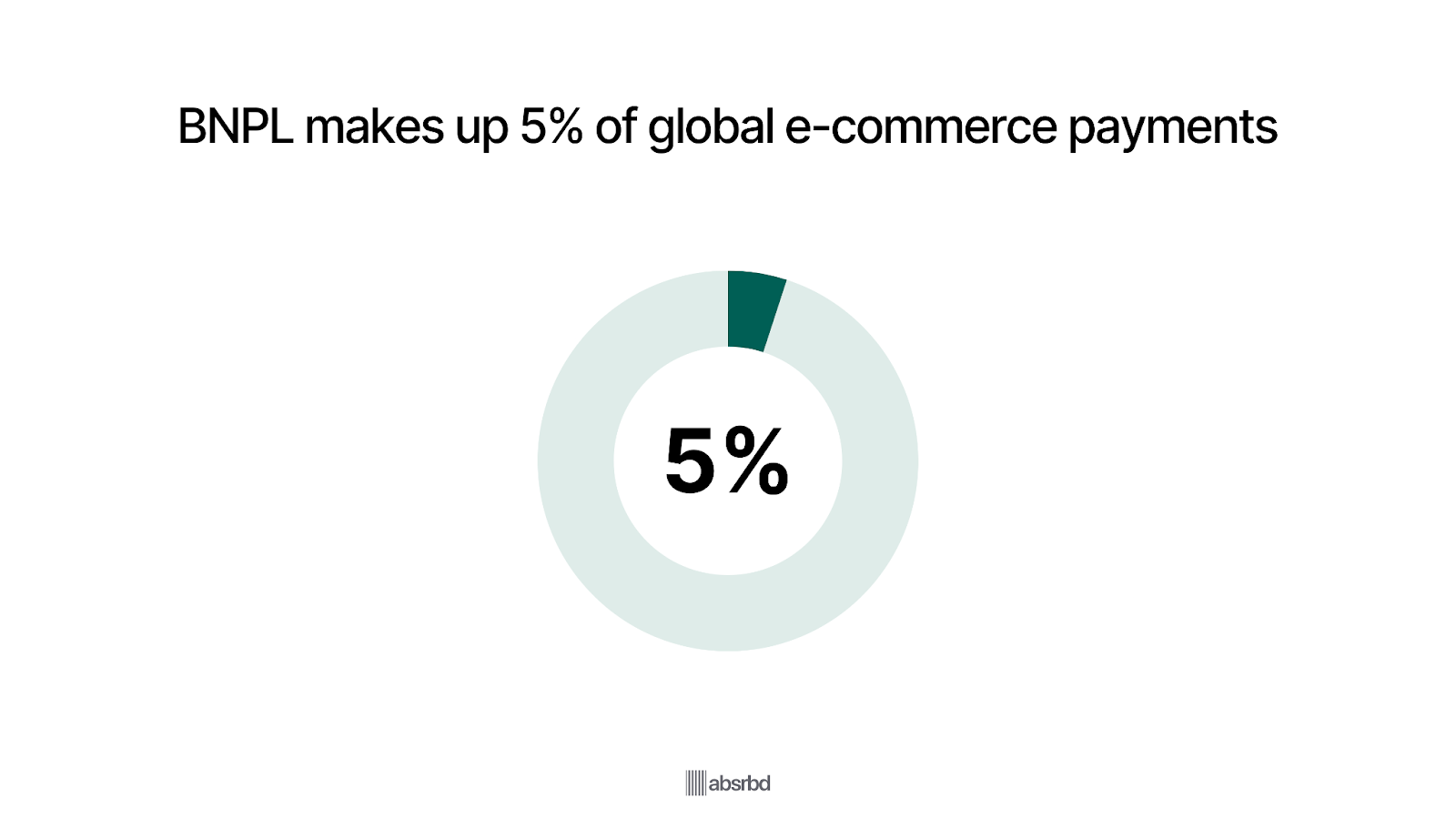

Worldwide, BNPL already represents about 5% of all e-commerce transactions.

Key Statistics

- The global BNPL transaction value is projected to hit USD 656.34 billion in 2026. GlobeNewswire

- Another source estimates global BNPL spending at USD 995 billion by 2026. Juniper research

- In the United States, total BNPL payment volumes are forecast to reach USD 111.6 billion in 2026, reflecting a growth rate of 14.7% year-on-year. Oberlo

- The BNPL market reached USD 340 billion globally in 2024. Digital Silk

- In 2024, 86.5 million Americans used BNPL services. Digital Silk

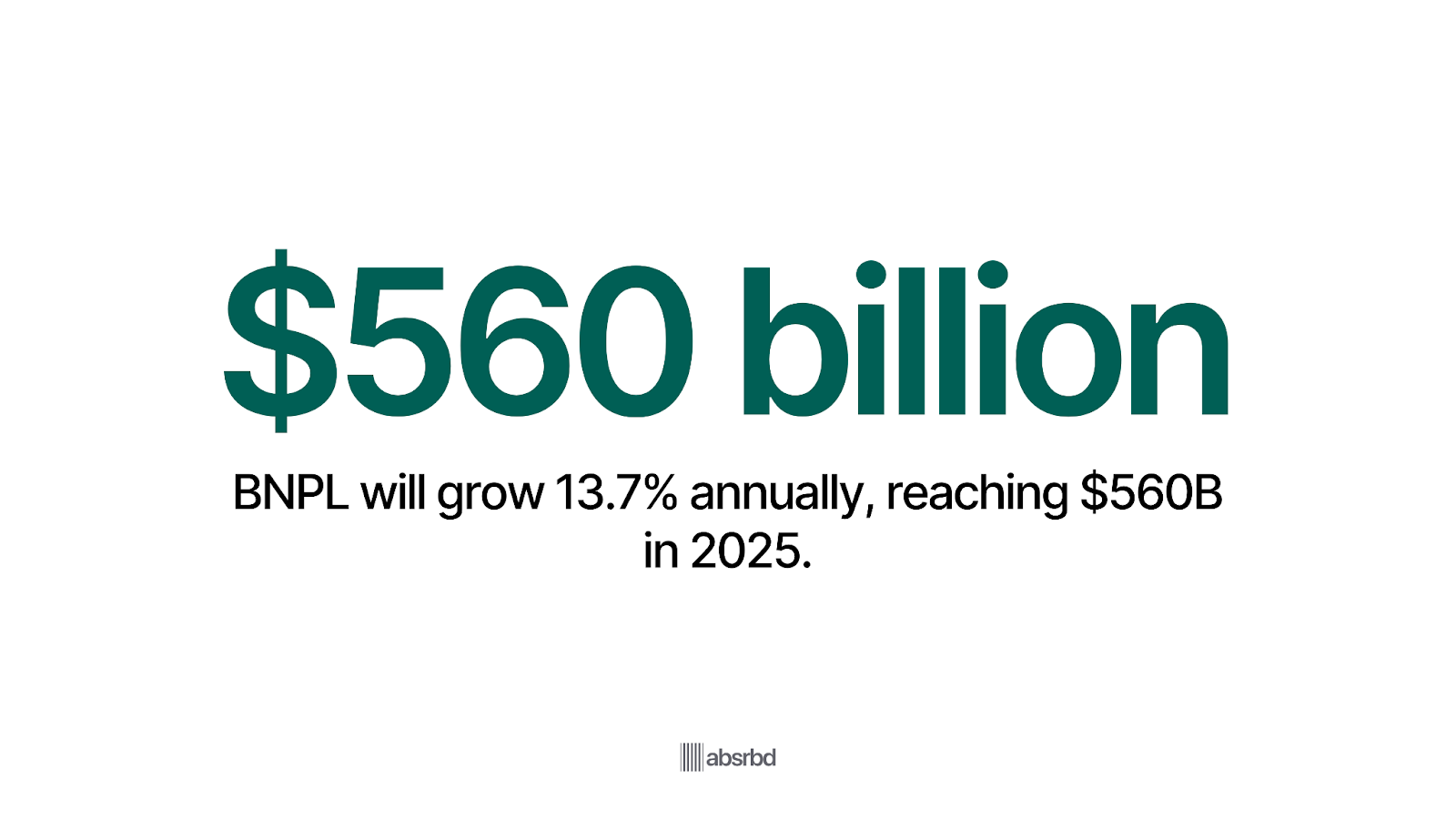

- The global BNPL market is projected to grow 13.7% annually to USD 560.1 billion in 2025. FinTech Futures

