111 NE 1st ST

Miami, Florida 33132

USA

A decade ago, investing meant working closely with financial advisors, relying on their expertise and human intuition.

Today, digital platforms and algorithms are transforming the sector.

This article dives into the dramatic shift in this $8.01 billion market, showcasing how AI-driven investment tools are transforming how people approach investing and personal finance, making wealth management more accessible, affordable, and efficient.

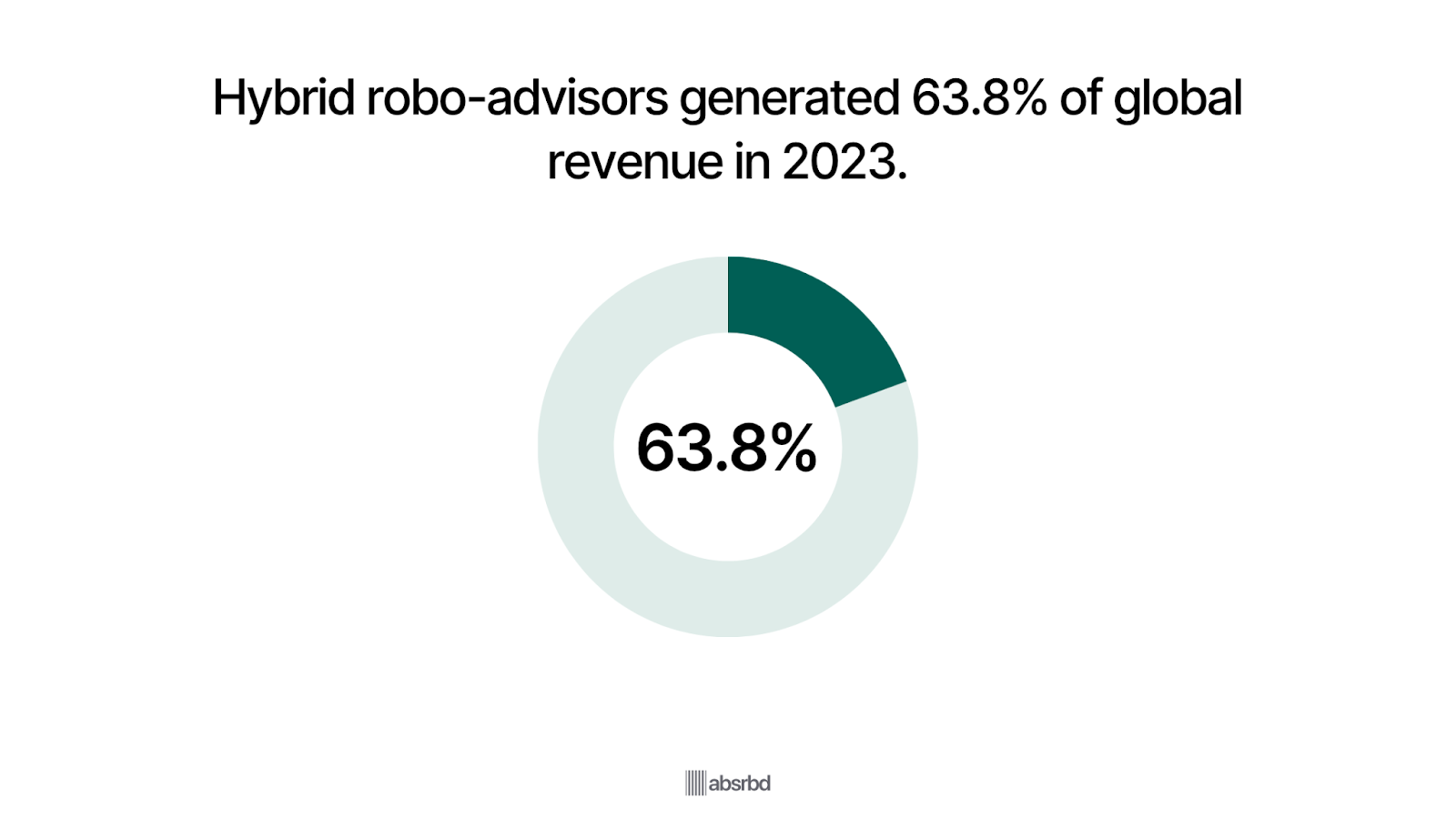

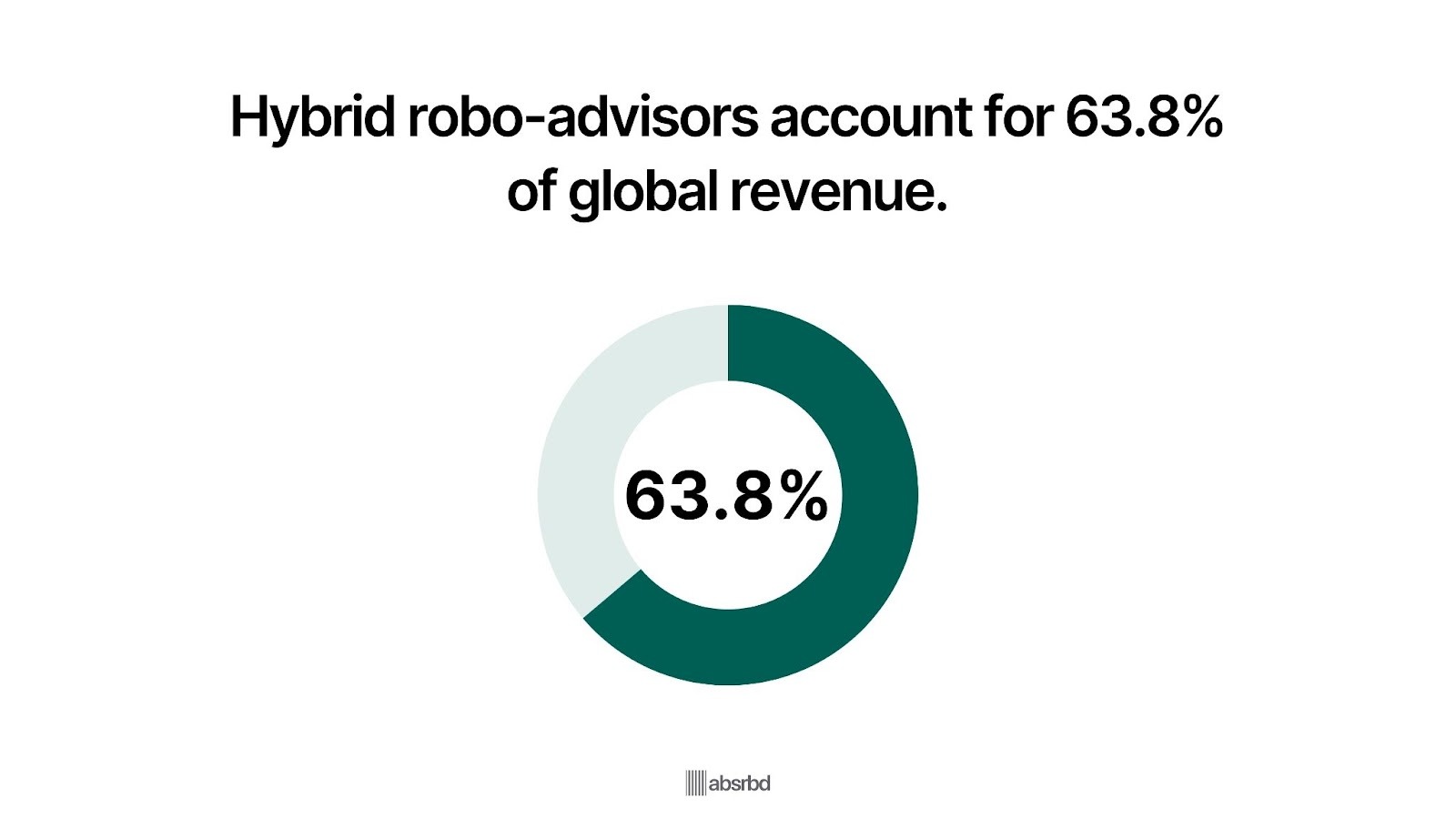

The Robo-Advisor market is projected to soar from $8.01 billion in 2024 to $33.38 billion by 2030 at a 26.71% CAGR.With hybrid robo-advisors leading with 63.8% revenue share.

Data Sources and Methodology

This article combines open-access resources and proprietary data to present accurate, up-to-date statistics and trends on robo-advisors.

Our methodology involves:

- Aggregating data from government databases, industry reports, and academic publications

- Incorporating exclusive insights from leading industry providers

- Regular updates to reflect the latest information

Key data providers include:

While we strive for accuracy, trends in robo-advisors are shifting rapidly.

These statistics reflect current patterns and should not be considered permanent facts.

Key Takeaway

- The global robo-advisor market was valued at approximately $7.39 billion in 2023.

