111 NE 1st ST

Miami, Florida 33132

USA

Embedded lending allows users to access loans seamlessly within the context of their activities, whether it's during an online purchase or within a mobile app.

This approach eliminates the stress and delay associated with visiting traditional financial institutions.

This article examines the statistics and trends driving the 19.6% growth of integrated lending services, enhancing credit accessibility, efficiency, and user experience.

Data Sources and Methodology

This article synthesizes data from diverse sources to provide a comprehensive overview of cryptocurrency trends. Our research process includes:

Data Collection:

- Primary sources: Industry survey and government database

- Secondary sources: Academic papers, reputable industry report

- Time frame: Data collected spans from 2022 to present

Key Data Providers:

Analysis Approach:

- Cross-referencing multiple sources to ensure accuracy

- Prioritizing the most recent data available

Limitations:

- The embedded lending market data can be volatile and subject to rapid changes

- Market dynamics in embedded lending can shift rapidly; readers should consider the publication date of this article.

Key Takeaways

- 56% of Gen Z and 55% of Millennials are willing to switch to providers offering embedded lending.

- The market is expected to grow from approximately $7.66 billion in 2024 to $45.74 billion by 2034 at a CAGR of 19.6%.

- BNPL is a significant component of embedded lending, with the market expected to grow at a 39% CAGR from 2021 to 2030.

- Embedded finance is gaining traction in the B2B sector, with 55% of non-financial businesses planning to offer financial services within the next two years.

Overview of Embedded Lending

Embedded lending emerged in the early 2020s, driven by the rapid advancement of technology and the need for seamless financial solutions.

It refers to the integration of lending services directly into non-financial platforms, allowing users to access loans without leaving the interface of their preferred applications.

Since its inception, embedded lending has experienced massive growth.

Key milestones include the widespread adoption of APIs, facilitating real-time credit assessments and instant loan approvals.

Today, the embedded lending market is characterized by its increasing integration into e-commerce, mobile apps, and various digital platforms.

Major players include fintech companies and traditional banks that partner with non-financial businesses to offer tailored lending solutions.

Influential factors such as data analytics and user-centric design continue to shape its trajectory.

The embedded lending market is projected to reach approximately $7.66 billion in 2024 and grow to around $45.74 billion by 2034. (Future Market insight)

It is crucial in enhancing financial inclusion and accessibility.

This makes it a key area of focus for businesses, consumers, and financial institutions looking to innovate and improve the borrowing experience.

Major Statistics

- The market size of embedded lending is projected to reach approximately $7.66 billion in 2024. (Future Market Insight)

- It is expected to grow to around $45.74 billion by 2034 at a compound annual growth rate (CAGR) of 19.6% from 2024. (Future Market Insight)

- A survey conducted by Visa found that 43% of consumers expressed strong interest in embedded lending solutions. (PYMNTS)

- 15% of respondents reported using embedded lending in the last 90 days. (The Finance Brand)

- 56% of Gen Z consumers and 55% of Millennials said they would switch to providers that offer embedded lending. (The Finance Brand)

- 37% of embedded lending users reported low credit limits as a pain point. (The Finance Brand)