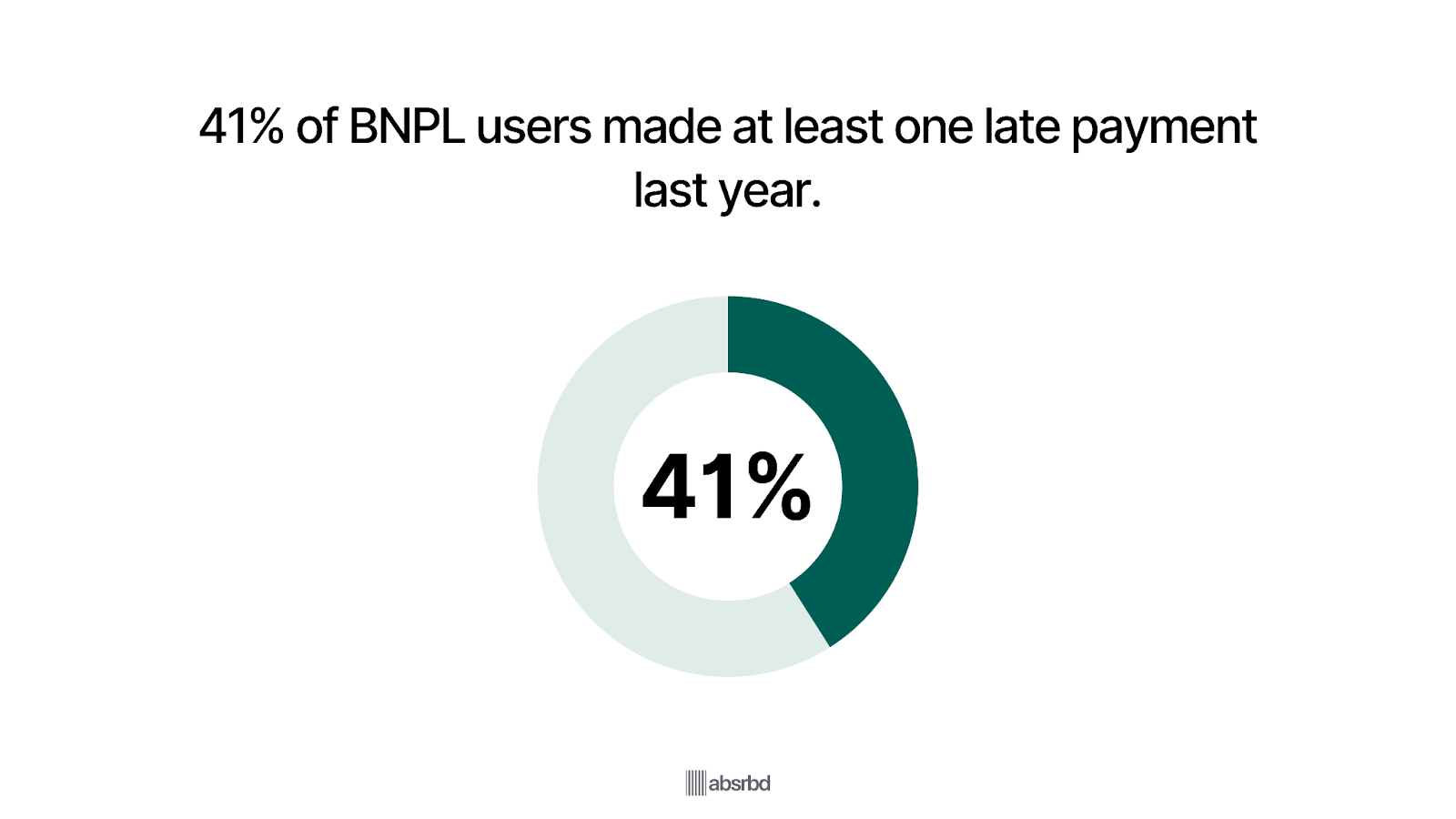

- More than 41% of BNPL users say they made at least one late payment in the past year. LendingTree

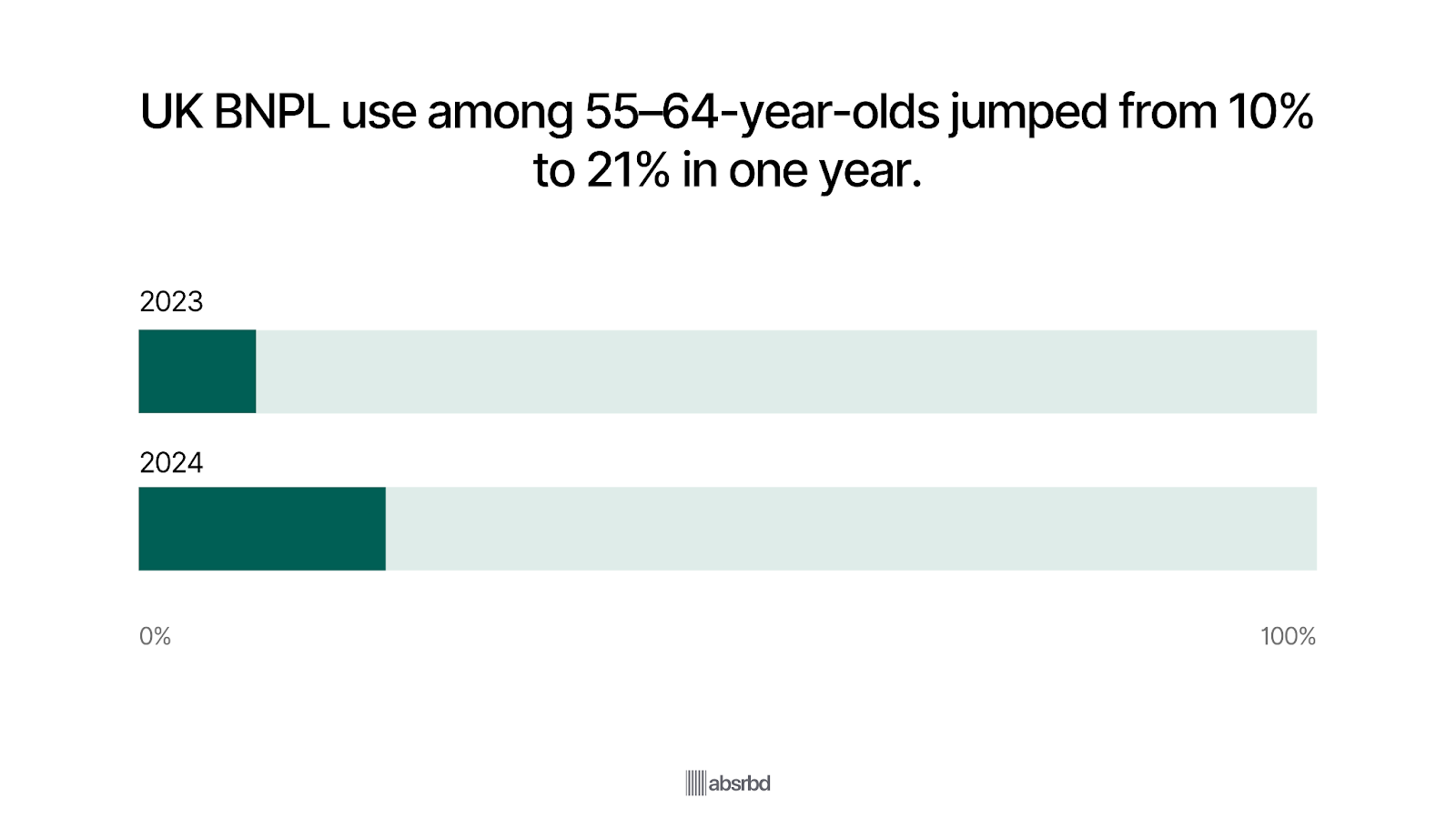

- In the UK, BNPL usage among 55–64 year-olds more than doubled from 10% in 2023 to 21% in 2024. The Guardian

