%20Statistics%202025.png)

111 NE 1st ST

Miami, Florida 33132

USA

88% of financial institutions fear losing part of their business to standalone fintech companies, according to PwC's 2021 Global Fintech Survey.

This unexpected concern is just one of many intriguing Banking-as-a-Service shifts.

This article explores statistics revealing the state and trajectory of this rapidly evolving sector in financial technology.

From market size projections to adoption rates across industries, we'll uncover the numbers behind the BaaS innovation.

Data Sources and Methodology

This article combines open-access resources and proprietary data to present accurate, up-to-date statistics and developments in banking as a service.

Our methodology involves:

- Aggregating data from government databases, industry reports, and academic publications

- Incorporating exclusive insights from leading industry providers

- Regular updates to reflect the latest information

Key data providers include:

While we strive for accuracy, happenings in banking as a service are shifting rapidly.

These statistics reflect current patterns and should not be considered permanent facts.

Key Takeaways

- The global BaaS market is projected to reach $14.72 billion by 2029, growing at a CAGR of 26.6%

- 93% of fintech companies cite regulatory compliance as a major challenge.

- 84% of banks plan to increase their fintech partnerships by 2025.

- By 2025, 90% of banks are expected to move to cloud-based platforms.

- Only 32% of consumers trust fintech companies with their financial data.

Overview of Banking as a Service (BaaS)

Banking as a Service BaaS emerged in the late 2010s, driven by the rise of fintech innovation and the increasing demand for digital financial services.

It refers to a model where non-banking businesses can offer banking services by leveraging the infrastructure and licensing of traditional banks through APIs.

Since its inception, BaaS has grown rapidly, enabling fintech companies, e-commerce platforms, and other industries to integrate financial services directly into their offerings.

Key milestones include the widespread adoption of embedded finance and partnerships between traditional banks and fintech firms.

Today, the BaaS market is characterized by its rapid expansion and growing competition, with the global market expected to grow at a CAGR of 26.6% through 2029. Mordor Intelligence

Major players include companies like Marqeta, Solarisbank, and Synapse, while factors such as regulatory developments and technological advancements in artificial intelligence and blockchain continue to shape the industry's trajectory.

With a projected market size of $14.72 billion by 2029, BaaS is crucial in democratizing access to financial services, enabling innovation, and driving global financial inclusion. Mordor Intelligence

This makes it a key area of focus for fintech companies, traditional banks, investors, and regulators alike.