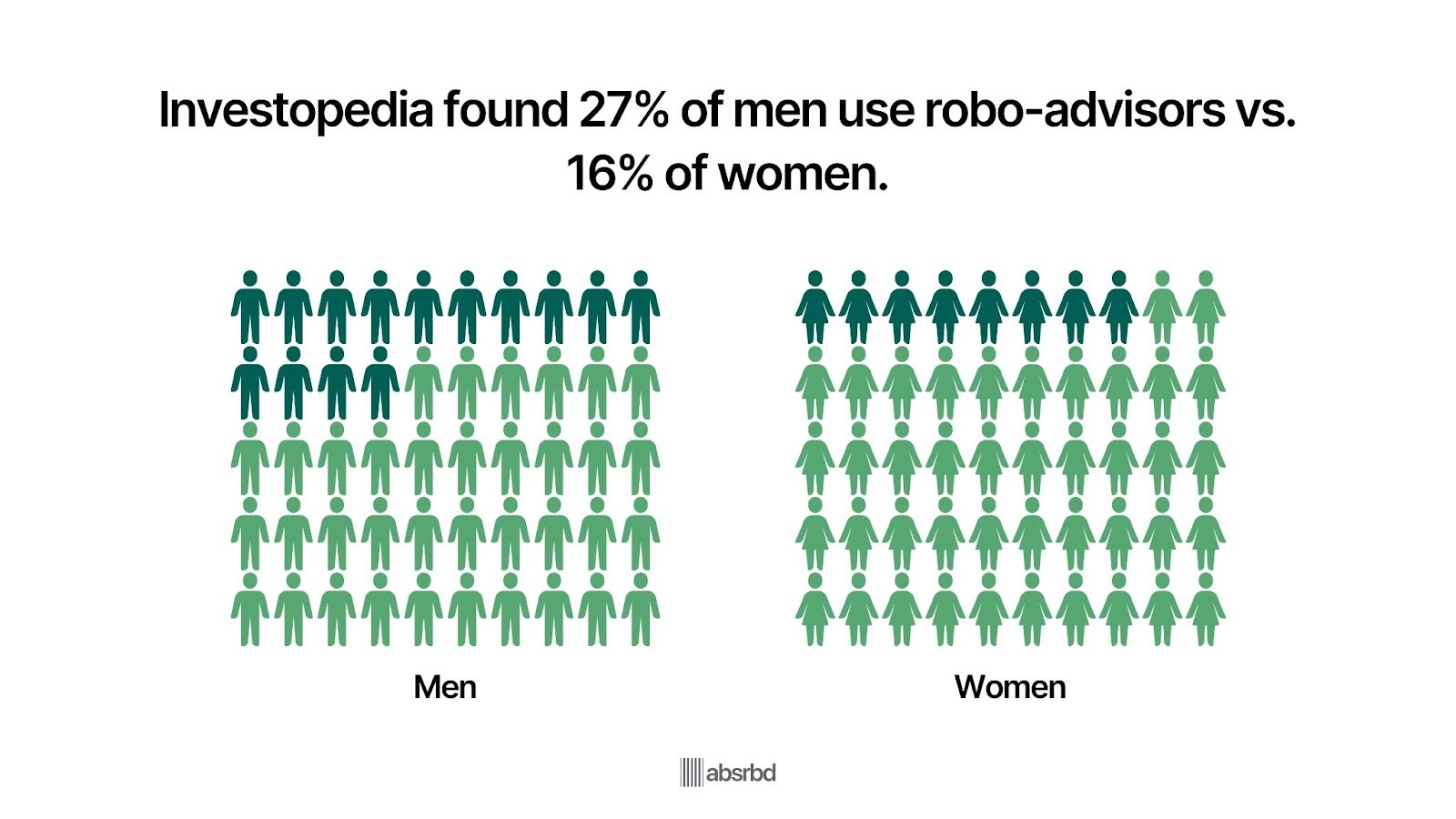

- 27% of male respondents use robo advisor versus 16% of women.

- The number of users is expected to amount to 34.130m users by 2028.

- Hybrid robo-advisors dominate the market, accounting for 63.8% of the global revenue of Robo-advisors.

- The United States takes the lead with the highest assets under management.

Overview of Robo-Advisors

Robo-advisors emerged in the early 2010s, driven by technological advancements and a growing demand for accessible investment solutions.

They refer to digital platforms that provide automated, algorithm-driven financial planning and investment services, typically with little human intervention.

Since their inception, robo-advisors have experienced exponential growth.

Key milestones include launching major platforms like Betterment and Wealthfront, which popularized the concept of automated investing.

Today, the robo-advisory market is characterized by a diverse range of services that cater to both novice and experienced investors.

Major players include Betterment, Wealthfront, and Vanguard, while factors such as increasing investor awareness and the demand for low-cost investment solutions continue to shape its trajectory.