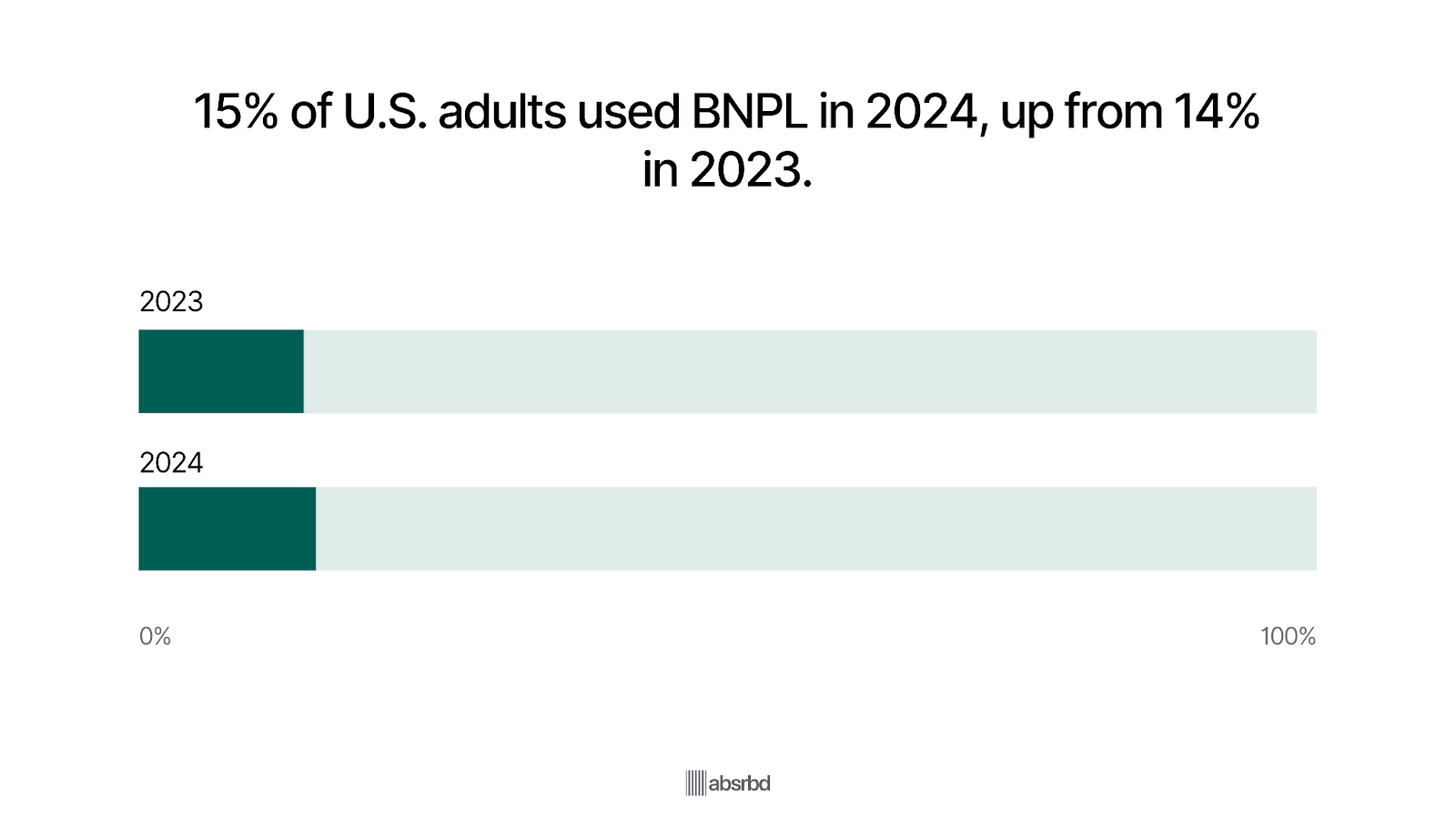

- In the U.S., 15% of adults used BNPL in 2024, up from 14% in 2023. The Motley Fool

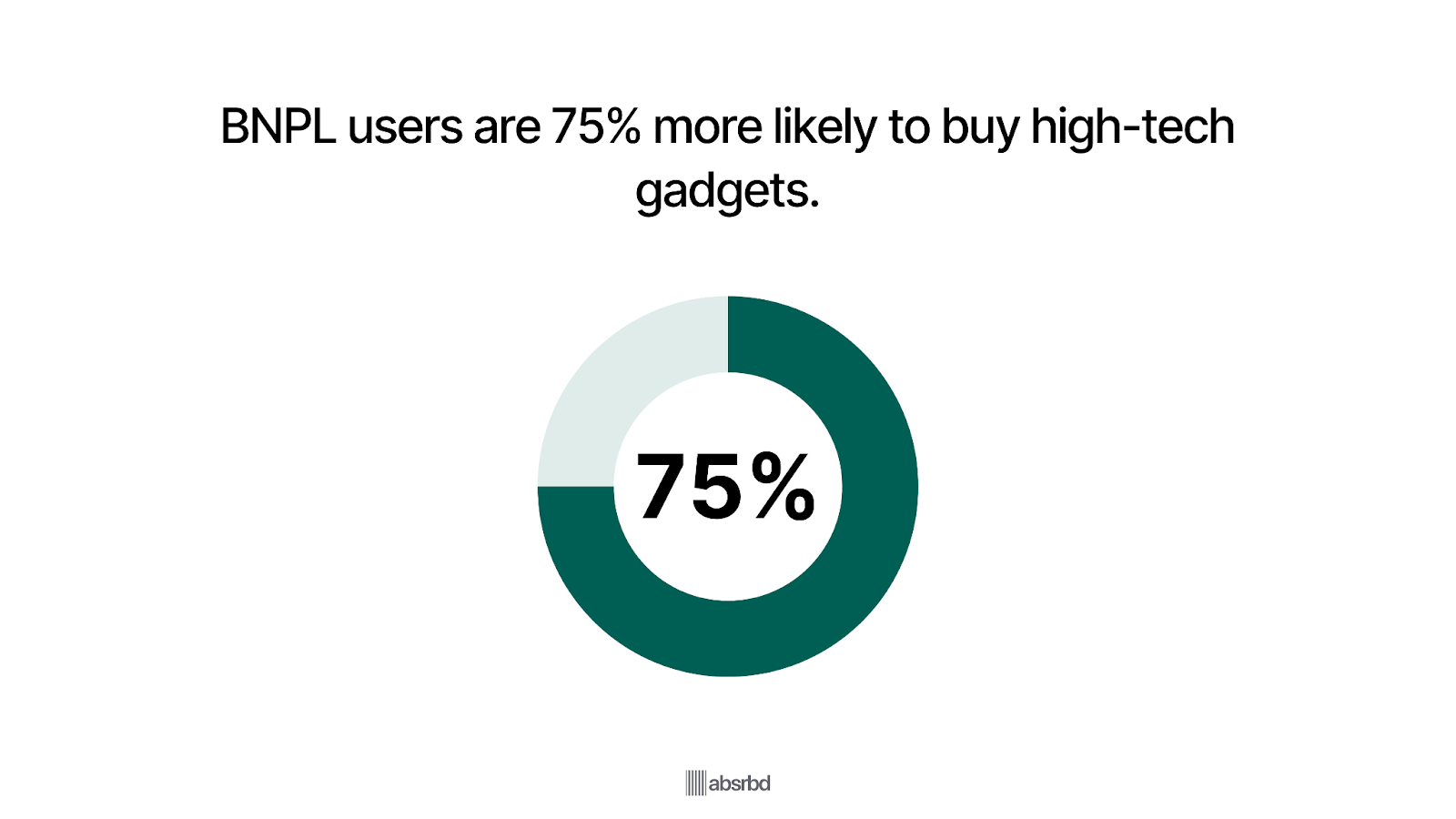

- BNPL users are 75% more likely than average to purchase tech gadgets like drones or robot vacuums. GWI

- The BNPL payment share in global e-commerce payments reached 5% in 2024. Digital Silk

- In 2024, shoppers spent USD 18.2 billion via BNPL during the holiday season. Digital Silk

- The U.S. BNPL market is expected to cross USD 124.82 billion by 2027. Oberlo

- In the U.S., 52% of consumers are projected to have used BNPL at least once by the end of 2025. CoinLaw

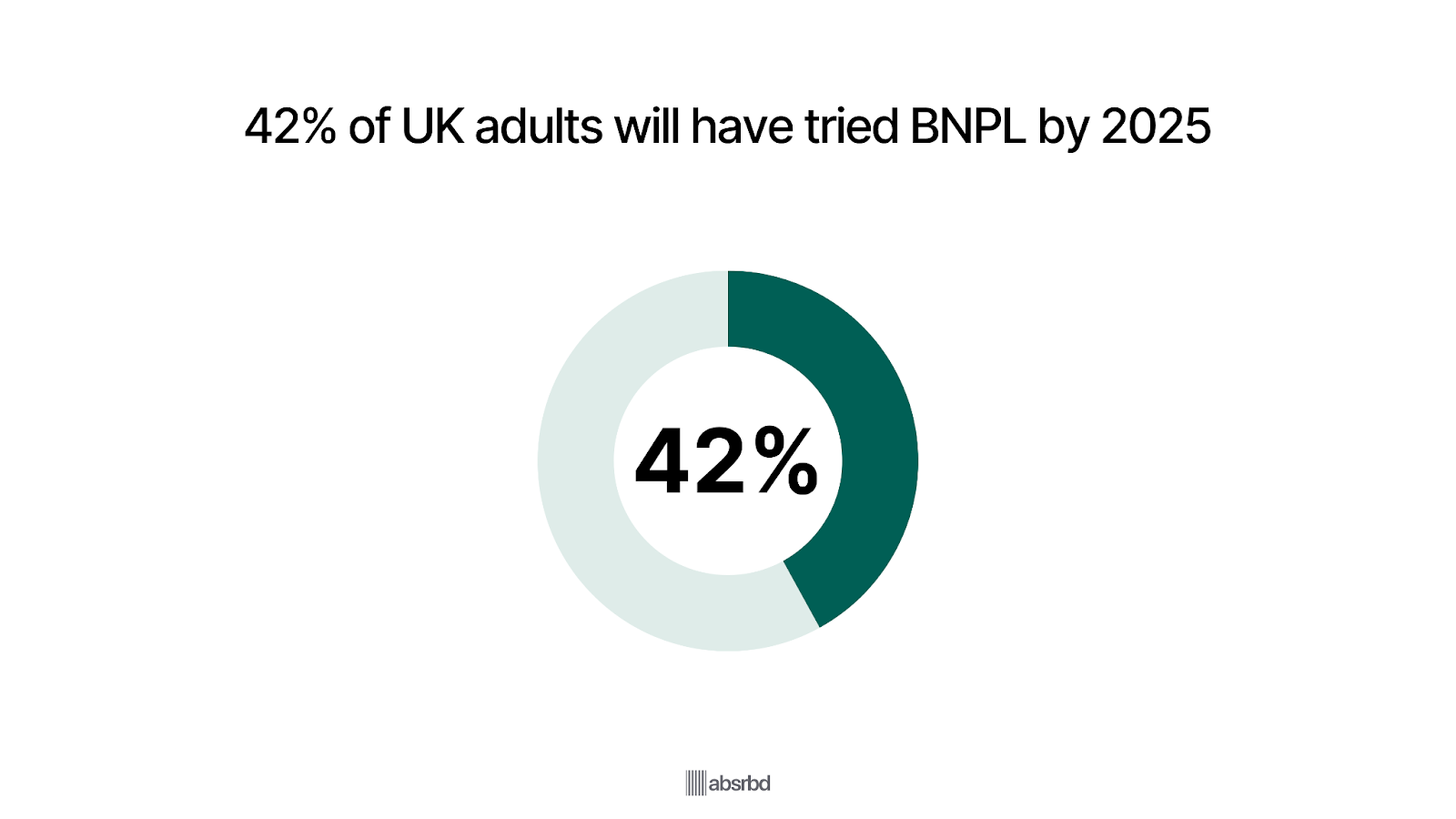

- In the UK, 42% of adults will have used BNPL in 2025. CoinLaw

- In Australia, 37% of people used BNPL for online purchases in 2025, up 11% YoY. CoinLaw

- More than 2 billion BNPL transactions were recorded globally in 2023. Allianz Trade Corporate

Major Trends in BNPL

Several key trends are reshaping the BNPL landscape and influencing its future direction.