Key Statistics

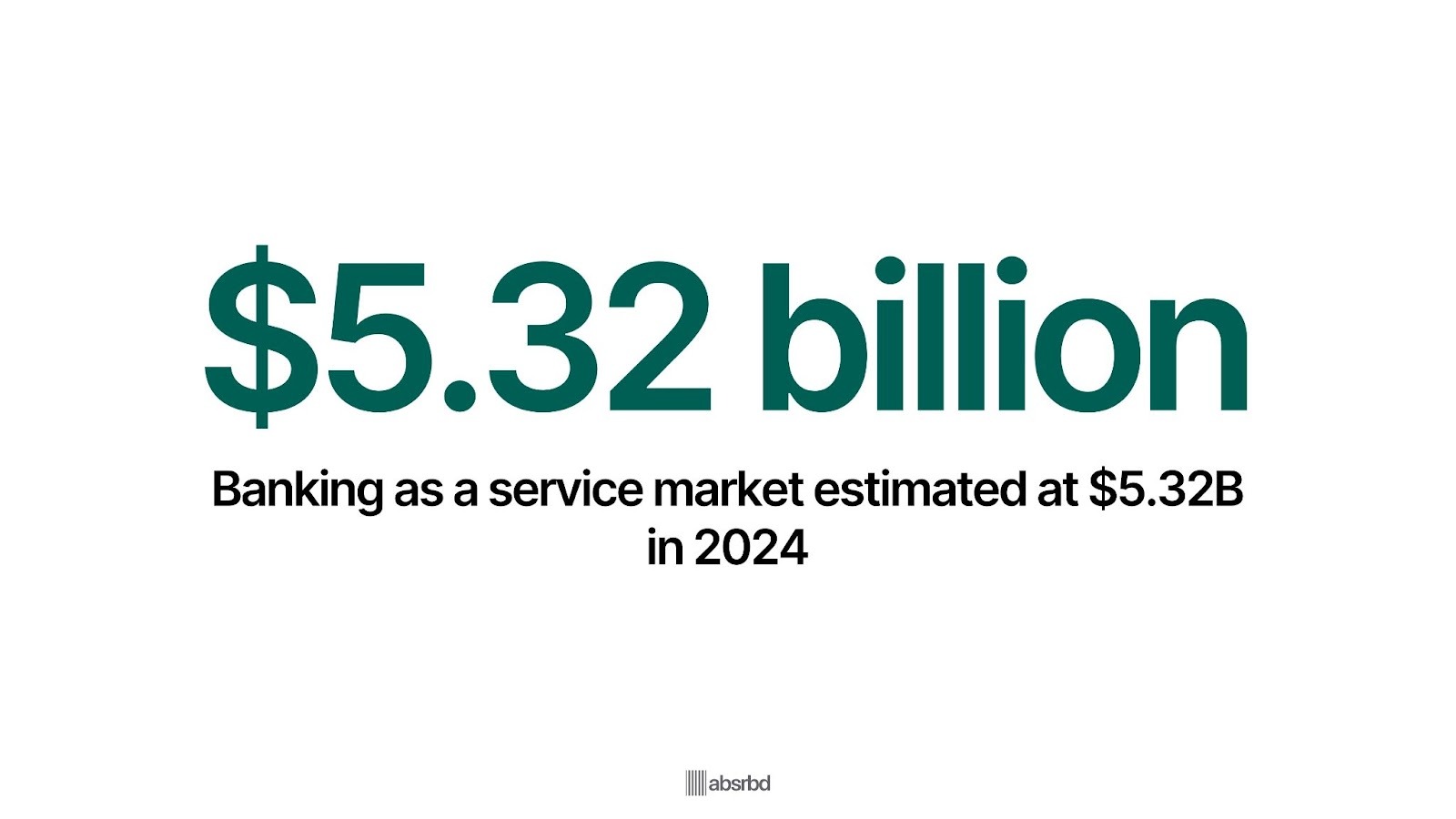

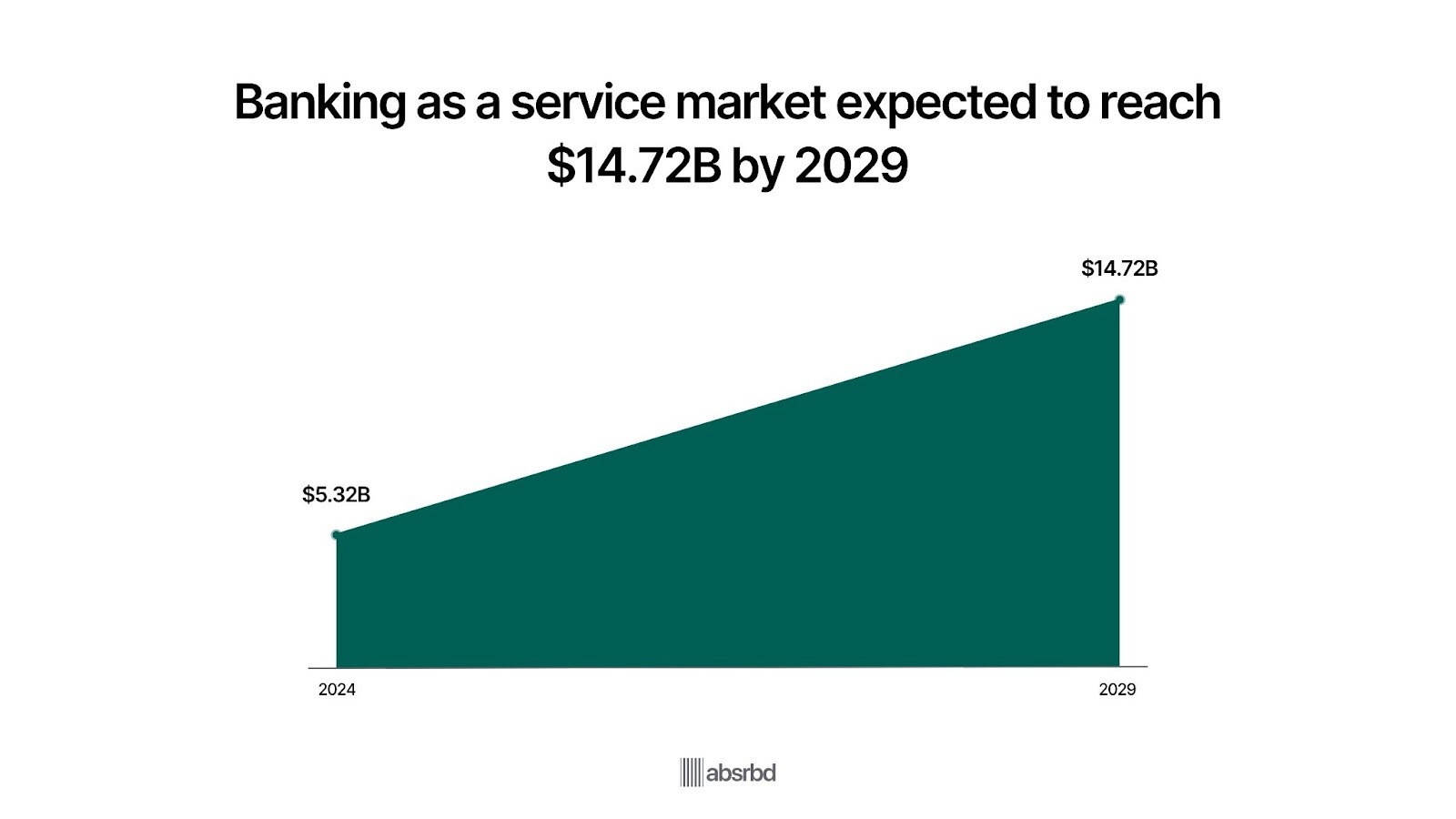

- The banking as a service market is estimated at $5.32 billion in 2024. Mordor Intelligence

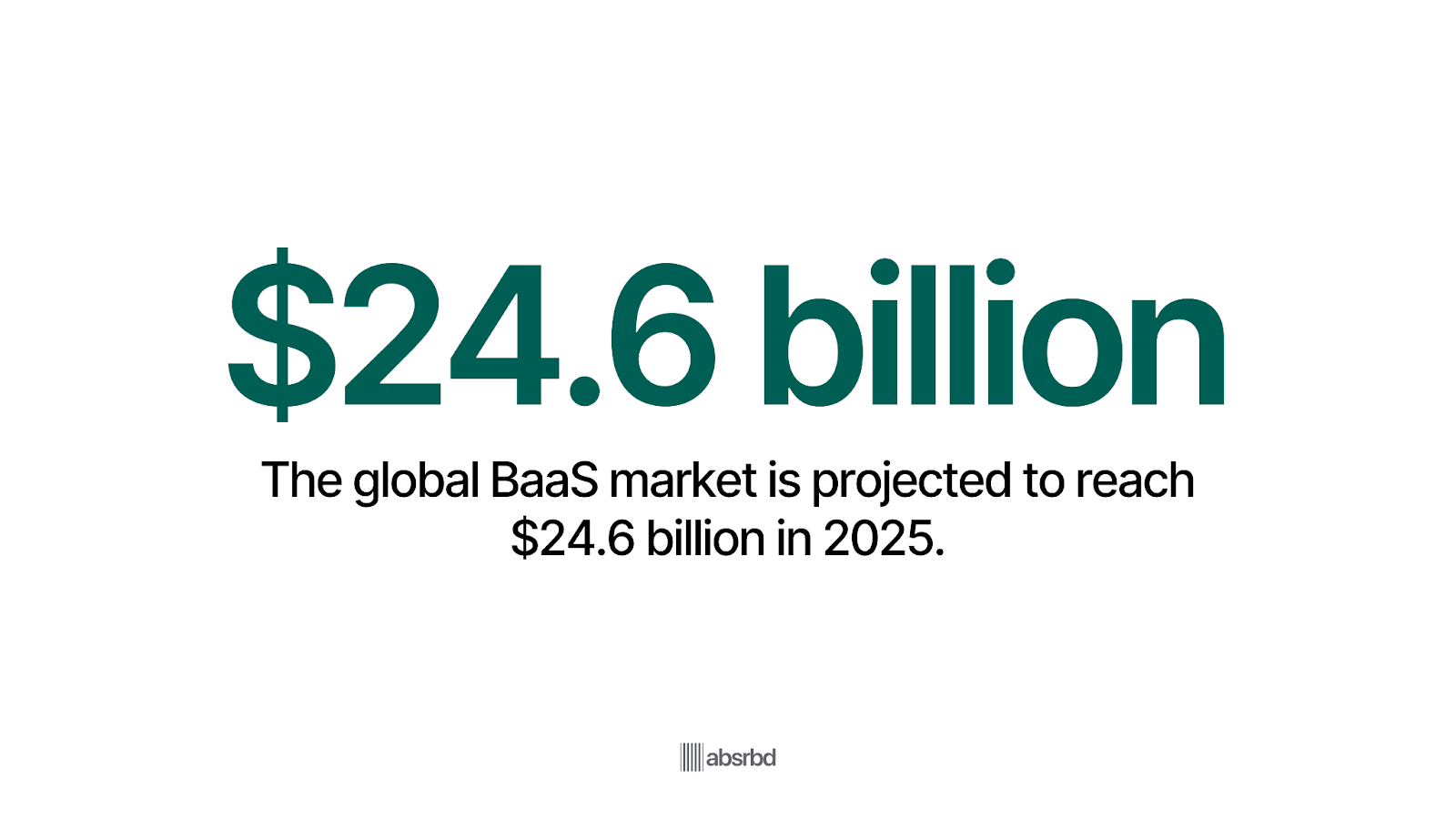

- According to Mordor Intelligence, the global BaaS market is projected to reach $24.58 billion in 2025. Mordor Intelligence

