.png)

111 NE 1st ST

Miami, Florida 33132

USA

Embedded payments are expected to reach $7 trillion in global transaction value by 2026, reshaping the financial sector. (PR Newswire)

This article explores essential statistics and events related to embedded payments.

We examine how payment services are seamlessly integrated into non-financial platforms, the growing role of fintech partnerships, and how these changes impact consumer behavior.

These driving forces are revolutionizing the way businesses and consumers interact with financial services, making payments more convenient, personalized, and efficient than ever before.

The embedded finance market is set to reach $588.49B by 2030 (32.8% CAGR). Embedded payments will hit $7T by 2026, with B2B payments reaching $2.6T and $6.7B in revenue.

Data Sources and Methodology

This article combines open-access resources and proprietary data to present accurate, up-to-date statistics and shifts on embedded payment.

Our methodology involves:

- Aggregating data from government databases, industry reports, and academic publications

- Incorporating exclusive insights from leading industry providers

- Regular updates to reflect the latest information

Key data providers include:

While we strive for accuracy, occurences in embedded payment are shifting rapidly.

These statistics reflect current patterns and should not be considered permanent facts.

Key Takeaways

- Embedded payments are expected to reach $7 trillion in global transaction value by 2026.

- The B2B embedded payment market is projected to reach $2.6 trillion by 2026, generating $6.7 billion in revenue.

- The global market for subscription-based payments is expected to hit $1.5 trillion by 2025.

- The rise in embedded payments has led to a 50% increase in cyberattacks.

- Digital wallets growing rapidly, with the global market expected to expand by 60% to $12 trillion by 2026

Overview of Embedded Payment

Embedded payments emerged in the early 2010s, driven by the rise of e-commerce and mobile applications.

It refers to the integration of payment processing directly into non-financial platforms, allowing users to complete transactions without leaving the application.

Since its inception, embedded payments have grown remarkably, with key milestones such as the introduction of one-click checkout systems marking major developments.

Today, the embedded payments market is characterized by a seamless user experience and increasing adoption across various industries.

Major players include companies like PayPal, Stripe, and Square, and consumer demand for convenience and speed continues to shape the industry's trajectory.

The embedded payments segment is estimated to have the largest market size within the embedded finance market, valued at $83.32 billion in 2023. (Grand View Research)

This growth highlights the crucial role embedded payments play in the digital economy, making it a key area of focus for businesses and financial institutions.

Key Statistics

- The embedded payment market is anticipated to surpass $138 billion by 2026. (Storms2)

- The embedded payments segment is estimated to have the largest market size within the embedded finance market, valued at $83.32 billion in 2023. (Grand View Research)

- The embedded finance market is expected to grow at a compound annual growth rate (CAGR) of 32.8% from 2024 to 2030, reaching $588.49 billion by 2030. (Grand View Research)

- Embedded business-to-business payments will reach $2.6 trillion by 2026, generating $6.7 billion in revenues for platforms and enablers. (Bain)

- By 2030, IDC predicts that 74% of global consumer payments will be processed by platforms owned by non-traditional financial service providers.