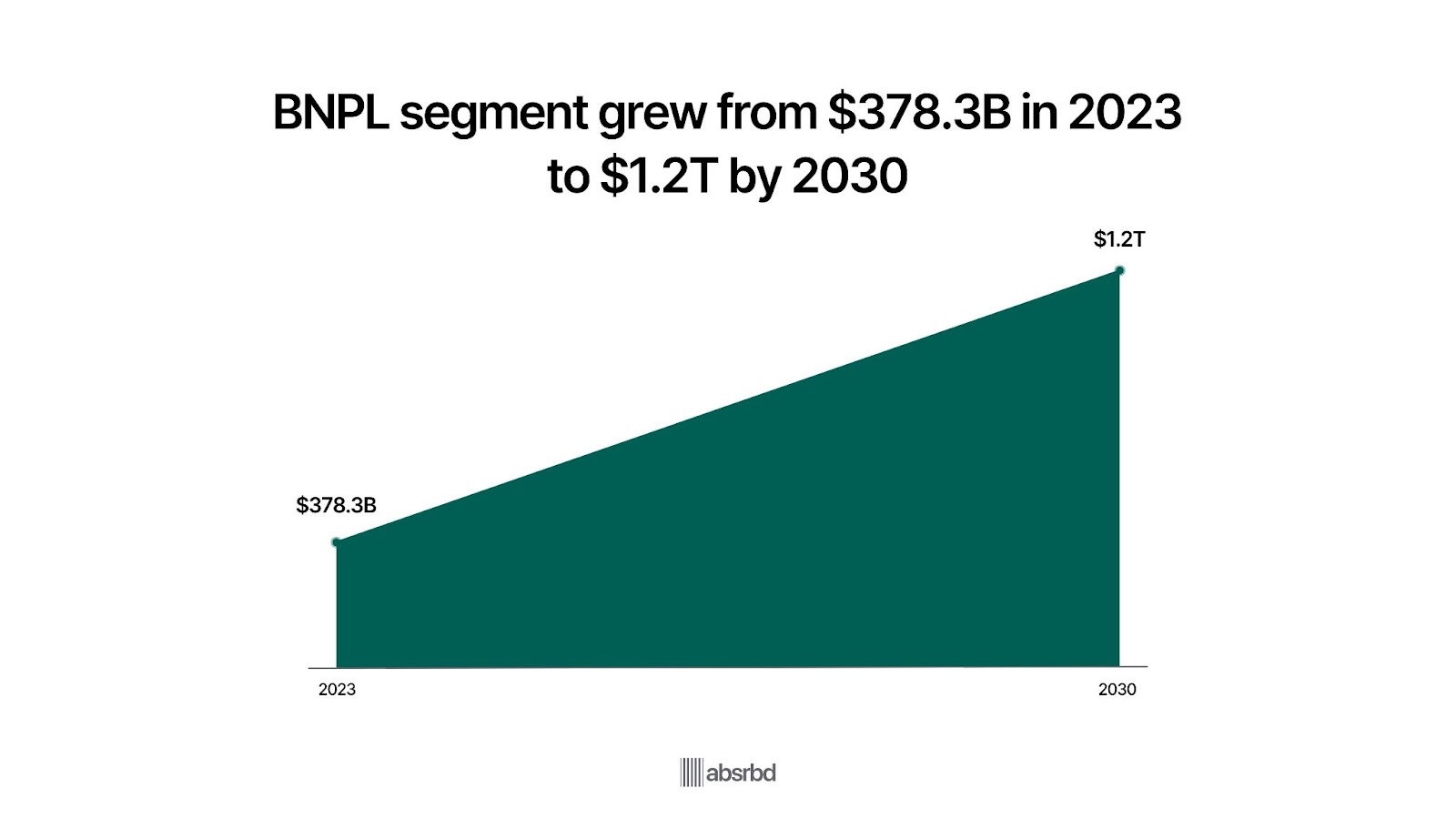

- The buy-now-pay-later (BNPL) segment, a prominent example of embedded lending, increased its user base from $378.3 billion in 2023 (GM Insight) to $1.2 trillion by 2030. (Lafferty)

- 29% of respondents said they prefer embedded lending options over other financing solutions for emergencies or unplanned costs.

- The BNPL user base increase from 52 million in 2020 to over 100 million in 2022. (Coherent Market Insight)

Major Trend

Growth of Buy Now, Pay Later (BNPL) with 20.7% Annual Growth Rate

The global Buy Now, Pay Later (BNPL) market is projected to grow at a 20.7% compound annual growth rate (CAGR) from 2024 to 2032. (Fortune Business Insight)

BNPL services, a major component of embedded lending, allow consumers to split payments into interest-free installments at the point of sale.

This trend is crucial as it provides instant credit access without traditional loans or credit cards.

It drives consumer spending and increases e-commerce conversion rates.