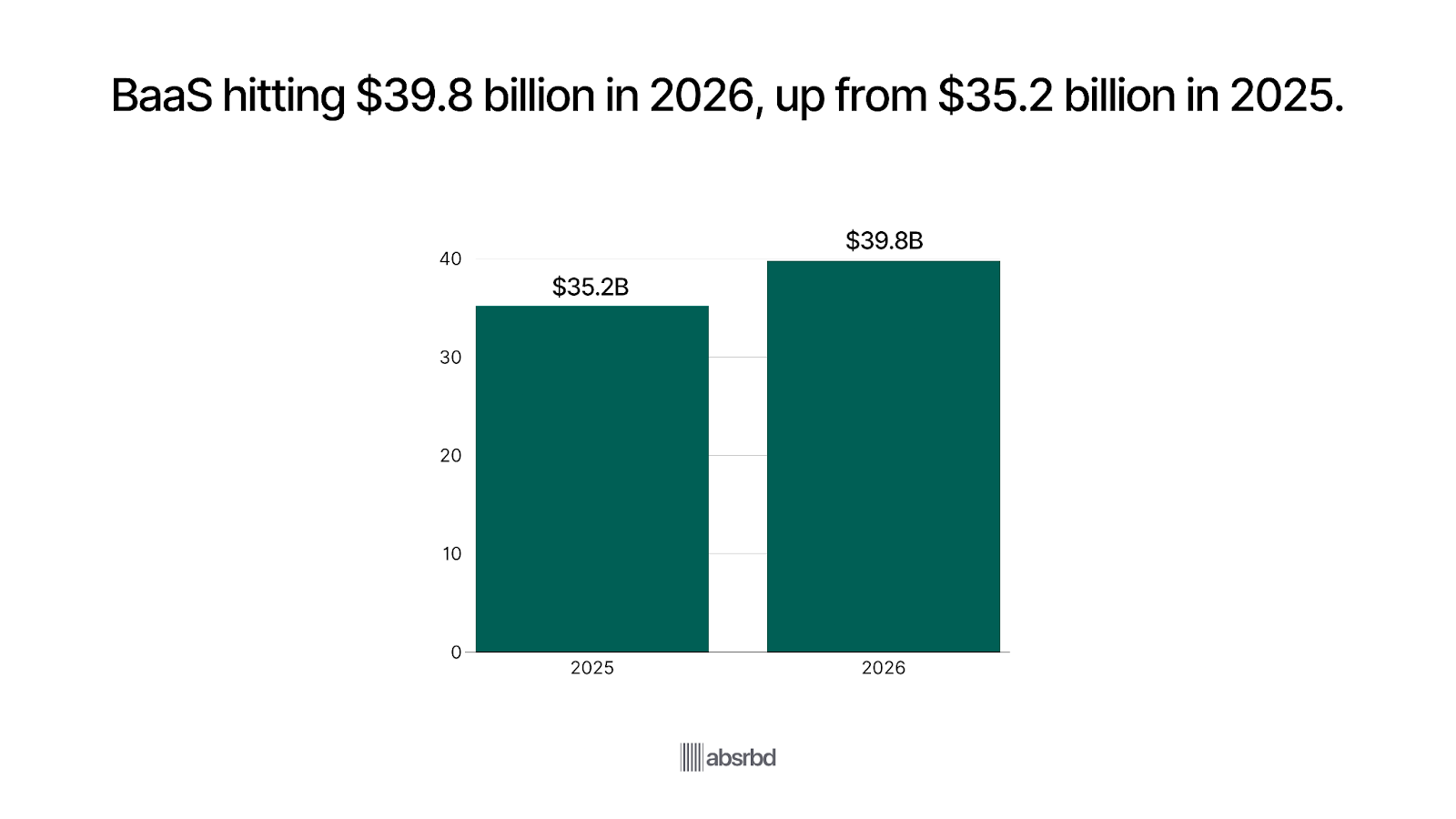

- One forecast estimates the BaaS market will hit $39.8 billion in 2026, up from USD 35.18 billion in 2025. Research Nester

- It is expected to reach $14.72 billion by 2029. Mordor Intelligence

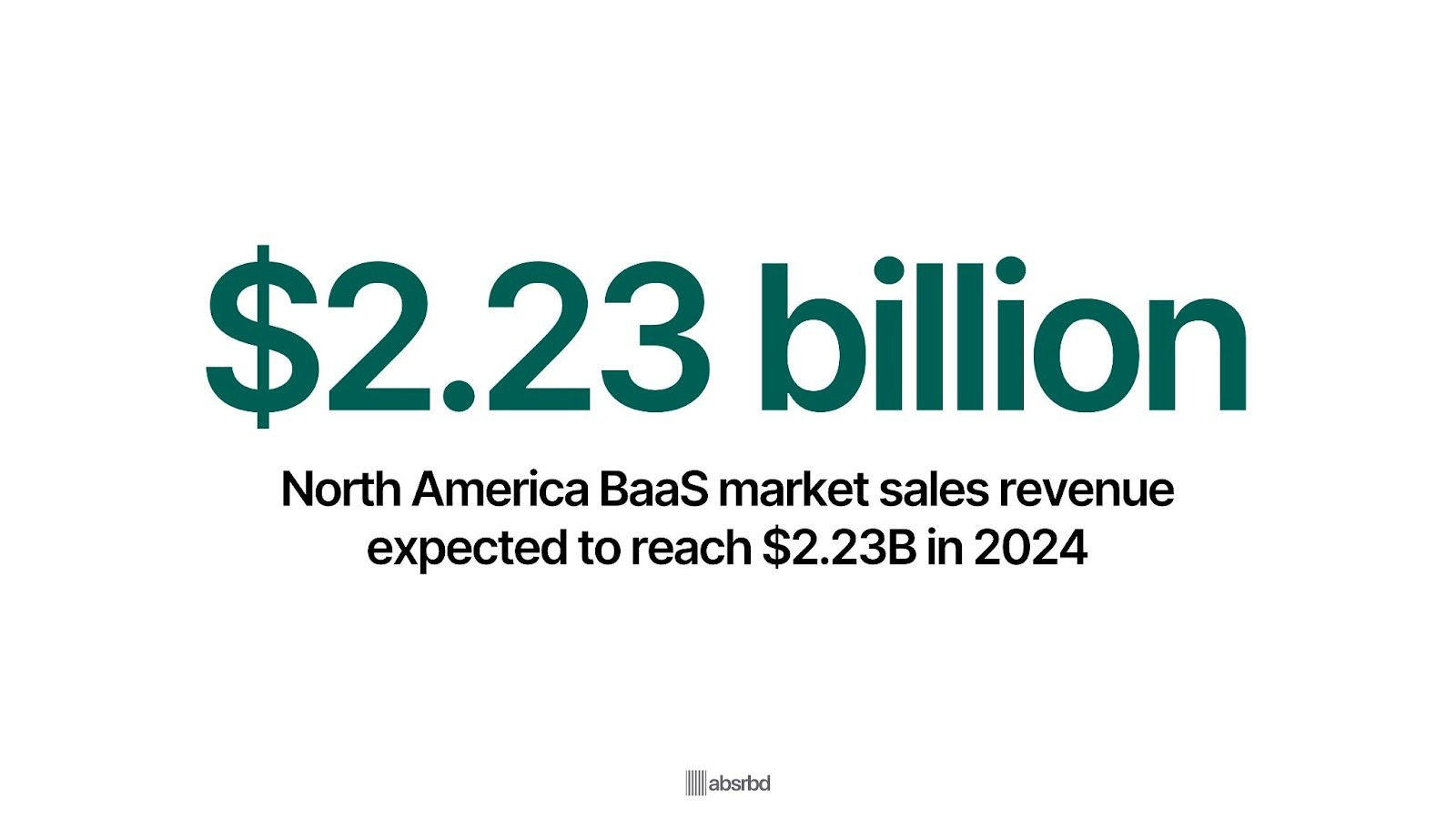

- North America Banking as a Service BaaS market sales revenue in 2024 is expected to reach. $2.23 billion. Cognitive Market Research