Global BNPL Transaction Value Projected at USD 565.8 Billion in 2026

Analysts forecast that the BNPL market will grow from USD 481 billion in 2025 to USD 565.8 billion in 2026, expanding into verticals like healthcare, travel, and education. Doofinder

This expansion underscores that BNPL is no longer confined to retail goods but is evolving into a broader consumer credit mechanism.

It also signals that competition and regulatory pressure will intensify as the scale becomes material to financial systems.

BNPL Spending to Reach USD 995 Billion in 2026

Spending via BNPL services is expected to nearly double its 2021 levels, reaching USD 995 billion in 2026, as consumer adoption deepens globally. Juniperresearch

That figure reflects the sum of installment-based purchases across online and offline channels. With this scale, BNPL platforms cross thresholds that attract institutional capital and regulatory scrutiny alike.

86.5 Million Americans UsedBNPL in 2024

In 2024, roughly 86.5 million U.S. consumers used BNPL at least once—about 1 in 3 adults. Capital One Shopping

That base is growing more slowly now but provides a strong foundation for further adoption into 2026 and beyond.

As adoption saturates younger cohorts, growth may increasingly come from older demographics and repeat use.

BNPL Usage Among Uk’s Older Cohort Rose to 21% of 55–64 Year Olds

In the UK, BNPL adoption among adults aged 55–64 jumped from 10% in 2023 to 21% in 2024, showing expansion beyond younger users. The Guardian

This trend suggests BNPL is becoming more accepted across broader demographics, not just early adopters.

It also raises risk management complexities, since older users may have different financial behaviors and credit profiles.

BNPL Share Hit 5 Percent of Global E-Commerce Transactions in 2024

BNPL accounted for 5% of all e-commerce payments worldwide in 2024, rising steadily from prior years. Digital Silk

That share is expected to increase further, especially as embedded finance and checkout integration deepen.

Brands and merchants that don’t offer BNPL risk losing conversion or share to competitors who do.

66% of Users Find BNPL Risky

Despite the popularity of BNPL, 66% of users express concerns about the financial risks associated with its use. (Payment Dive)

Many consumers may underestimate their total debt due to the fragmented nature of BNPL transactions, which often do not report to credit agencies.

It points out the need for greater consumer education on responsible borrowing and the potential risks of using BNPL services for budgeting, as misuse can result in considerable financial strain.

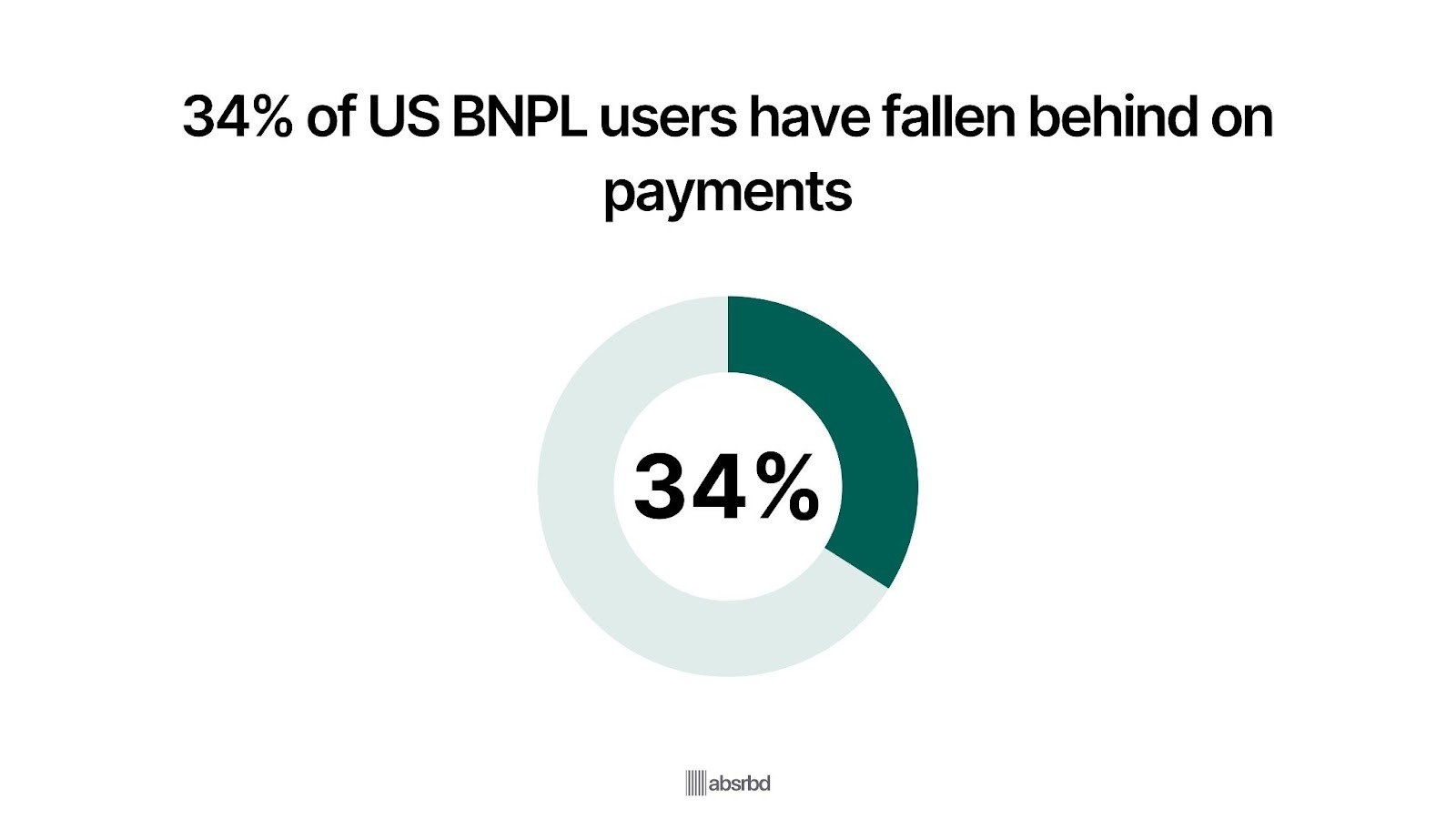

34% of Users in the US Have Fallen Behind on One or More Payments

Another challenge is the potential for rising consumer debt. BNPL services can encourage consumers, particularly younger ones, to overspend since payments are deferred.

A survey by Credit Karma found that 34% of U.S. BNPL users have missed at least one payment, leading to late fees and negatively affecting their credit scores.

This growing debt burden could pose a long-term risk to consumers and BNPL providers.

The Buy Now, Pay Later (BNPL) industry faces several key challenges that could impact its growth and sustainability. Here are the major challenges identified:

BNPL Has Over 200 Providers Globally Making the Market Hyper Competitive

The BNPL industry is becoming increasingly competitive, with over 200 companies that offer BNPL services. (Statista)

This saturation has led to price pressure and reduced profit margins for existing providers.

Major banks and tech giants like Apple and JPMorgan Chase have entered the BNPL space, leveraging their established customer bases and resources.

This is crucial as it threatens smaller BNPL firms, which may struggle to compete with larger, more resourceful entities.

Moody's predicts that many BNPL companies may not survive independently due to these competitive pressures, leading to potential acquisitions or closures.

Key Challenges Facing the BNPL Industry

The BNPL industry faces growing challenges that threaten its rapid growth and long-term sustainability.

41% of BNPL Users Made at Least One Late Payment in the Past Year

Late payments are rising even though overall defaults remain lower than credit card averages. LendingTree

This trend signals that many consumers are relying on BNPL to manage cash flow rather than convenience.

As more users juggle multiple payment plans, providers face higher credit risk and potential regulatory scrutiny.