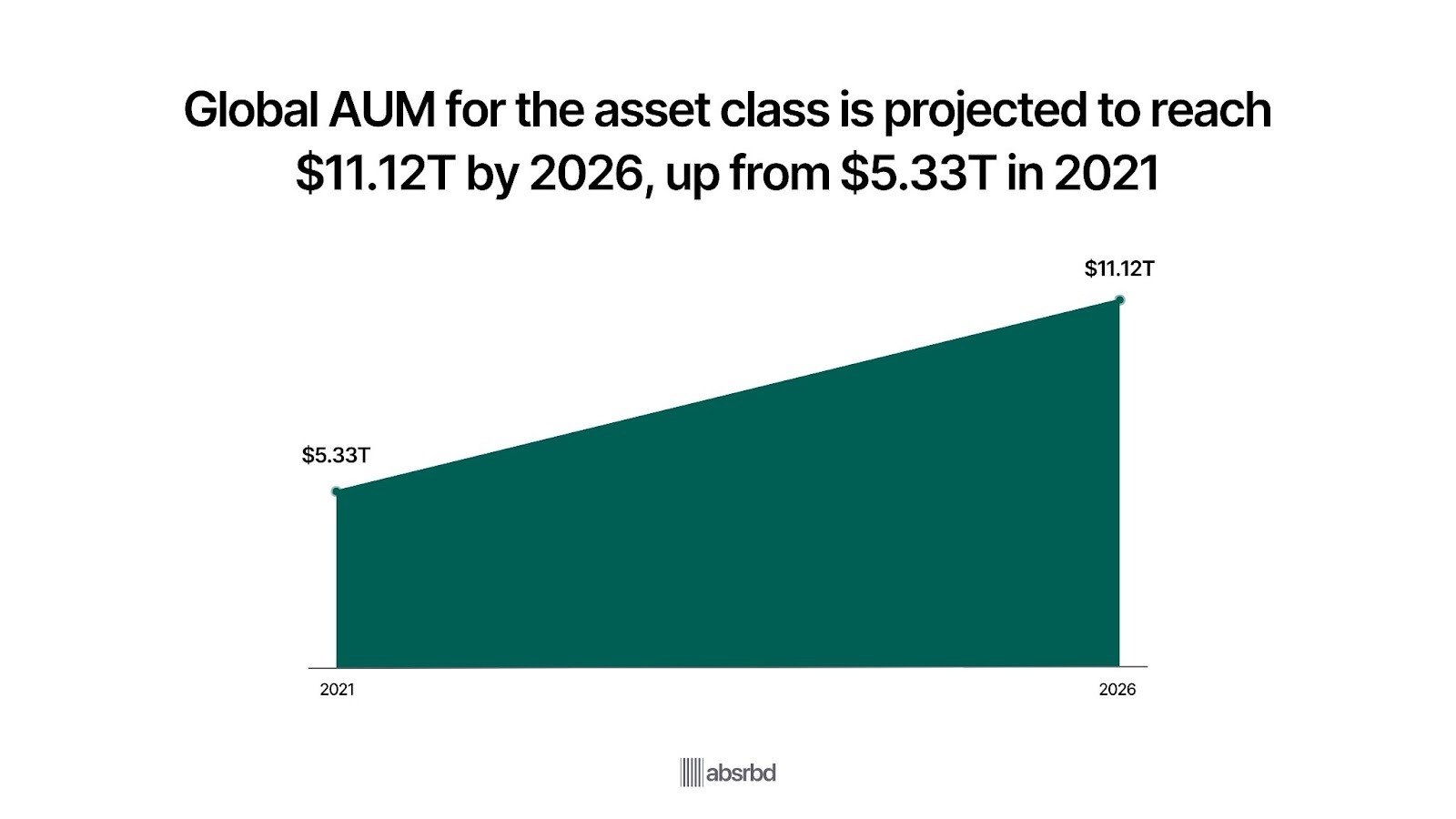

Global Asset Under Management (AUM) for the asset class is forecast to increase to $11.12 trillion in 2026 from an estimated $5.33 trillion at the end of 2021 S&P Global.

This makes them a key area of focus for individual investors, financial institutions, and regulators alike as they seek to navigate the dynamic world of digital finance.

Major Statistics

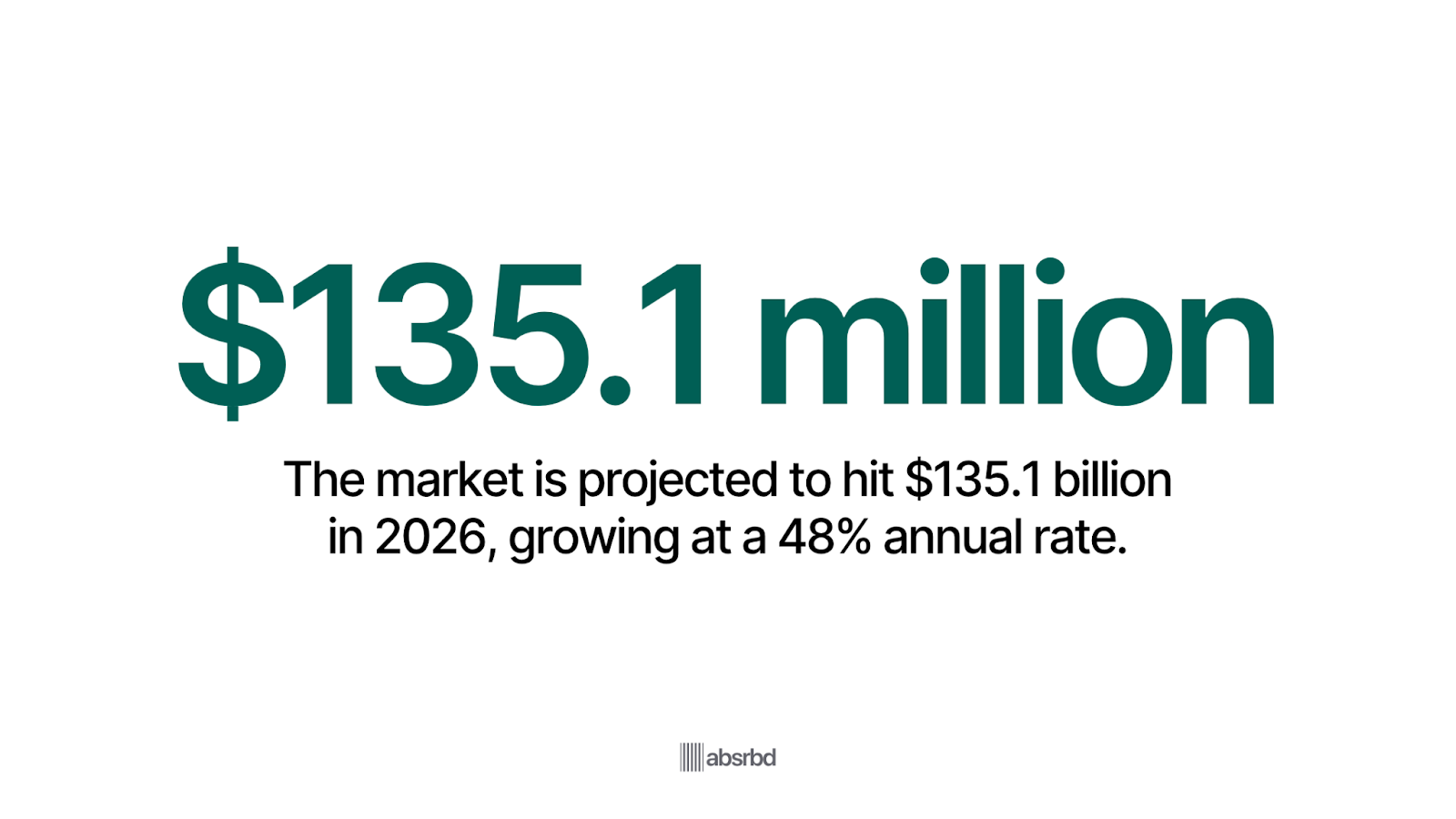

- The market is expected to reach $135.11 billion in 2026 at a CAGR of 48.08%. Yahoo Finance