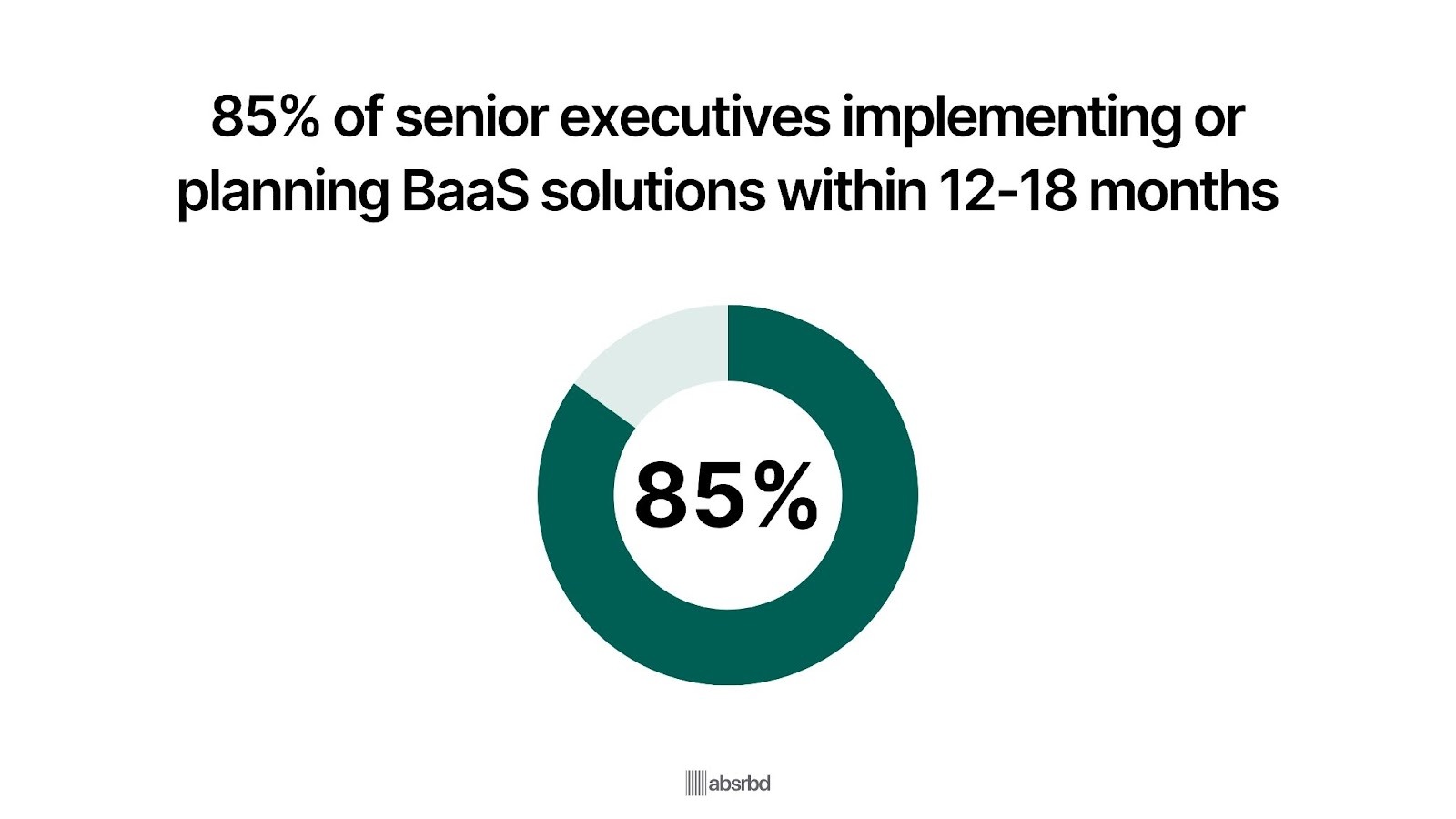

- 85% of senior executives are already implementing BaaS solutions or planning to do so within the next 12-18 months. Mordor Intelligence

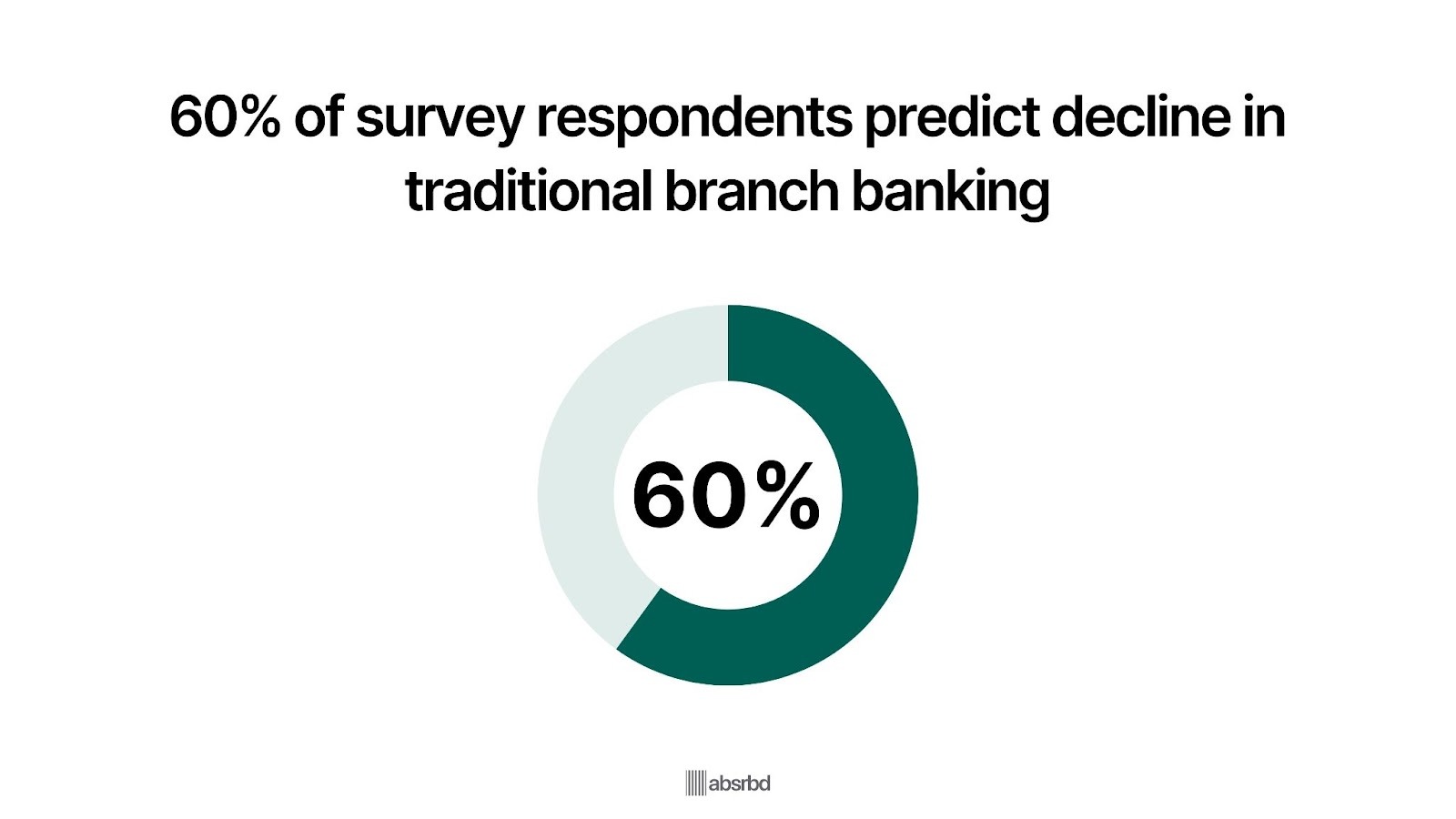

- In a survey, 60% of correspondents predicted a decline in traditional branch-based banking. Vodeno