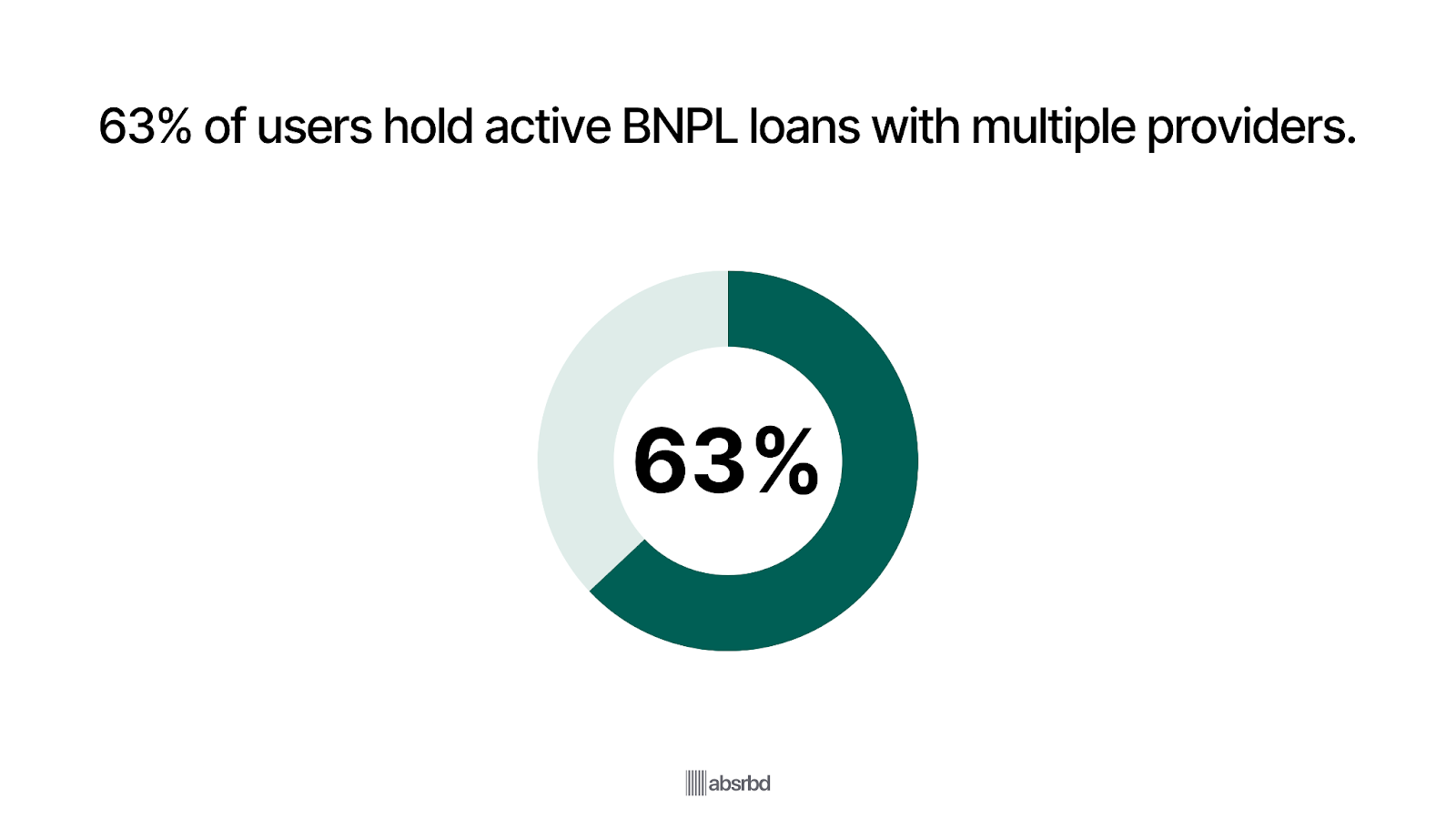

63% of BNPL Users Have Active Loans With Multiple Providers

Loan stacking, taking on several BNPL plans across different apps — is becoming a serious visibility issue.

Without unified credit reporting, users can overextend themselves across platforms.

This lack of transparency increases delinquency risk and creates “hidden debt” that traditional lenders cannot easily assess.

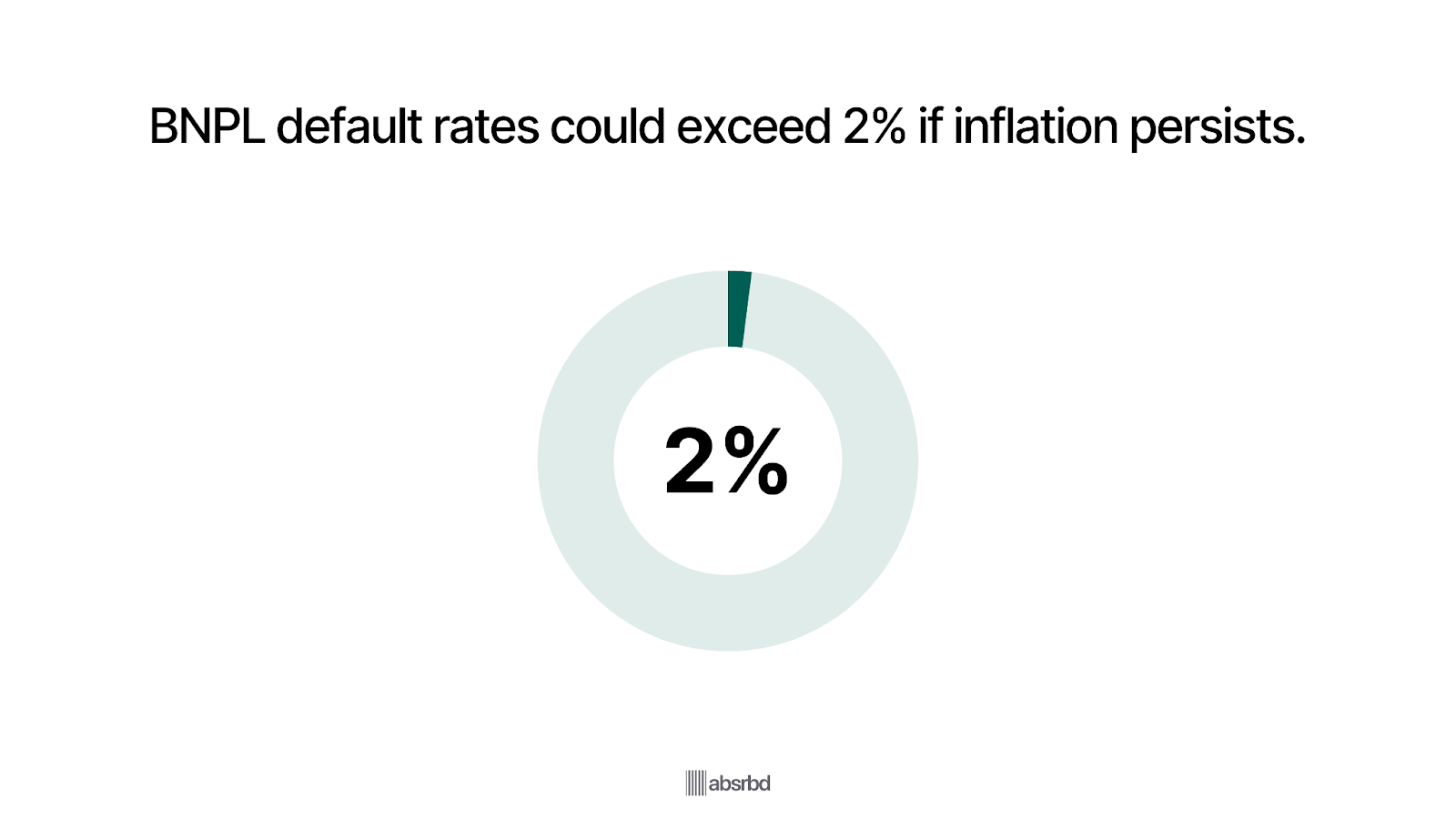

Default Rates Could Rise Above 2% if Inflation Pressures Persist

While BNPL default rates currently average around 2%, inflation and higher living costs could push defaults higher. CFPB

For thin-margin providers, even small changes in loss rates can erode profitability.

Risk-adjusted pricing and improved affordability checks will be critical through 2026.

UK Introduces New Affordability Rules for BNPL Loans Under £50

From mid-2026, UK regulators will require affordability checks for all BNPL products, even low-value purchases. The Guardian

This marks the end of “light-touch” regulation in the sector.

Compliance costs will rise, and smaller providers may struggle to adapt, potentially accelerating market consolidation.