- The global robo-advisor market was valued at approximately $7.39 billion in 2023. Polaris Market Research

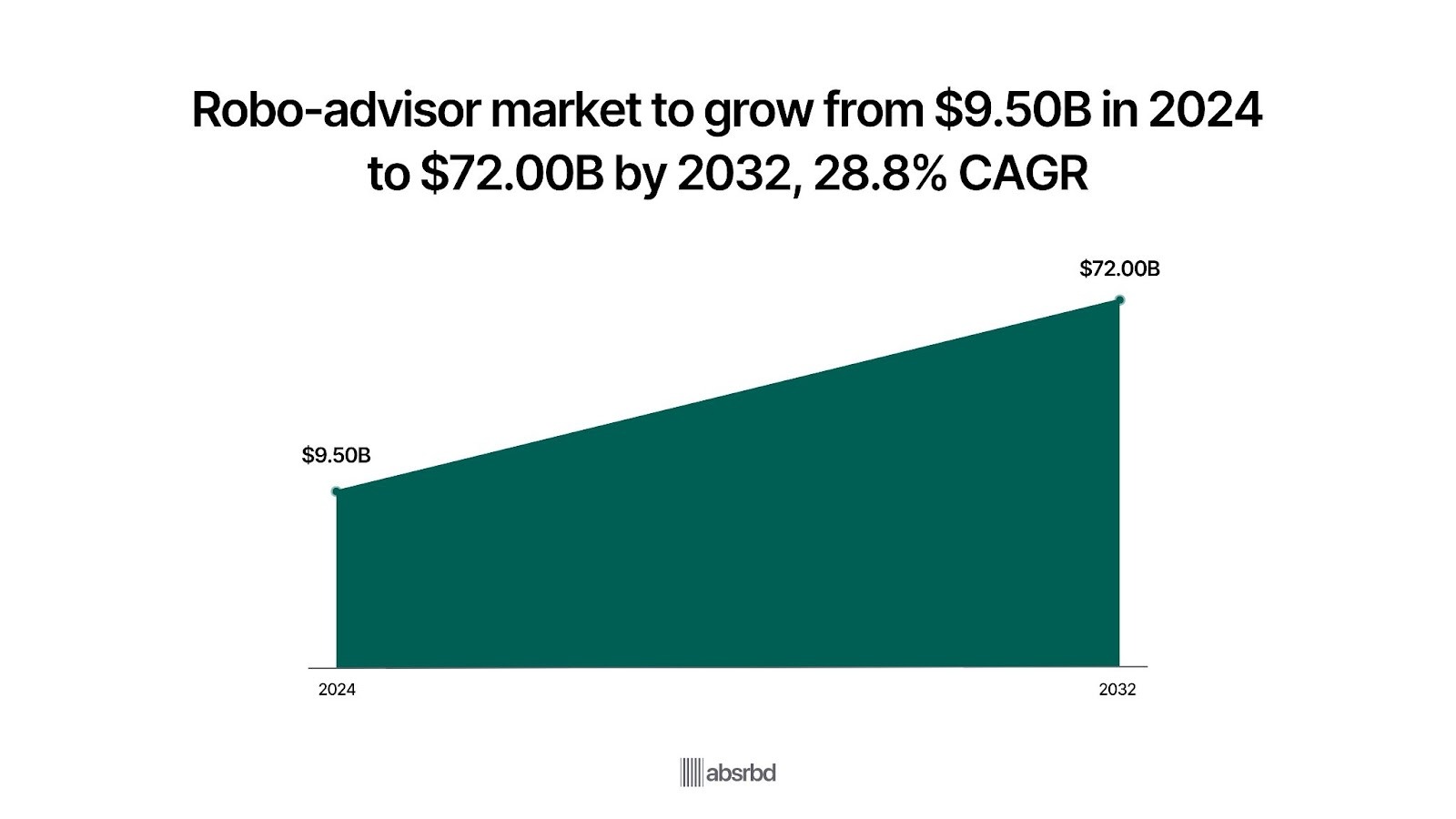

- The market is anticipated to grow from $9.50 billion in 2024 to $72.00 billion by 2032, exhibiting a compound annual growth rate CAGR of 28.8%. Polaris Market Research