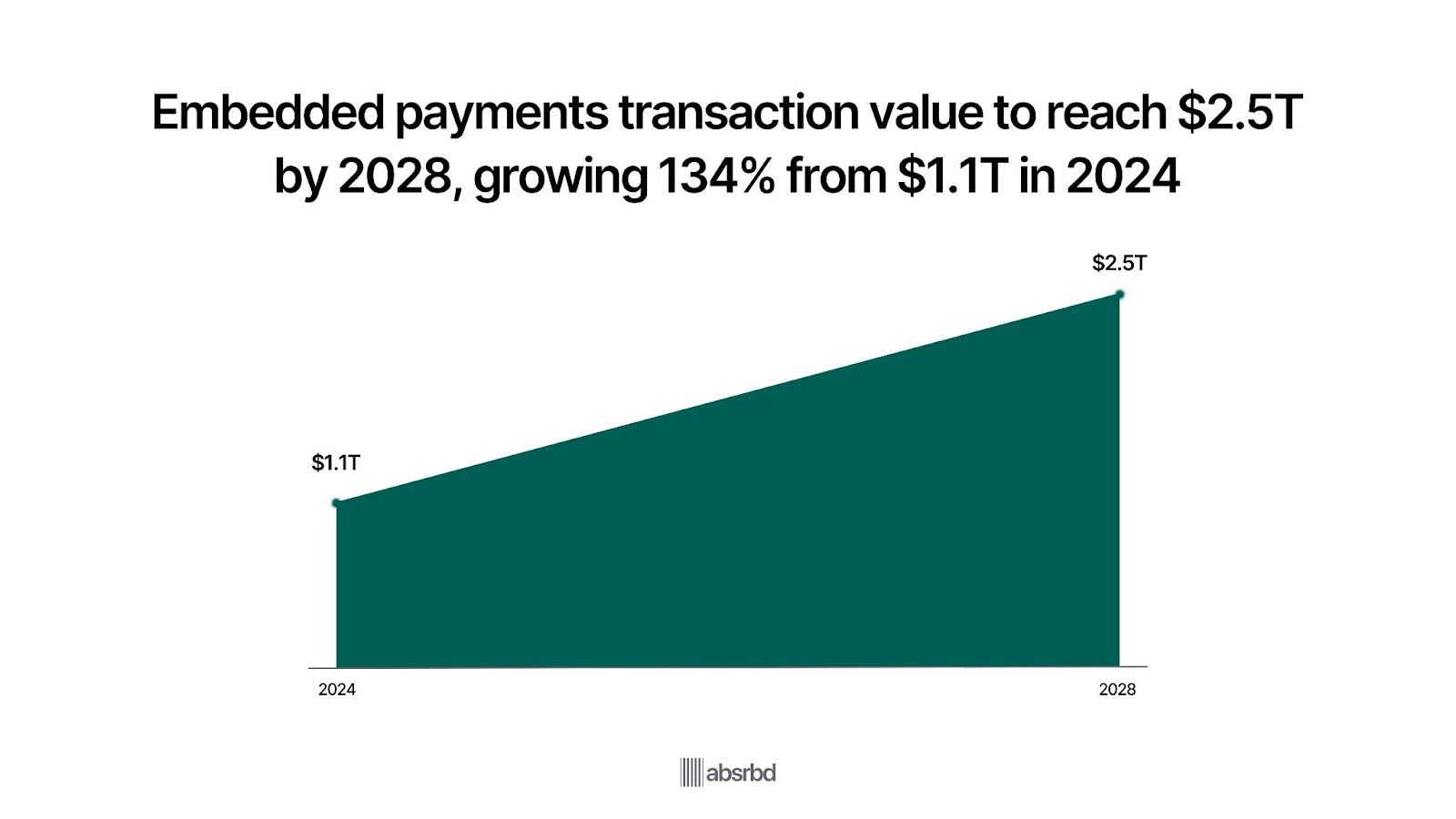

- The global transaction value from embedded payments will increase 134% by 2028, from $1.1 trillion in 2024, reaching 2.5 trillion. (Juniper Research)

- Embedded payments are expected to facilitate 21 billion one-click checkout experiences. (Juniper Research)

- A recent Pathward survey found that 82% of U.S. executives plan to implement embedded within the next two years.

Major Trends

Embedded payments are becoming increasingly popular as businesses and consumers seek more seamless, integrated payment experiences.

These trends are transforming how payments are made across industries, from e-commerce to mobility services, driving the growth and evolution of embedded payments:

Surge in Digital Wallet Adoption with 60% projected Growth by 2026

Digital wallets are on the rise, with the global market projected to grow by 60% to $12 trillion by 2026. (Juniper Research)

Consumers increasingly prefer wallets like Apple Pay and Google Pay for their seamless and secure payments across apps and platforms.

This is meaningful because it reduces friction in transactions, making checkout quicker and more convenient.

For example, Starbucks attributes over 30% of its U.S. sales to embedded digital wallet payments. (Geek Wire)

The expansion of embedded finance in non-financial apps is projected to reach $588.49 billion by 2025.

Non-financial apps, from ride-sharing to e-commerce, are integrating embedded payments, and this sector is expected to reach $588.49 billion by 2030. (Grand View Research)

The convenience of paying directly within the app—such as Uber's automatic fare payment—enhances user experience, creating a more streamlined financial ecosystem.

This is remarkable as it opens new revenue streams for non-financial companies while making transactions more efficient for consumers.

Embedded B2B payments are expected to surpass $2.6 trillion by 2026.

Embedded business-to-business (B2B) payments are also experiencing major growth, with projections indicating they will reach $2.6 trillion by 2026. (Bain)

This underscores the value embedded payments bring to the B2B space, enabling more efficient and streamlined business transactions.

As companies seek to optimize their financial processes and reduce friction, embedded B2B payments offer a compelling solution.

The $6.7 billion in revenue that embedded B2B payments are expected to generate for platforms and enablers by 2026 further emphasizes the commercial potential of this course. (Bain)

Expansion of Subscription-based payments as it is projected to hit $1.5 trillion by 2025

Subscription-based services are booming, with the global market expected to hit $1.5 trillion by 2025. (Forbes)

Platforms like Netflix, Spotify, and Adobe lead this shift by embedding recurring payments directly into their ecosystems.

This is vital because it encourages customer loyalty while automating revenue streams.

Over 60% of U.S. households now use multiple subscription services, driven by the ease of embedded payments. (Forbes)

Key Challenges in the Embedded Payment Industry

The embedded payment industry, while rapidly growing and innovating, faces several key challenges as it seeks to offer seamless, secure, and efficient payment experiences.

These challenges affect both businesses implementing embedded payment solutions and consumers using them. Here are the primary challenges in the industry:

Merchant Adoption of Embedded Payments Remains Low at 5%

Despite the outstanding growth projections, merchants' adoption of embedded payments remains relatively low, with only 5% currently offering embedded payment options. (Storm2)

This presents both challenges and opportunities for the industry.

Barriers to adoption may include technological complexity, regulatory concerns, or a lack of awareness.