Leading BNPL providers like Klarna, Affirm, and Afterpay have expanded rapidly, with Klarna alone serving over 150 million users worldwide. (Business of App)

Digital Transformation Accelerates Customer Loyalty by 90% (Capterra)

The COVID-19 pandemic has accelerated the digital transformation across various sectors, leading to a surge in demand for embedded finance solutions.

This trend is important as it underscores businesses' need to adapt to changing consumer behaviors.

Post-pandemic, 90% of businesses utilizing embedded finance report improved customer loyalty, according to Capterra.

This statistic showcases how digital financial solutions are becoming essential for maintaining a competitive advantage in today's market.

Rise of Digital Wallets with 64% of Users Expecting Lending Features (Forbes)

Digital wallets are expanding to offer embedded lending services, with 64% of global digital wallet users expecting access to credit and lending features. (Forbes)

This trend is note-worthy because digital wallets are becoming an all-in-one financial solution, integrating payments, savings, and lending.

Companies like PayPal and Square have already embedded lending into their platforms, providing micro-loans to users and small businesses.

Shift Towards B2B Embedded Finance as 55% of Non-Financial Businesses to Offer Financial Services (Statista)

Embedded finance is increasingly recognized in the B2B sector, where companies are expected to provide integrated financial solutions as part of their service offerings.

This shift is notable because it reflects a growing expectation among businesses to streamline transactions and enhance operational efficiency.

As a result, 55% of non-financial businesses plan to implement embedded finance services within the next two years, indicating a substantial market opportunity. (Statista)

Key Challenges Facing the Embedded Lending Industry

Regulatory Ambiguity as 42% of Companies Face Unclear Compliance Requirements (American Banking Association)

The need for clarity regarding regulatory responsibilities poses a challenge for companies offering embedded lending services.

This trend is crucial as it can lead to compliance failures, resulting in legal repercussions and financial penalties.

Companies often struggle to determine who is accountable for regulatory compliance—the financial institution, the API provider, or the non-financial company.

As a result, 42% of companies report confusion about compliance requirements, which can hinder the growth of embedded lending solutions. (American Banking Association)

Data Security Concerns with 61% of Consumers Worry About Data Safety (The Banking Scene)

Data security is a paramount challenge for the embedded lending industry.

The integration of financial services into non-financial platforms increases the risk of data breaches and privacy violations.

This trend is remarkable because the trust of consumers is foundational to the success of embedded lending.

If consumers feel their data is insecure, they may avoid using these services altogether.

A survey revealed that 61% of consumers express concerns about data security when engaging with embedded finance solutions. (The Banking Scene)

This highlights the need for robust security measures to protect sensitive information.

Fintech Loans Twice as Likely to Default

Identifying customer risk is another critical challenge in embedded lending.

Compared to traditional banks that have access to comprehensive financial histories, many fintech companies need more data to accurately assess borrower risk. This leads to uniform lending terms being offered to all customers, regardless of their financial status.

Fintech loans show a higher risk of delinquency compared to conventional bank loans.

After 15 months, they are twice as likely to be delinquent, posing a risk for lenders in the embedded finance space. (The Financial Brand)

Complex commercial relationships as there’s increased confusion among consumers

The intricate commercial relationships arising from embedded lending can confuse consumers.

When financial services are embedded into non-financial platforms, customers may find it difficult to identify which entity is responsible for various aspects of the service.

This includes areas like loan servicing and customer support.

This complexity can lead to dissatisfaction and distrust, as consumers may not know whom to approach for complaints or issues.

A customer using a ride-sharing app that offers embedded lending might need clarification on whether to contact the app or the lending partner for assistance.

This could complicate the user experience.

Emerging Opportunities in Embedded Lending

SMBs as central players with 37% interested in embedded lending (PYMNTS)

Small and medium-sized businesses (SMBs) are increasingly becoming pivotal in the embedded lending landscape.