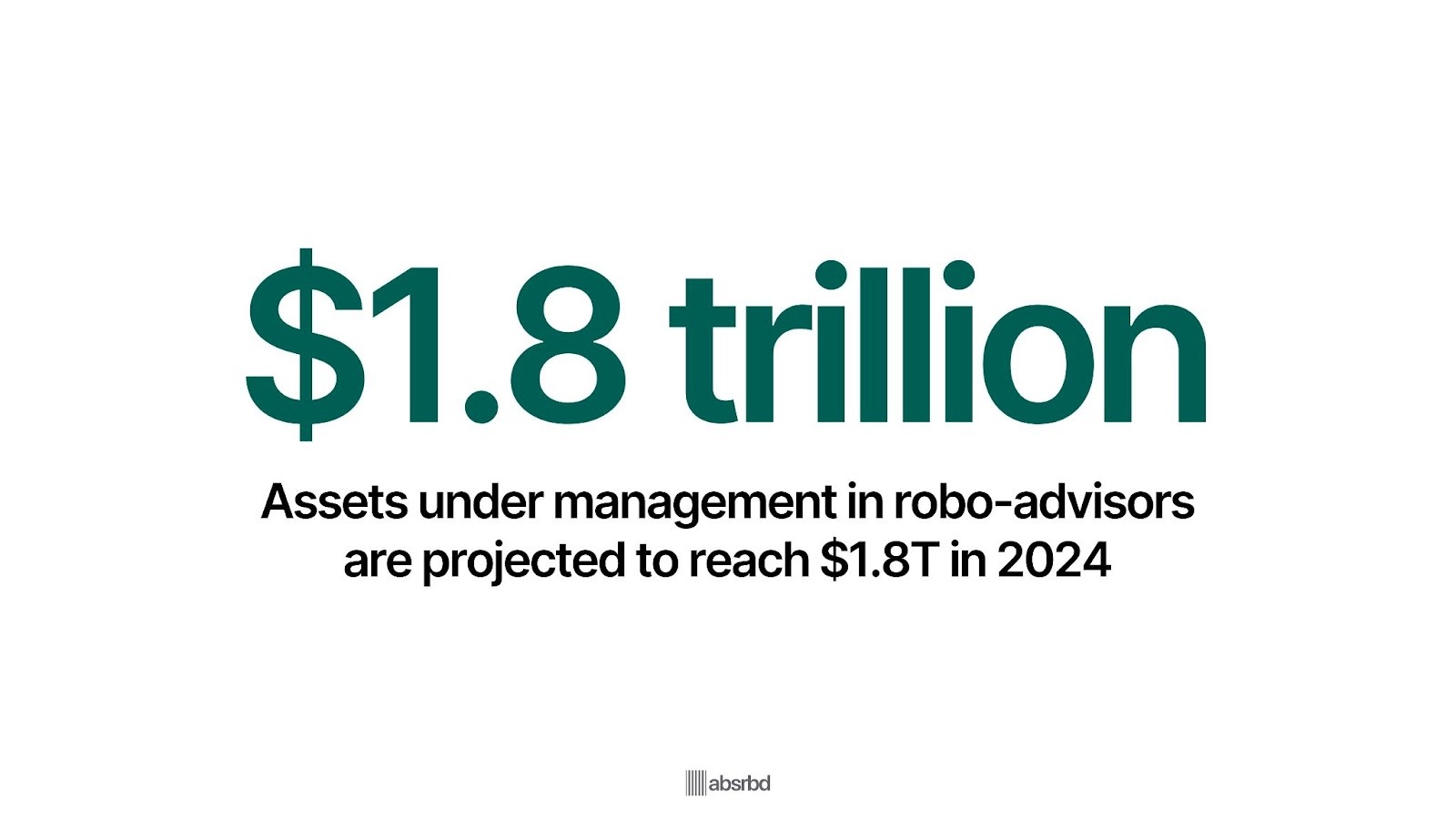

- Assets under management in the Robo-Advisors market are projected to reach $1.8 trillion in 2024. Statista

- Hybrid robo-advisors accounted for 63.8% of global robo advisory revenue in 2023. Grand View Research

- Robo-advisory platforms globally manage over USD 1.0 trillion in assets as of 2025. CoinLaw