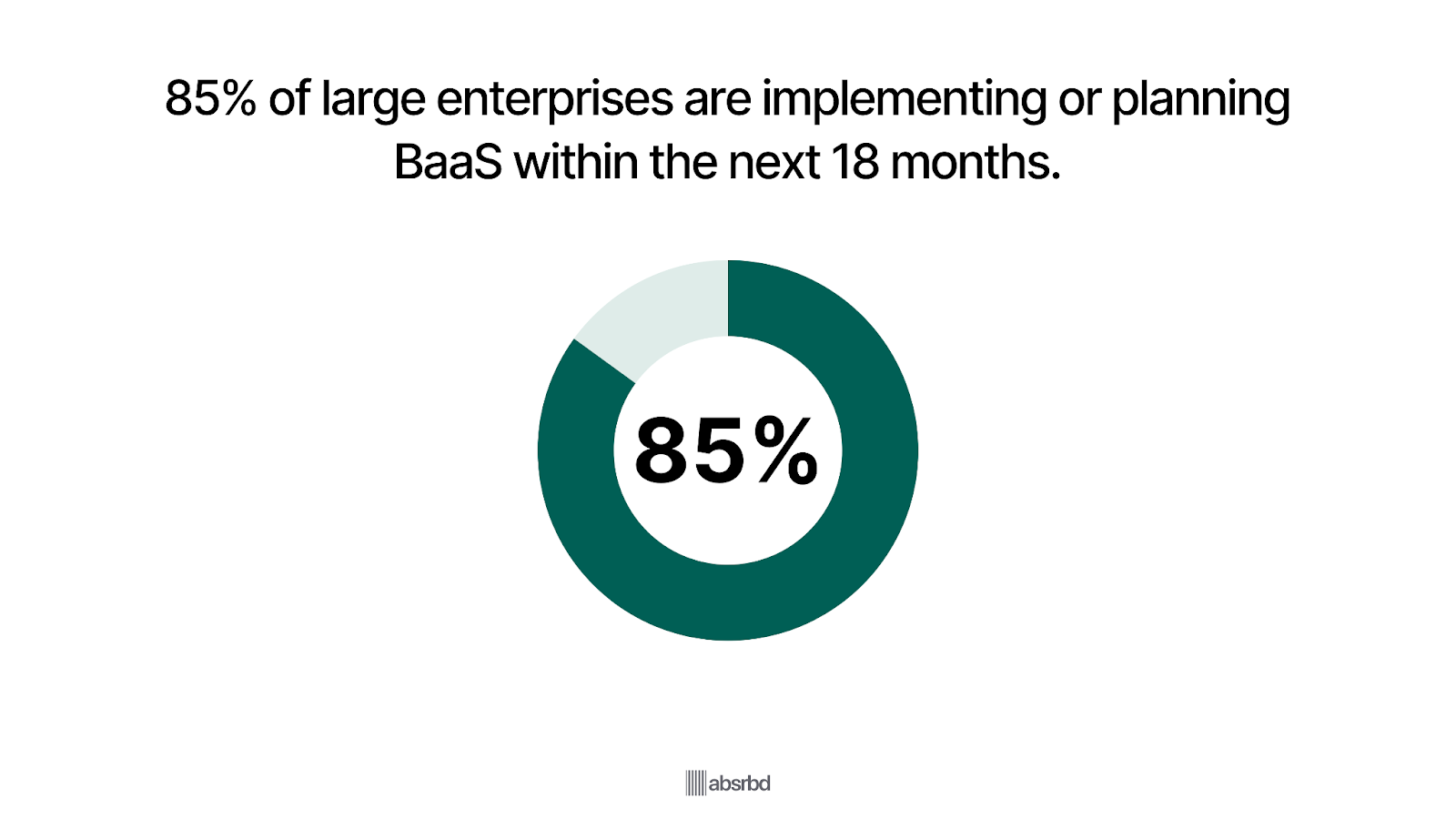

- Large enterprises lead adoption with 85% either implementing or planning BaaS within 18 months. Cognitive market research

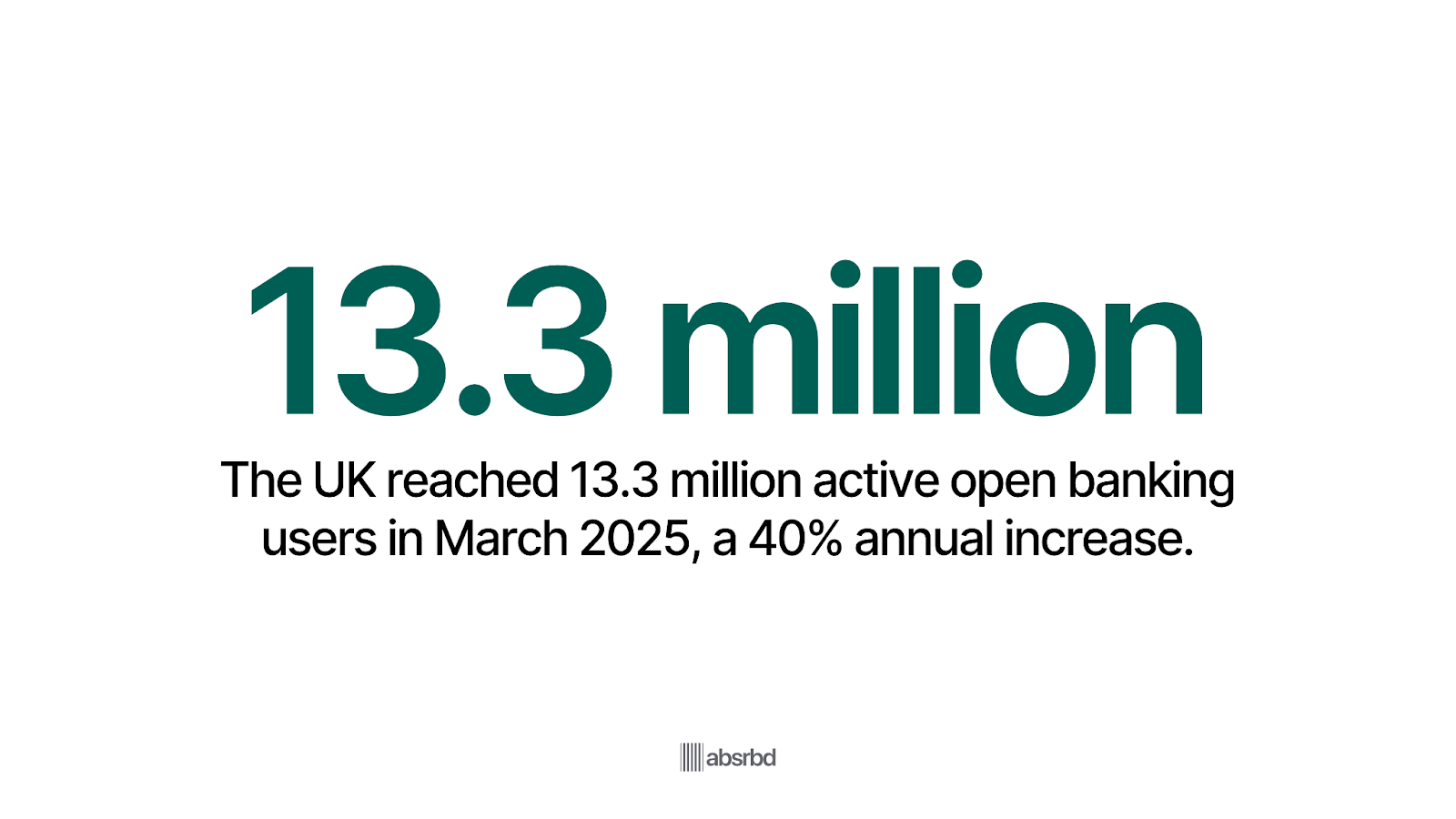

- In the UK, active open banking users numbered 13.3 million as of March 2025, up 40% from the previous year, evidencing rapid user adoption. Open banking