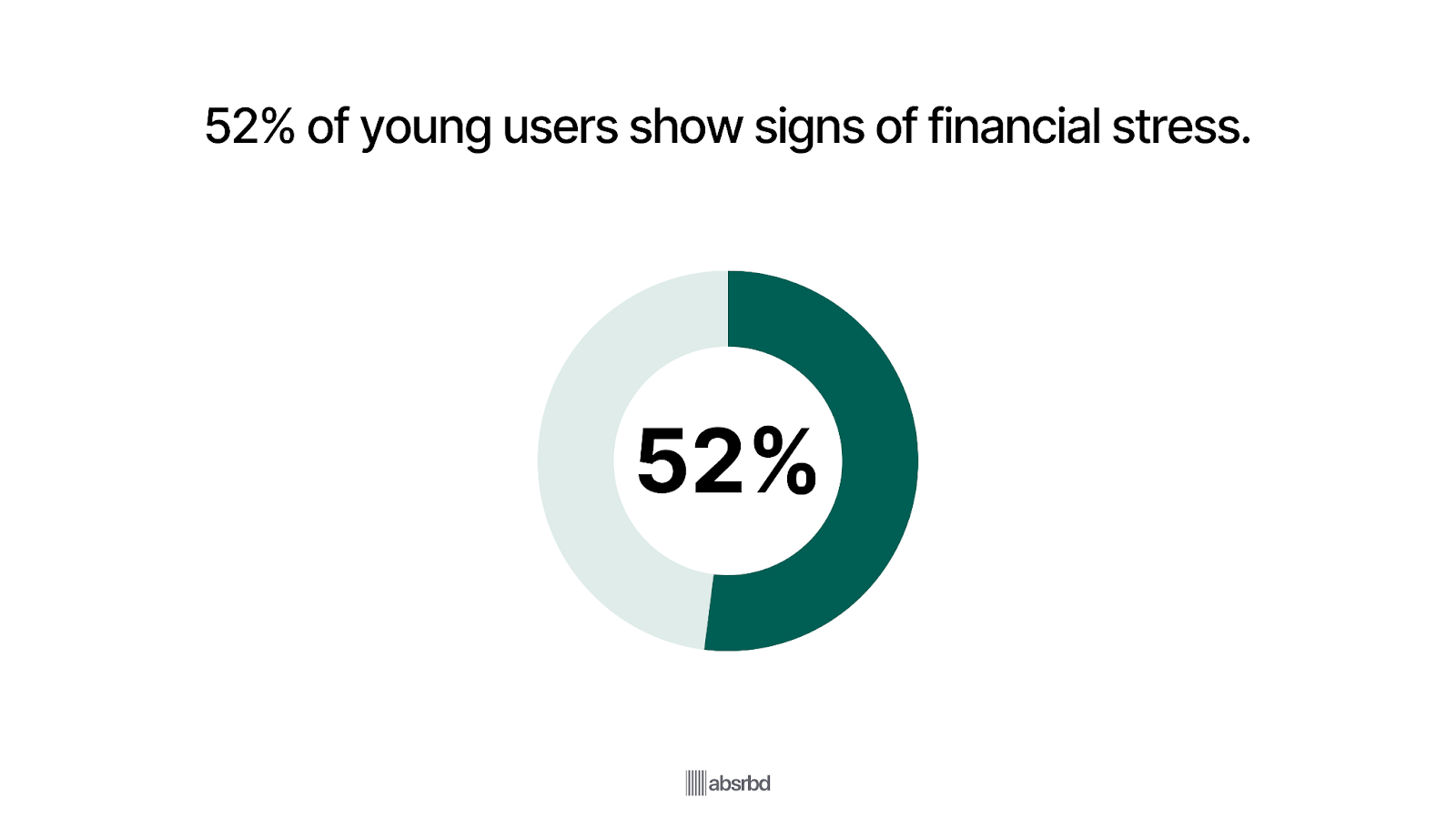

52% of Younger BNPL Users Show Signs of Financial Stress

A Dutch market study found that over half of BNPL users under 35 regularly overdraw accounts or miss payments. Empower

Younger consumers tend to view BNPL as free credit rather than debt, increasing their risk of financial hardship.

Providers face growing pressure to build responsible lending frameworks tailored to younger audiences.

Many BNPL Loans Remain Unreported to Credit Bureaus Investopedia

In most markets, BNPL loans still don’t appear on consumers’ credit reports.

This blind spot makes it difficult to assess total debt exposure and weakens lenders’ ability to evaluate creditworthiness.

As regulators push for mandatory credit reporting, providers will need to overhaul data-sharing processes.

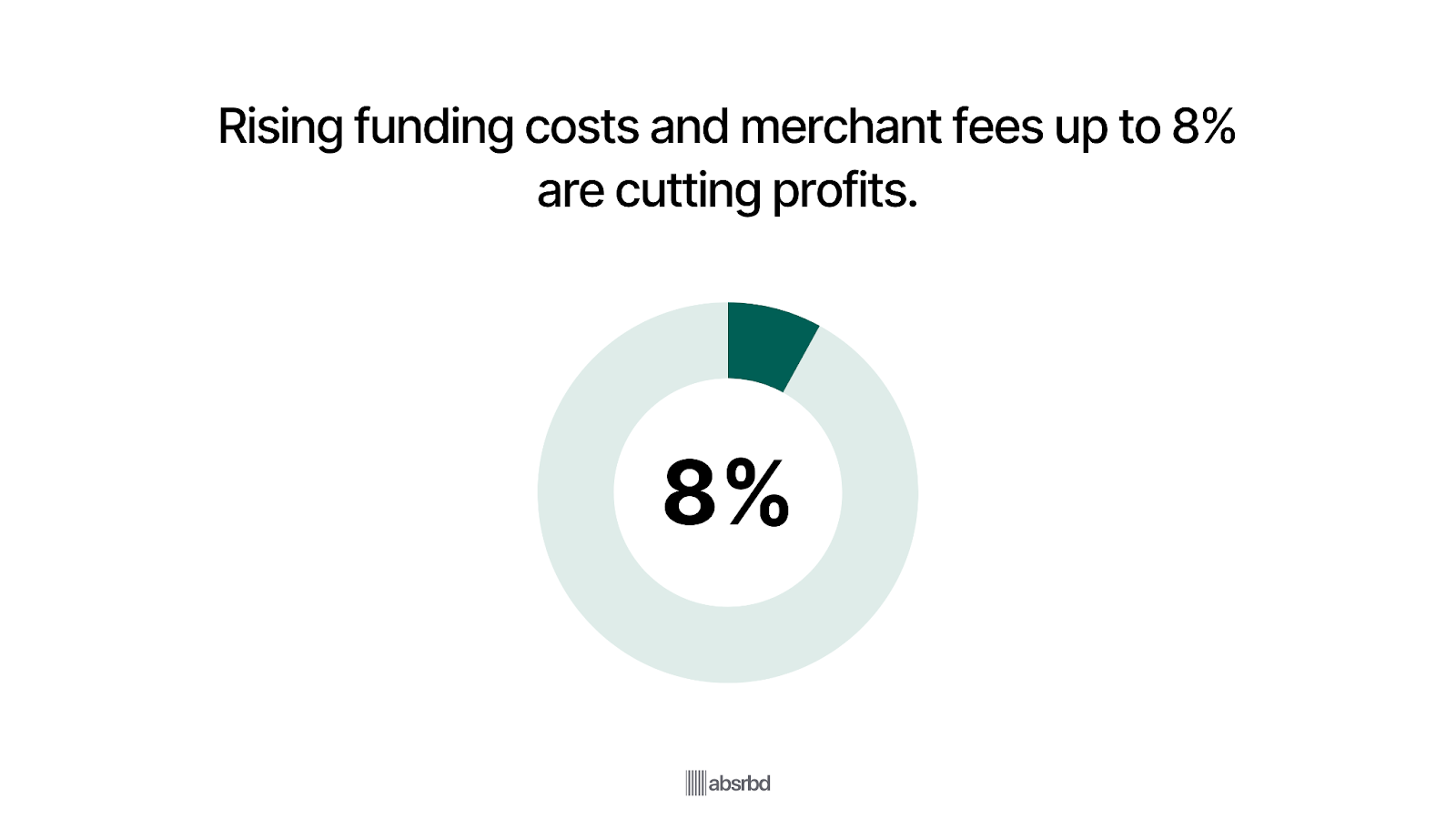

Profitability Remains Limited Despite Surging Transaction Volumes

Even as BNPL volumes approach the trillion-dollar mark, most providers are still struggling to turn a profit.

Rising funding costs, merchant fees between 2% and 8%, and high marketing spend have squeezed margins. Grant Horthon

Only the largest or most diversified players are likely to remain sustainable through 2027.

Regulatory Fragmentation Complicates Global Operations

BNPL rules vary widely across markets, from near-bank-level regulation in the UK to limited oversight in emerging regions.

Providers operating internationally face compliance complexity and increased administrative costs.

A lack of harmonized standards may slow expansion and innovation.