As the industry matures, addressing these challenges and driving merchant adoption will be crucial for realizing the full potential of embedded payments.

Data Security Concerns with a 50% Rise in Cyberattacks

With the rise in embedded payments, data security has become a top challenge as cyberattacks have increased by 50% over the last year. (Purple Sec)

As companies handle more sensitive payment data, they become prime targets for hackers.

This is important because breaches can lead to financial losses, consumer distrust, and regulatory penalties.

For instance, the 2019 Capital One data breach impacted over 100 million customers, underscoring the importance of robust security measures.

Managing Payment Method Diversity

Supporting a wide range of payment methods, including credit cards, digital wallets, and bank account payments, to cater to a diverse customer base can be both technically and operationally challenging.

Each payment method has unique requirements that must be addressed, from integration to fraud prevention.

Businesses must strike a balance between offering a broad selection of payment options and maintaining a streamlined user experience.

Failure to manage payment method diversity effectively can lead to customer frustration and abandoned transactions.

Adapting to Evolving Customer Preferences and Technological Advancements

The embedded payments industry is rapidly developing, driven by changing customer preferences and technological advancements.

Businesses must stay agile and adaptable to keep pace with these changes, which may require ongoing investments in technology, staff training, and process optimization.

Failure to adapt can lead to outdated systems, customer dissatisfaction, and lost market share.

Successful businesses in the embedded payments industry will be those that can anticipate and respond to industry drifts and customer needs.

Emerging Opportunities in Embedded Payments

The embedded payments industry is poised for considerable growth, with numerous emerging opportunities shaping the future of financial transactions.

Here are some of the key opportunities in this rapidly expanding space:

Expansion into New Industries and Markets

As embedded payments continue to gain traction, there is a vast opportunity for expansion into new industries and markets traditionally underserved by traditional financial services.

This includes sectors like healthcare, education, and the gig economy, where embedded payments can streamline transactions and enhance user experiences.

Personalization and Customization

With the increasing adoption of artificial intelligence and machine learning, embedded payments are becoming more personalized and customized to individual user preferences.

This opens up opportunities for businesses to offer tailored payment experiences, such as one-click payments, subscription models, or pay-per-use services, further enhancing customer engagement and loyalty.

Increased Financial Inclusion

Embedded payments have the potential to drive greater financial inclusion by providing access to financial services for underserved populations.

By integrating payment capabilities into everyday platforms and applications, embedded payments can reach individuals who may not have had access to traditional banking services, enabling them to participate in the digital economy.

Collaboration with Fintechs and Non-Financial Brands

As embedded payments continue to boom, there is a growing opportunity for collaboration between traditional financial institutions, fintechs, and non-financial brands.

By partnering with fintechs, banks can leverage cutting-edge technologies and innovative solutions to enhance their payment offerings.

On the other hand, non-financial brands can integrate payment capabilities into their platforms, creating new revenue streams and strengthening customer relationships.

Adoption of Emerging Technologies

The embedded payments industry is poised to benefit from adopting emerging technologies such as blockchain, quantum computing, and 5G.

These technologies have the potential to enhance security, speed, and scalability, making embedded payments even more attractive to businesses and consumers alike.

As these technologies mature and become more widely adopted, they will create new opportunities for innovation and growth in the embedded payments space.

Impact on Stakeholders

Embedded payments are substantially impacting various groups in different ways.

Let me break down the effects on consumers, businesses, and investors:

Consumers:

- Payments are seamlessly integrated into apps and services, reducing friction in transactions.

- Smoother checkout processes and fewer steps to complete Tailored offers and recommendations based on payment data.

- Potential privacy concerns as more data being collected and shared across platforms.

Businesses:

- Smoother transactions can lead to higher conversion rates and customer satisfaction.

- Opportunities to monetize payment data and offer value-added services.

- Lower transaction fees compared to traditional payment methods.

- Faster settlement times and real-time payment processing.

- Need for technical expertise and potential integration issues.

Investors:

- New investment opportunities

- Potential for high returns as the sector expands rapidly.

- Opportunity to invest in various sectors adopting embedded payments.

- Risks as regulatory changes and market saturation as the field becomes more competitive.

Financial Institutions:

- Traditional banks need to adapt to remain competitive.

- Collaborations with fintech companies and other businesses.

- As payments become more integrated into other services.

Regulators:

- To address new payment models and protect consumers.

- Ensuring new payment methods are safe and comply with anti-money laundering laws.

Technology Providers:

- Increased demand for payment integration solutions and APIs.

- Need to continuously innovate to stay ahead in a rapidly growing market.

Conclusion

The developments in digital wallet usage and embedded payments have far-reaching implications for various stakeholders.

For consumers, the increasing adoption of digital wallets offers greater convenience and enhanced security in transactions.

Meanwhile, businesses must contend with the challenge of integrating these payment systems while ensuring a seamless customer experience.

These shifts are driving a reevaluation of payment processing strategies across industries.

Moving forward, success in this space will hinge on user experience and security enhancements.

Those who prioritize innovation and customer engagement will be best positioned to thrive in the maturing world of digital payments.