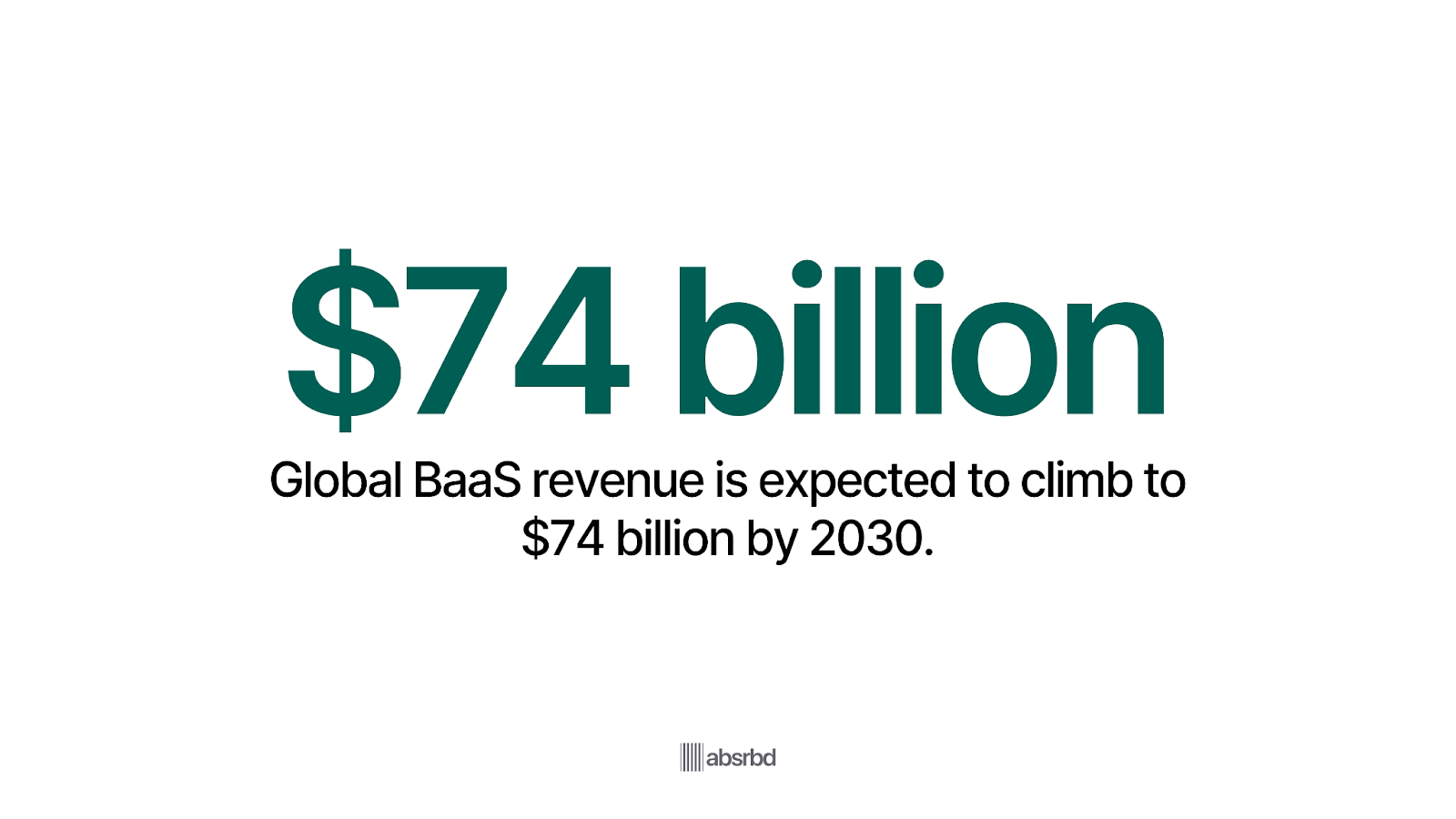

- The worldwide BaaS revenue is poised to reach $74 billion by 2030. Finance yahoo

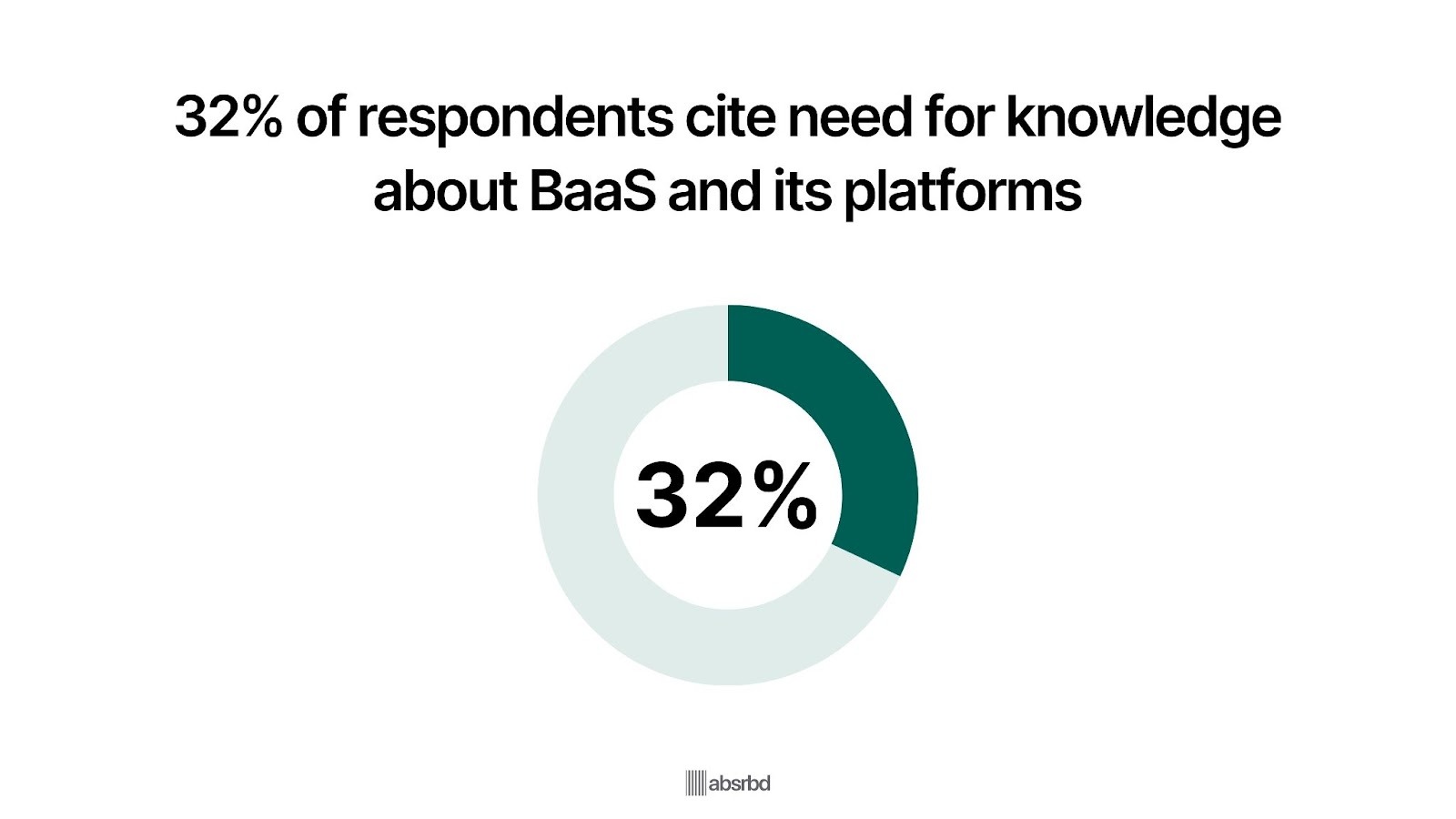

- Among respondents who still need to implement BaaS services, 32% cited a need for knowledge about BaaS and its platforms. Vodeno