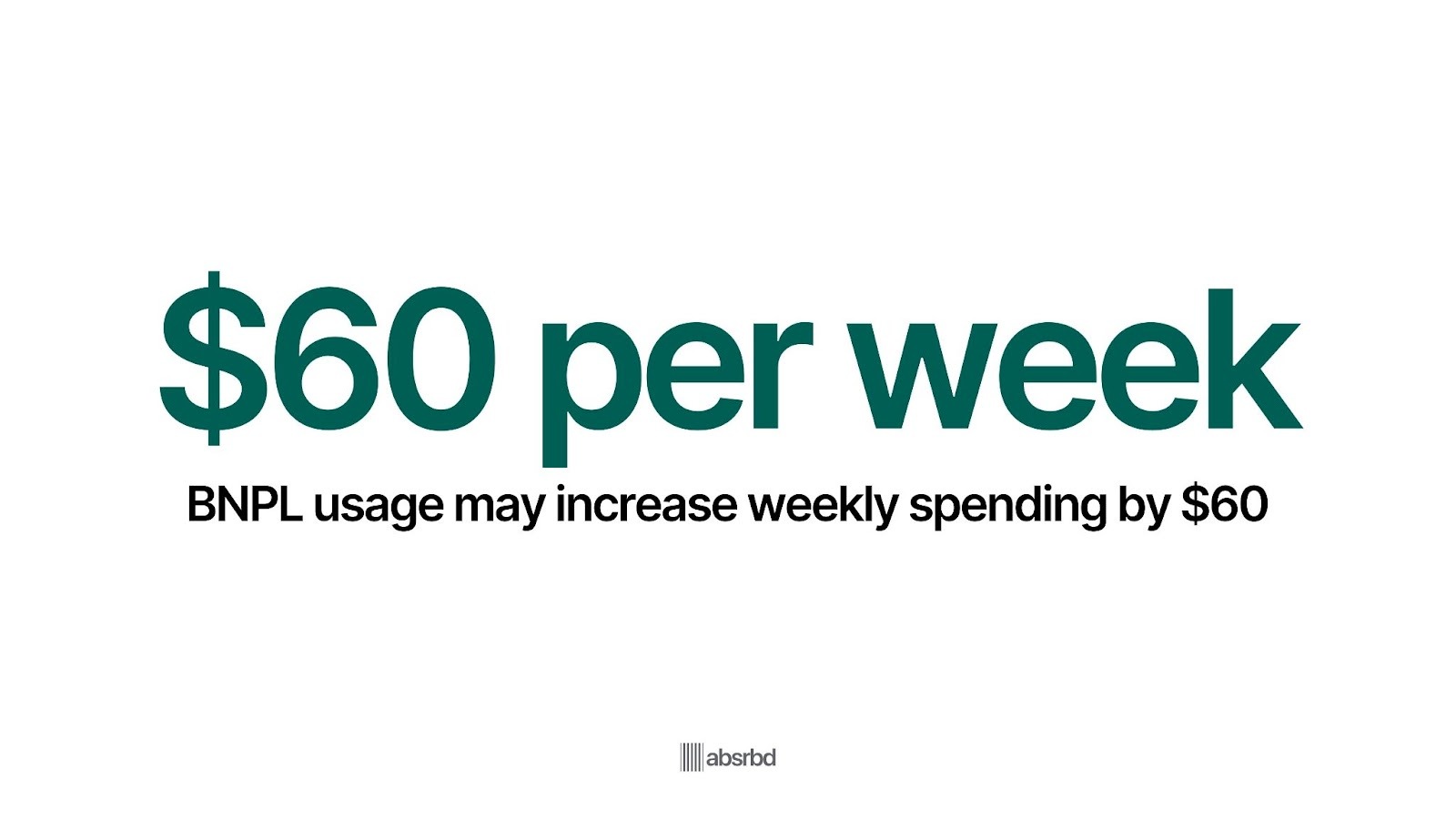

BNPL Usage Can Lead to an Increase in Spending by Approximately $60 per Week

A study by the National Bureau of Economic Research found that BNPL usage can lead to an increase in overall spending by approximately $60 per week, stretching household budgets by 30%. NBER

A lack of financial literacy among consumers is a critical challenge facing the BNPL industry.

A survey also revealed that two-thirds of BNPL users are making questionable buying decisions, purchasing more “wants” such as jewelry and other luxury items they may not have otherwise bought.

These users do not fully understand the implications of using BNPL services, leading to potential over-reliance on these payment options.

The absence of reporting to credit agencies further complicates consumers' ability to accurately gauge their overall debt levels.

It is critical as it can result in consumers accumulating unmanageable debt, ultimately affecting their financial well-being and the reputation of BNPL providers.

Efforts to improve consumer education and transparency in lending practices are essential to mitigate this issue.

Emerging Opportunities in the BNPL Market

New trends and innovations are creating fresh growth opportunities in the BNPL market by 2026.

Global BNPL Market to Reach USD 1.43 Trillion by 2030

The global BNPL market, valued at roughly USD 640 billion in 2025, is projected to reach USD 1.43 trillion by 2030, growing at a CAGR of nearly 17.5%. Mordor Intelligence

Rising e-commerce volumes, financial digitization, and increased merchant partnerships are driving sustained adoption.

Emerging markets in Asia and Latin America are expected to contribute the largest share of new users.

Healthcare and Wellness BNPL to Grow at Nearly 30% CAGR Through 2030

BNPL adoption in healthcare and wellness services is forecasted to grow at a CAGR of about 29.7%. Mordor Intelligence

Consumers are increasingly using installment plans for elective medical treatments, cosmetic procedures, and wellness subscriptions.

This diversification beyond retail strengthens BNPL’s position as a versatile financial tool.

BNPL Embedded in Point-Of-Sale and Digital Wallets Sees Record Adoption

BNPL is becoming a standard feature at checkout across digital and in-store environments.

Point-of-sale integration and digital wallet partnerships have expanded access, allowing customers to use BNPL instantly across multiple brands.

For merchants, this has resulted in higher conversion rates and larger average order values.

Alternative Credit Scoring Unlocks Underbanked Markets

AI and data-driven scoring models now allow BNPL providers to underwrite consumers with little or no credit history.

These models use mobile payment patterns, e-commerce behavior, and income proxies to assess risk.

The shift is opening up financial access to millions of users in developing economies.

Subscriptions and Memberships Adopt BNPL Flexibility

Subscription-based services, including streaming, fitness, and software memberships, are integrating BNPL payment options.

Customers can now split recurring fees into predictable installments, while providers gain more consistent revenue streams and higher retention rates.

Venture Capital Targets Vertical-Specific BNPL Startups

Investors are increasingly backing BNPL startups focused on niche segments such as healthcare, travel, and education.

These verticalized models typically face lower default risks and attract more loyal customer bases.

As competition intensifies, specialized BNPL offerings are emerging as a key differentiator in the market.

Regulatory Harmonization Strengthens Consumer Trust In BNPL

New credit-reporting frameworks in the US, UK, and EU are introducing transparency and accountability into BNPL.

Early compliance by major players is helping improve trust among regulators and consumers alike.

Standardized disclosures and credit data sharing are expected to elevate BNPL’s reputation as a responsible credit solution.

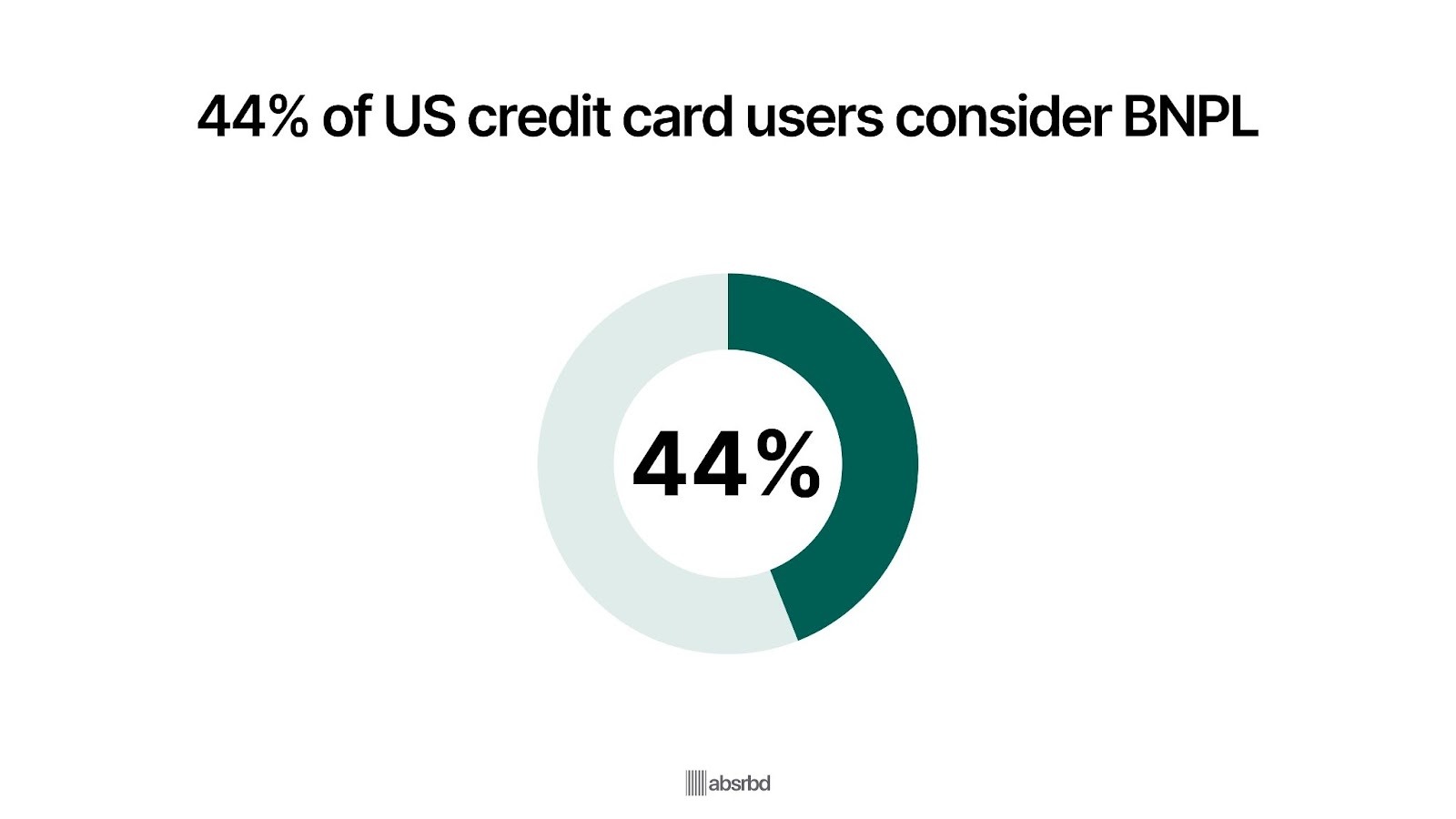

44% of Credit Card Users in the US are Considering BNPL

A study by J.D. Power found that 44% of U.S. credit card customers would consider using BNPL for high-ticket purchases. (JD Power)

This rising interest indicates a shift in consumer preferences as people look for alternatives to traditional credit cards, especially for larger transactions.