37% of SMBs express high interest in switching to providers that offer embedded lending options. (PYMNTS)

This trend is important because it reflects a growing demand for integrated financial solutions that enhance the customer experience and streamline purchasing processes.

By partnering with fintech companies, SMBs can tailor lending solutions to meet their needs, thus improving customer engagement and sales conversion rates.

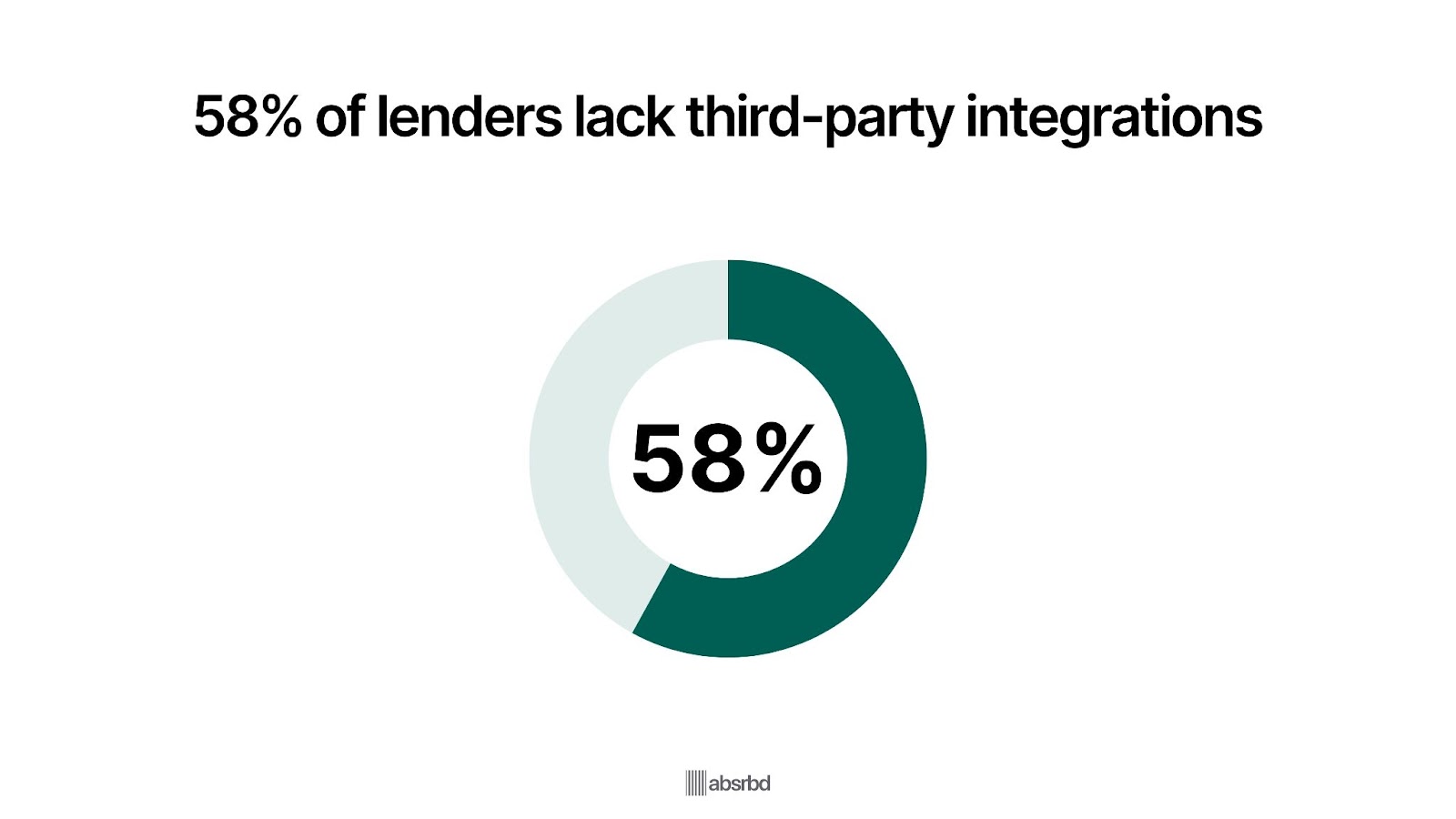

Technological Integration as 58% of Lenders Lack Third-Party Integrations (PYMNTS)

Despite the potential, approximately 58% of lenders serving consumers currently lack third-party platform integrations necessary for effective embedded lending.