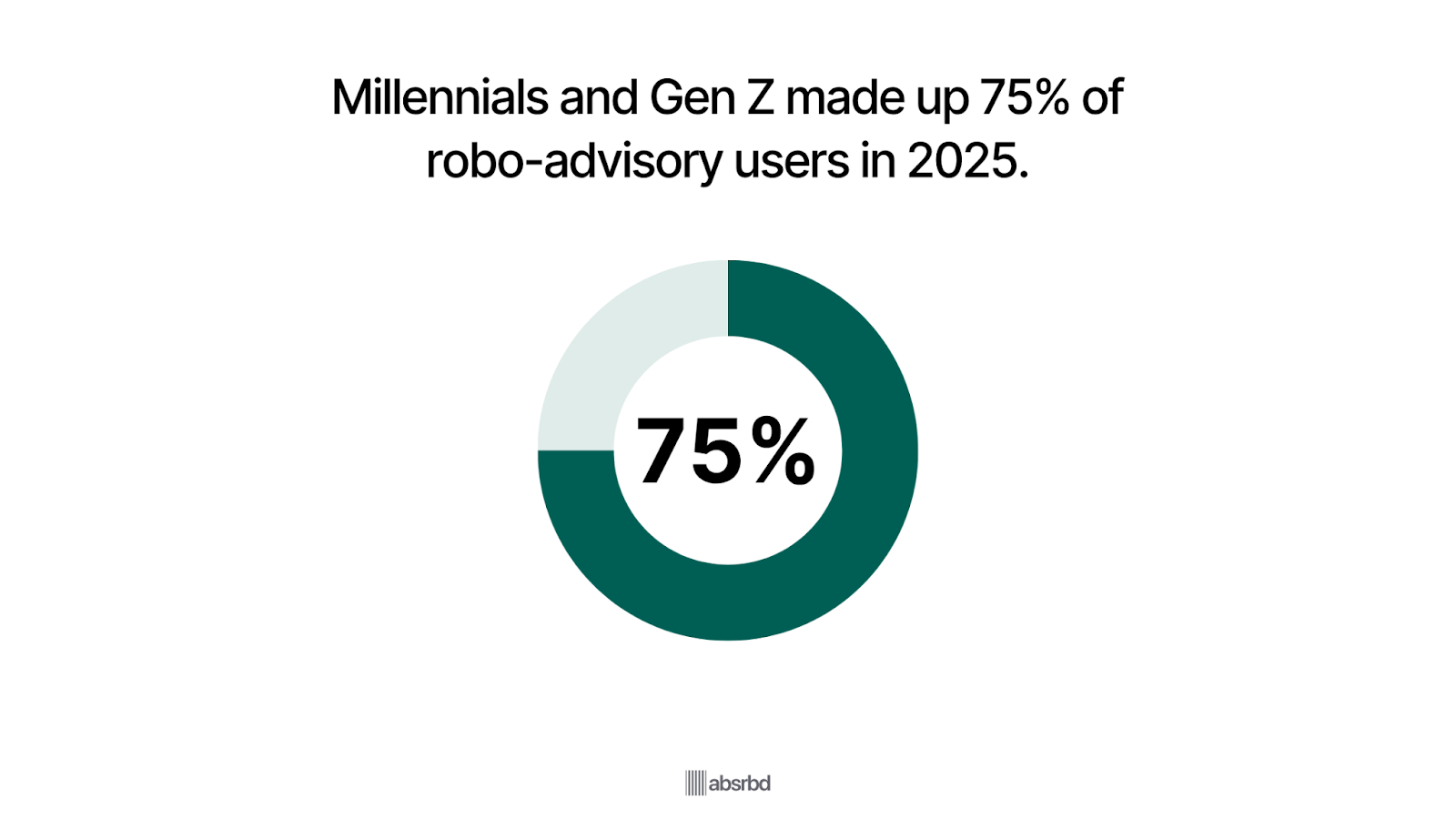

- Millennials and Gen Z made up about 75% of robo-advisory users in 2025. CoinLaw

- Robo-advisors are projected to manage about USD 2.06 trillion in assets under management AUM globally in 2025. Statista

- Users are expected to reach 34.05 million by 2029 in the global robo-advisor market. Statista