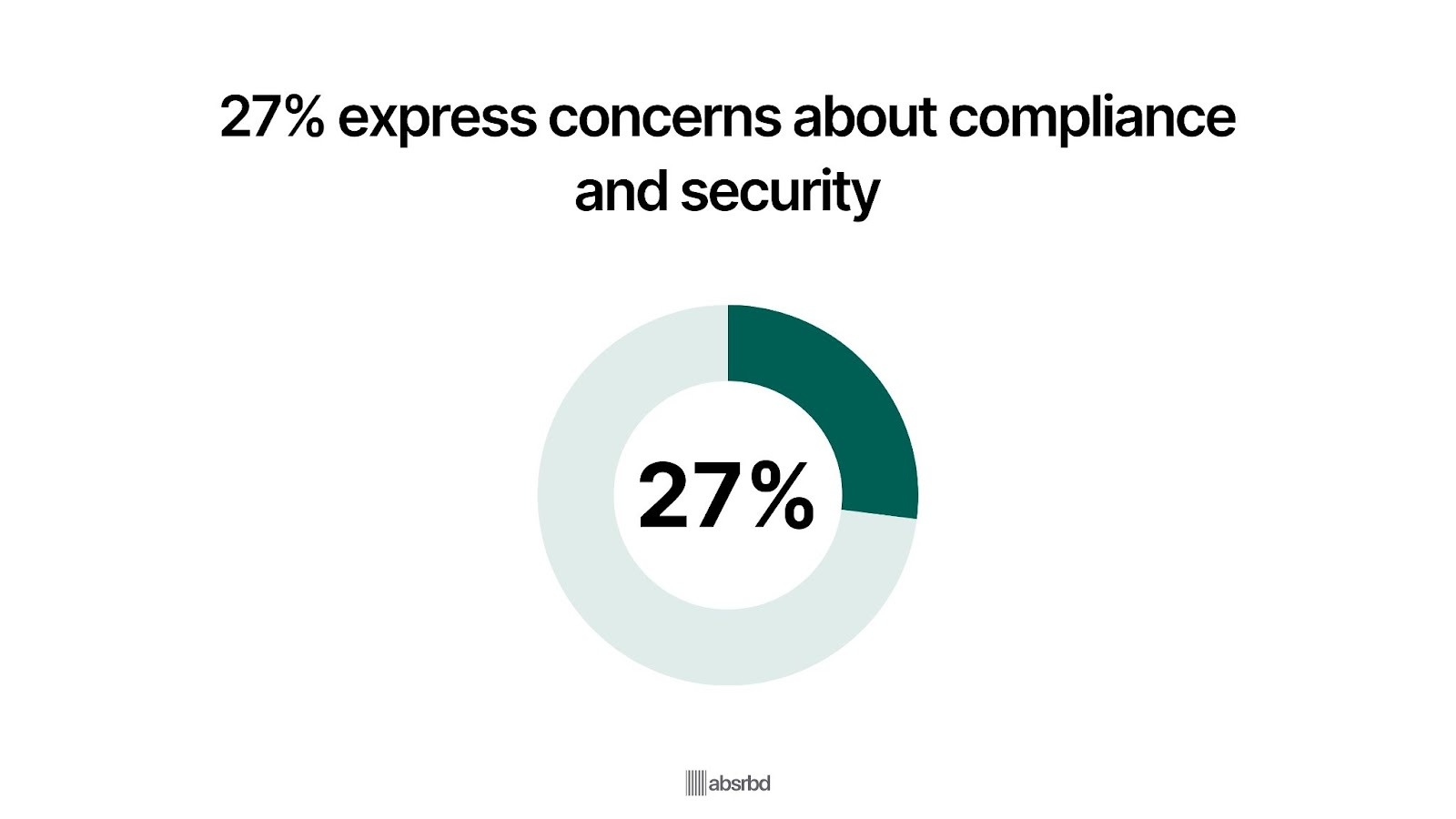

- 27% express concerns about compliance and security. Vodeno

Major Trends in Banking as a Service Sector

The BaaS sector is experiencing rapid expansion with several shifts shaping its course:

70% of Consumers Expect Personalized Financial Services From Their Providers

Consumers increasingly expect personalized financial services tailored to their specific needs.

According to a survey by Accenture, 70% of consumers expect their financial service providers to offer personalized services based on their spending habits and financial goals. Fintech Magazine

BaaS platforms enable companies to deliver these personalized experiences by leveraging data analytics and AI.

Personalization is becoming a key differentiator in the competitive financial services market.

As personalization becomes a key differentiator in the competitive financial services market, BaaS providers offering the tools and technologies to deliver personalized experiences are set to be in high demand.

This demand is expected to come from fintech companies and traditional banks alike as they seek to meet the growing expectations of consumers.

Chime, a U.S.-based digital bank, uses BaaS to offer personalized financial products such as fee-free overdrafts and early direct deposit access, catering to the unique needs of its customer base.

This personalization has helped Chime grow to over 12 million users. Technology Magazine

SMEs Driving 40% of New BaaS Demand by 2026

Small and medium-sized enterprises are emerging as the next frontier for BaaS growth.

40% of SMB Merchants Consider Moving from Banks to PayTechs, adopting embedded banking for faster payments, credit access, and automated financial workflows. Fintech demand

BaaS is enabling SMEs to launch digital wallets and embedded credit tools at record speed.

These businesses want banking functionality without banking bureaucracy, and BaaS delivers exactly that.

AI-Driven Compliance Reduces Risk and Costs by Up to 30%

AI and machine learning are transforming regulatory compliance in BaaS.

Automation now reduces manual monitoring, improves fraud detection accuracy, and cuts compliance costs by up to 30%. GSC online press

A study on ML-based cloud computing compliance processes claims improvement in accuracy from 78% to 93%, which is a 15 percentage points gain 19% in risk identification/accuracy. arXiv

This shift from reactive to proactive compliance turns regulation into a value-add, helping financial partners launch safely and scale faster.

60% of Fintech Companies Cite Regulatory Compliance as a Primary Challenge

The evolving regulatory framework is both a challenge and a growth driver for the BaaS industry.

As governments and regulatory bodies develop new digital banking and financial services frameworks, BaaS providers adapt to ensure compliance.

A study found that 60% of fintech companies cite regulatory compliance as their biggest challenge. American Bankers Association

Regulatory framework is critical because it impacts how BaaS providers operate and expand into new markets. BaaS companies that can navigate these regulations effectively will be positioned to thrive in the global financial ecosystem.

In Europe, the introduction of the PSD2 directive has tremendously impacted the BaaS industry by opening up banking data to third-party providers fostering innovation in digital payments and financial services.

84% of Banks Are Planning to Increase Their Fintech Partnerships by 2025

As the BaaS industry evolves, traditional banks increasingly partner with fintech companies to leverage their technology and innovation.

According to a PwC report, 84% of banks globally plan to increase their fintech partnerships by 2025.

These collaborations allow banks to offer cutting-edge services without developing new technology in-house. Partnerships between banks and fintech companies are crucial for driving innovation in the financial sector.

Banks gain access to the latest technology, while fintech companies benefit from the banks' established infrastructure and regulatory knowledge.

Goldman Sachs’ partnership with Apple to launch the Apple Card is a prominent example. The collaboration leverages Goldman Sachs’ BaaS platform to offer a seamless credit card experience within the Apple ecosystem.

90% of Banks Are Expected To Move to Cloud-Based Platforms by 2025

Cloud technology plays a pivotal role in the development of BaaS platforms, allowing for greater scalability, flexibility, and innovation. A report predicts that by 2025, 90% of banks will have moved to cloud-based platforms, driving the adoption of BaaS services. Cloud Zero

Cloud-based platforms enable faster deployment of services, reduce operational costs, and enhance the ability to scale. This shift is critical for BaaS providers, allowing them to offer their clients more efficient and cost-effective solutions.

Stripe, a primary BaaS provider, uses cloud infrastructure to power its global payment platform, allowing businesses of all sizes to integrate payments seamlessly into their applications. The company's cloud-based approach has enabled it to scale rapidly and support millions of businesses worldwide.

Key Challenges Facing the BaaS Industry

As the BaaS sector transform led by innovations, it face some limitations, such as:

Customer Trust and Adoption

Customer trust is another critical challenge facing the BaaS industry. Despite the growing popularity of digital banking and financial services, only 32% of consumers trust fintech companies with their financial data, according to a 2022 survey. The Financial Brand

This trust gap can be a barrier to the adoption of BaaS-powered services, particularly when it comes to handling sensitive financial information. Without customer trust, BaaS providers will struggle to scale their offerings.