This gap allows lenders to enhance their offerings by investing in technology that facilitates seamless integration with e-commerce platforms and payment systems.

Addressing this challenge is crucial as it can unlock new revenue streams and improve operational efficiency, enabling lenders to serve better.

Data-driven lending enhanced by AI

The rise of data analytics and machine learning is transforming how lenders assess creditworthiness in embedded lending.

Advanced data analysis allows lenders to make more informed lending decisions, particularly for underserved markets.

This trend is remarkable because it allows for more inclusive lending practices, enabling businesses and consumers with limited credit histories to access financing.

For instance, fintech companies are already utilizing these technologies to provide personalized lending solutions that cater to diverse customer profiles.

Personalization and Monetization

The advent of open finance, which enables the secure sharing of financial data between institutions, is unlocking new possibilities for embedded lending.

By leveraging the wealth of data available through open finance, lenders and businesses can offer highly personalized lending solutions tailored to individual customer needs.

This trend is important as it allows for more relevant and valuable services, ultimately leading to better customer experiences and increased revenue opportunities.

Appana from Finastra emphasizes that open finance leads to an open economy, and there are tremendous opportunities to monetize and provide the right services."

Impact on Stakeholders

The major trends in embedded lending are affecting various groups in the following ways:

Consumers:

- Embedded lending enables consumers to access financing seamlessly within their everyday digital experiences, such as e-commerce checkouts or mobile apps, improving their ability to make purchases or access funds.

- Embedded lending provides a frictionless application and approval process, allowing consumers to obtain credit quickly and conveniently without the traditional hassles of visiting a bank or filling out extensive paperwork.

- Embedded lending leverages data and algorithms to provide consumers with customized credit options tailored to their individual needs and creditworthiness.

- The ease and accessibility of embedded lending could lead some consumers to take on more debt than they can reasonably manage without appropriate financial education and safeguards.

Businesses:

- New revenue streams: Businesses, particularly those in non-financial sectors, can generate additional revenue by offering embedded lending options to their customers, often through partnerships with fintech companies or banks.

- Enhanced customer experience: Embedding lending capabilities within a business's digital platforms can improve the overall customer experience, increasing customer satisfaction and loyalty.

- Expanded customer base: Offering embedded lending can help businesses attract new customers who may have been previously excluded from traditional credit options.

- Risk management challenges: Businesses must carefully assess and manage the credit risk associated with embedded lending, as poor underwriting or high default rates could negatively impact their financial performance.

Investors:

- The growth of embedded lending is creating investment opportunities in fintech companies that are developing innovative lending solutions and partnerships.

- The increasing volume of embedded lending transactions could lead to the development of new types of asset-backed securities, providing investment opportunities for investors.

- Investors will likely focus on the risk management and underwriting practices of businesses and fintech firms engaged in embedded lending, as these factors can impact investment returns.

Conclusion

The embedded lending sector faces both challenges and opportunities.

While regulatory scrutiny and cybersecurity risks pose hurdles, the potential for seamless integration into diverse digital platforms remains crucial.

The rise of Banking-as-a-Service (BaaS) models illustrates this duality. Industry players navigating this landscape must prioritize compliance and robust security measures while innovating to meet changing consumer expectations.

Those who successfully balance risk management with user-centric design will likely capture larger market shares and establish strong brand loyalty.

As we look to the future, the ability to leverage AI to improve credit decisions and personalize offerings will separate the leaders from the followers in the world of embedded lending.

Ultimately, the sector's growth trajectory will depend on how effectively companies can address challenges while capitalizing on the vast opportunities presented by the digital economy.