It is notable that BNPL providers have the potential to capture market share from credit card issuers, particularly among younger consumers who are increasingly cautious about credit card debt.

Impact on Stakeholders

The evolving BNPL landscape is significantly affecting all stakeholders, from consumers to lenders and retailers.

Impact on Consumers

Increased Accessibility and Flexibility

The rapid growth of BNPL services has made flexible payment options more accessible to consumers.

With 360 million users globally, BNPL allows consumers to split purchases into manageable installments, often interest-free. Global Blue

This particularly appeals to younger generations, such as Millennials and Gen Z, who prefer not to use traditional credit cards due to concerns about debt accumulation and interest rates.

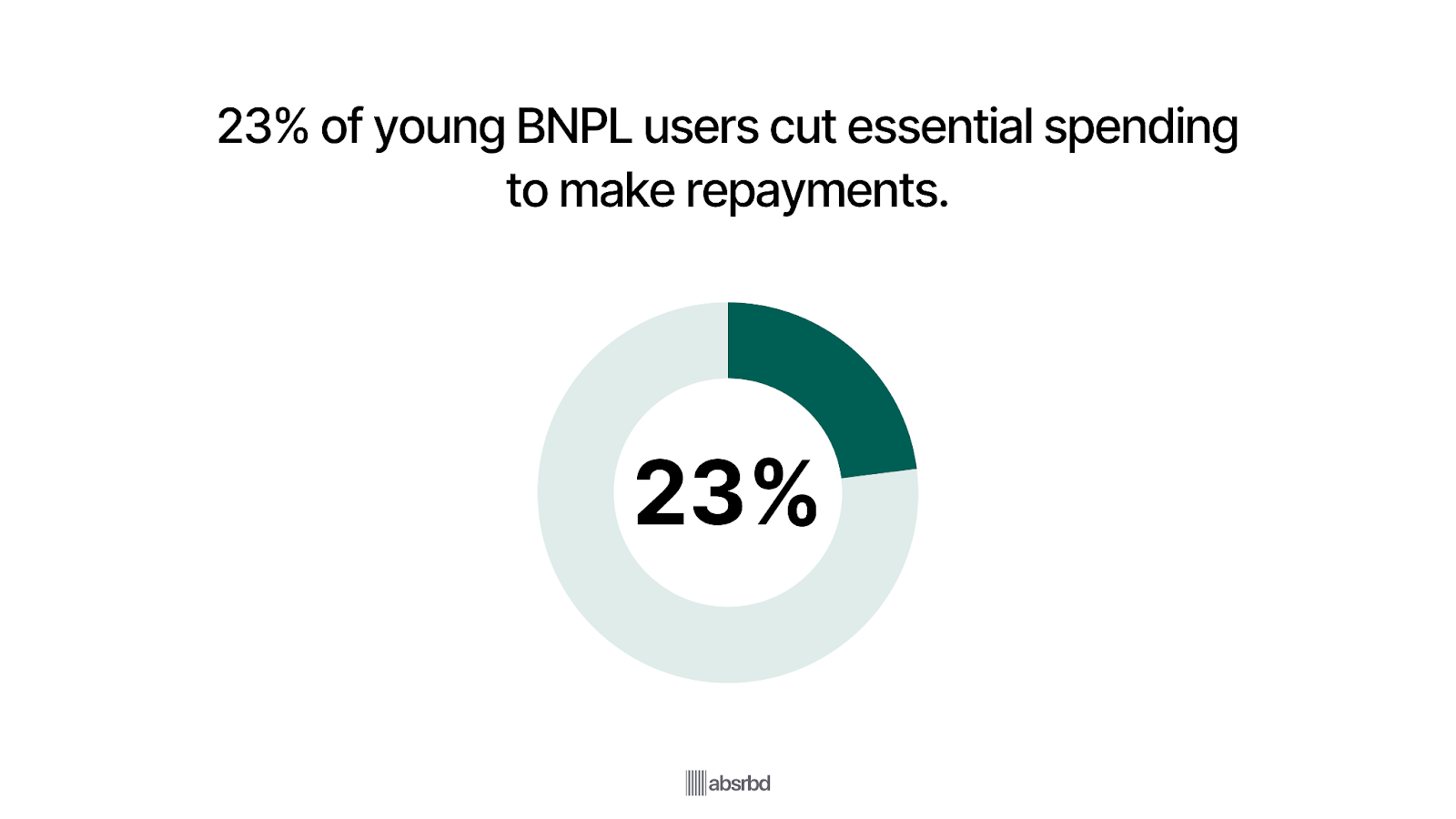

Potential for Debt Accumulation

However, the ease of access also comes with risks.

A study by Barclays revealed that almost a quarter (23%) of 18–34-year-old BNPL users have had to reduce their spending on essential purchases like groceries to keep up with their BNPL repayments. (Barclay)

With 10.5% of borrowers facing late fees in 2021, there is a considerable risk of financial strain, prompting calls for improved consumer education and responsible borrowing practices.

Impact on Businesses

1. Diversification of Customer Base: Businesses benefit from the increasing adoption of BNPL as it attracts a broader customer base. Diversifying BNPL usage beyond apparel to sectors like healthcare and travel opens new revenue streams for merchants. For example, companies like Affirm are partnering with healthcare providers to offer financing for medical expenses, addressing a critical need for many consumers.

2. Increased Sales and Average Order Values: Using BNPL can lead to higher sales and increased average order values. The average individual order financed by BNPL rose from $121 in 2020 to $135 in 2021, indicating that consumers are more likely to make larger purchases when they can pay in installments.

Impact on Investors

1. Market Growth and Investment Opportunities: The BNPL market is projected to reach $80.77 billion in total payment value by 2024, presenting substantial investment opportunities. Investors are keen on the growth potential of BNPL providers, especially as the market expands into new sectors and demographics.

2. Risk of Market Saturation and Competition: However, investors must also consider the risks associated with increased competition and market saturation. With over 200 BNPL providers competing for market share, profit margins may be pressured, particularly as larger players like banks and tech companies enter the space.

Conclusion

The rise of Buy Now, Pay Later (BNPL) services is reshaping the financial sector for stakeholders. Consumers gain increased purchasing flexibility but face potential risks of overspending.

Conventional banks are challenged to innovate or risk obsolescence. This shift is prompting a reassessment of lending practices industry-wide.

With BNPL's rapid adoption, particularly among younger users, we can anticipate heightened regulatory oversight and possible industry consolidation.

Future success in this field will depend on balancing protecting consumers and fostering innovation. Companies that excel at using data to make responsible lending decisions and offer user-friendly interfaces are likely to lead the growing alternative finance market.

Frequently Asked Questions

Who is the Leader of BNPL?

- Klarna is frequently mentioned as a leading global BNPL provider, boasting millions of users and partnerships with numerous retailers. It is also described as the largest BNPL company based on the number of consumers and retailers using its services.

- Afterpay, with Affirm and Zip, is recognized as one of the "big four" global BNPL providers, each with a large user base.

- Affirm is another prominent BNPL company, especially in the U.S. market. It is mentioned as one of the major BNPL players partnering with large retailers like Apple, Amazon, Walmart, and Target.

- Zip (formerly known as QuadPay) is also highlighted as a leader in the BNPL space, offering payment options for major retail giants.

What Percentage of Americans Use BNPL?

Recent statistics show that adopting Buy Now, Pay Later (BNPL) services in the United States is widespread.:

- Around 1 in 5 BNPL users live in the US, which translates to approximately 79 million US-based BNPL users as of 2022, an increase of 56.1% over the previous year. (Exploding Topics)

- In 2023, about 50% of US consumers reported using BNPL services, up from 37.7% in 2020. (E Marketer)

- Adoption rates among Gen Z in the US are expected to increase from 36.8% in 2021 to 47.4% by 2025, while 32.6% of Gen X and 15.3% of baby boomers are projected to use BNPL in 2024. (Exploding Topics)

Why Shouldn't I Use BNPL?

1. Risk of Overspending and Debt Accumulation: BNPL services can lead to overspending, as consumers may focus solely on manageable payment amounts rather than the total cost of their purchases. This can result in accumulating debt, especially if multiple purchases are financed simultaneously, making it challenging to keep track of total financial obligations.

2. Fees and Interest Charges: Missing a payment can result in late fees or interest charges, which can quickly add up. If payments are not made, accounts may be sent to collection agencies, potentially damaging the consumer's credit score.

3. Potential for Overdrafts: Automatic payments scheduled through BNPL can increase the risk of overdrafts in consumers' bank accounts. If consumers do not keep track of their payment schedules, they may incur additional fees from their banks.

4. Loss of Rewards and Benefit: Using BNPL instead of credit cards means consumers may miss out on rewards programs and other benefits typically offered by credit cards, such as purchase protection and cashback incentives.

5. Lack of Understanding: Many consumers do not fully understand the terms and conditions of BNPL agreements, which can lead to missed payments and unexpected financial strain. A survey indicated that 34% of BNPL users have fallen behind on payments, highlighting the need for better consumer education.