Building trust requires a combination of strong security practices, transparent communication, and effective customer support. However, this is not easy, especially for new entrants without established reputations.

Robinhood faced serious trust issues after the 2021 GameStop trading fiasco, where it restricted trades on certain stocks. CNBC

Customer backlash underscored the importance of trust in the fintech industry and the challenges BaaS providers face in maintaining customer confidence.

Profitability and Monetization Concerns

While BaaS offers remarkable growth opportunities, profitability remains a challenge for many players in the industry.

The need to invest heavily in technology, security, and compliance often outweighs revenue generation, especially in the early stages.

The path to profitability for BaaS providers can be long and uncertain.

Many companies rely on external funding to sustain operations, but the current economic environment—with rising interest rates and reduced venture capital investment—poses a threat to their long-term sustainability.

Brex, a fintech unicorn, recently shifted its focus to profitability after years of prioritizing growth at all costs.

The company cut back on some of its services and laid off staff to focus on its core offerings, reflecting the broader industry challenge of balancing growth with profitability.

Legacy Infrastructure Integration

Traditional banks often face challenges integrating BaaS solutions with their legacy infrastructure.

A report found that 79% of banks struggle with the complexity of integrating modern BaaS platforms into their existing systems. PYMNTS

Legacy infrastructure, often built decades ago, lacks the flexibility and scalability required to support the innovative services provided by BaaS platforms. Integration issues can delay the time-to-market for new services and increase operational costs.

Banks that cannot modernize their infrastructure may struggle to compete with more agile fintech firms that can quickly adapt to new technologies.

JPMorgan Chase has invested billions in upgrading its IT infrastructure to better integrate with FinTech solutions and stay competitive in the digital banking space.

However, smaller banks without such resources may find it challenging to keep up with these demands, limiting their ability to adopt BaaS platforms effectively.

Security and Data Privacy Risks

As BaaS platforms handle sensitive financial data, they are prime cyberattack targets.

With global cybersecurity damages expected to reach $10.5 trillion annually by 2025, the BaaS industry faces increasing risks related to data breaches and financial fraud. Cybersecurity

Ensuring data privacy and security while complying with stringent regulations like GDPR and the California Consumer Privacy Act CCPA remains a top challenge. A single data breach can result in massive financial losses, legal consequences, and reputational damage for BaaS providers.

Given the sensitive nature of financial data, ensuring robust security measures is critical to gaining and maintaining customer trust.

In 2019, Capital One faced a massive data breach that affected over 100 million customers, exposing sensitive information such as Social Security numbers and bank account details. This breach highlighted the considerable risks of handling financial data and the need for stronger security protocols in the BaaS industry.

Emerging Opportunities in the BaaS Industry

As we look to the future, the BaaS sector offer opportunities to stakeholders, such as:

Partnerships With Traditional Banks

Partnerships between traditional banks and fintech companies create new opportunities for BaaS providers. According to a PwC survey, 82% of banks plan to partner with fintech companies to drive digital innovation and improve their customer offerings.

These partnerships allow banks to leverage fintechs' agility and technology while fintech companies gain access to the banks' infrastructure and customer base.

As traditional banks face increasing pressure to innovate and digitize their services, BaaS providers can act as intermediaries, enabling banks to offer new digital financial products without developing the technology in-house.

BBVA partnered with Uber to provide digital banking services in Mexico through a BaaS platform. This partnership allowed Uber to offer financial services to its drivers and customers.

At the same time, BBVA gained access to Uber's large customer base, showcasing the mutually beneficial nature of BaaS-powered partnerships.

Adoption of Artificial Intelligence in Financial Services

Artificial intelligence AI is transforming the financial services industry, and BaaS providers have an opportunity to incorporate these AI-driven tools into their platforms.

The AI market in fintech is projected to reach $1.24 trillion by 2025, according to MarketsandMarkets.

AI can enhance fraud detection, credit scoring, personalized recommendations, and customer support automation.

AI enables BaaS providers to offer advanced analytics and automation, which can help fintech companies and banks improve operational efficiency, reduce costs, and deliver more personalized services.

AI-powered BaaS platforms can also help with real-time decision-making and risk management.

OakNorth, a BaaS provider, uses AI to offer its banking partners advanced credit scoring and risk analysis tools.

By leveraging AI, OakNorth can provide more accurate assessments of small business credit risk, enabling its partners to offer tailored financial products to underserved markets.

Rise of Decentralized Finance DeFi as the DeFi Market Is Projected to Grow at a CAGR of 42.5% Through 2030

Decentralized finance DeFi is gaining momentum, presenting an emerging opportunity for BaaS providers to integrate blockchain technology and decentralized financial services into their platforms.

According to Allied Market Research, the DeFi market is expected to grow at a CAGR of 43.4% through 2032 as more users seek alternatives to traditional financial systems.

Why this opportunity matters: DeFi represents a new frontier in financial services, offering opportunities for BaaS providers to facilitate decentralized lending, borrowing, and payments.

By integrating DeFi protocols, BaaS platforms can cater to the growing demand for decentralized and peer-to-peer financial services.

BaaS provider Sila has integrated blockchain technology into its platform, allowing developers to build decentralized finance applications.

By offering tools to create DeFi solutions, Sila enables fintech companies to tap into the growing demand for blockchain-based financial services, such as decentralized lending and stablecoins.

Growth of Embedded Finance With the Embedded Finance Market Is Projected to Reach $7 Trillion by 2030

Embedded finance, which integrates financial services into non-financial platforms, is a key opportunity for BaaS providers. Bain & Company estimates that the transaction value of the embedded finance market could reach $7 trillion by 2026.

As more companies in sectors like e-commerce, healthcare, and transportation seek to offer financial services, BaaS platforms are well-positioned to enable this transition.

Embedded finance allows non-financial companies to enhance customer experience by directly integrating services like payments, lending, and insurance into their platforms. This creates a rich growth opportunity for BaaS providers to cater to a wider range of industries.

Shopify has successfully integrated BaaS to provide financial services to its merchants through Shopify Capital, which offers small business loans directly on the platform. This embedded finance solution allows merchants to access funding easily without leaving the Shopify ecosystem, demonstrating the power of BaaS in enabling new revenue streams for non-financial companies.

Impact on Stakeholders

The major growth in Banking-as-a-Service considerably impact various groups. Let me briefly outline how these drifts affect consumers, businesses, and investors:

Consumers:

- Increased access to financial services

- More personalized banking experiences

- Potentially lower fees due to increased competition

- Faster and more convenient digital banking solutions

Businesses:

- Opportunity to integrate financial services into their products

- Reduced barriers to entry in offering financial products

- Potential for new revenue streams through financial offerings

- Improved cash flow management and financial operations

Investors:

- New investment opportunities in fintech and BaaS providers

- Potential for high growth in the BaaS sector

- Disruption of traditional banking models, affecting existing investments

- Increased focus on regulatory compliance and cybersecurity

Conclusion

The emergence of Banking-as-a-Service has been remarkable.

From a niche concept in the early 2010s to a multi-billion dollar industry today, the sector has undergone remarkable transformation.

Today's financial space, characterized by widespread adoption across various industries and a growing ecosystem of providers, sets the stage for tomorrow's innovations.

Current data points to a compound annual growth rate of 26.6% from 2023 to 2029, suggesting that BaaS will become an increasingly integral part of the global financial infrastructure.

This trajectory underscores the importance of strategic partnerships and regulatory compliance for stakeholders.

As we stand at this crossroads, one thing is clear: the future of BaaS will be shaped by those who can innovate while navigating the complex interplay of technology, regulation, and customer expectations.