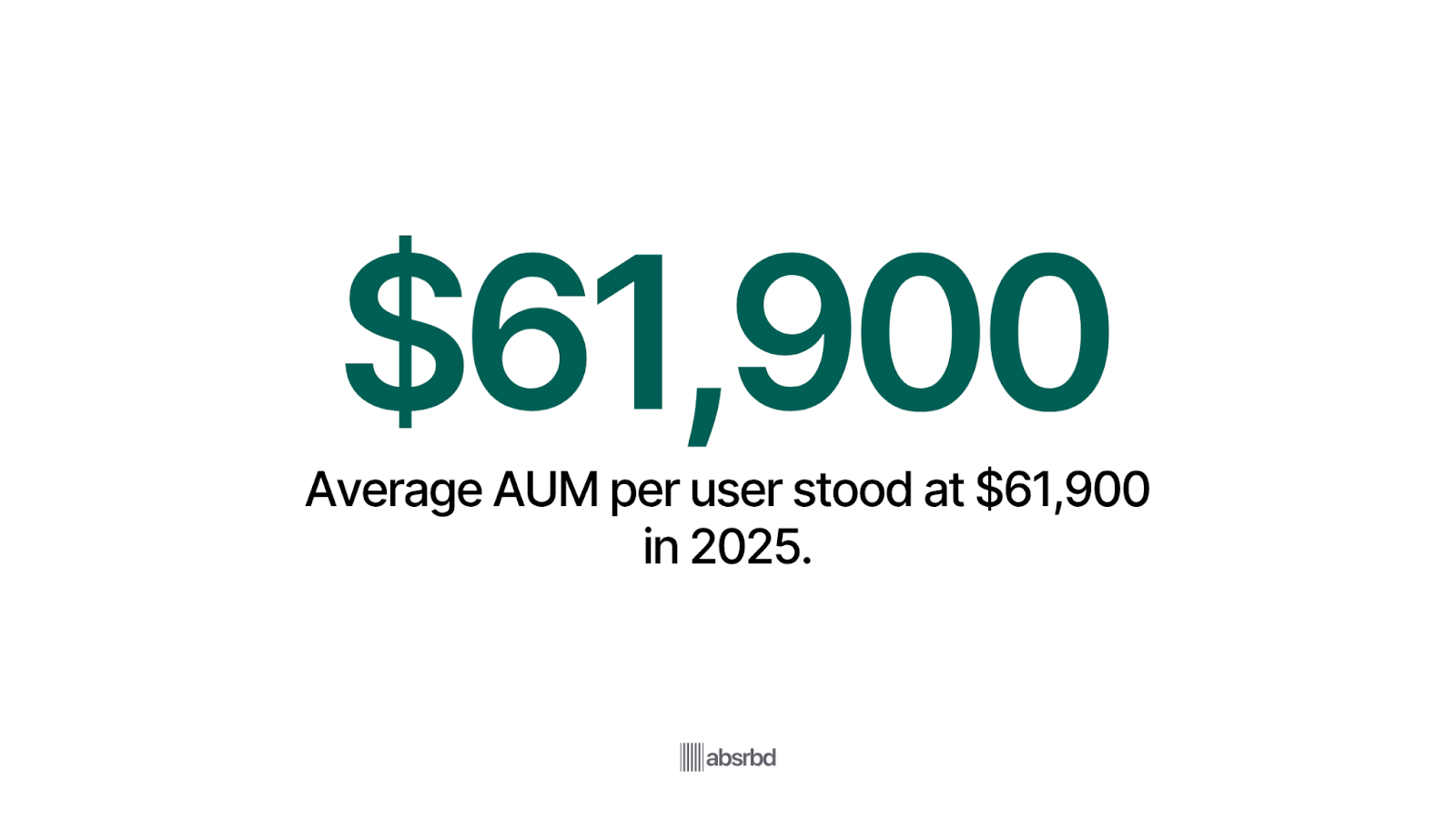

- The average AUM per robo-advisor user is forecast at USD 61,900 in 2025.Statista

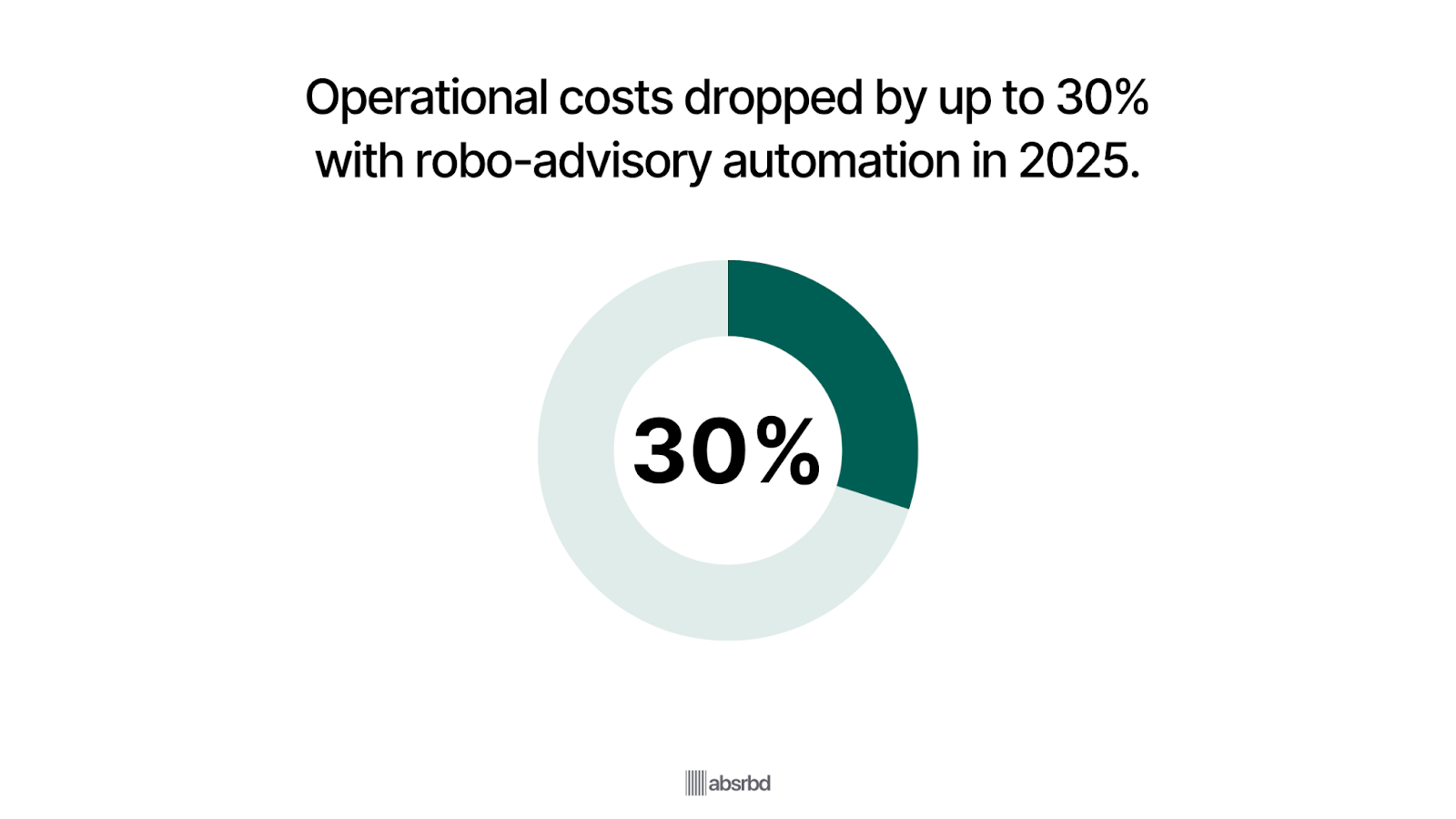

- Robo-advisory platforms cut operational costs by up to 30% in 2025. CoinLaw

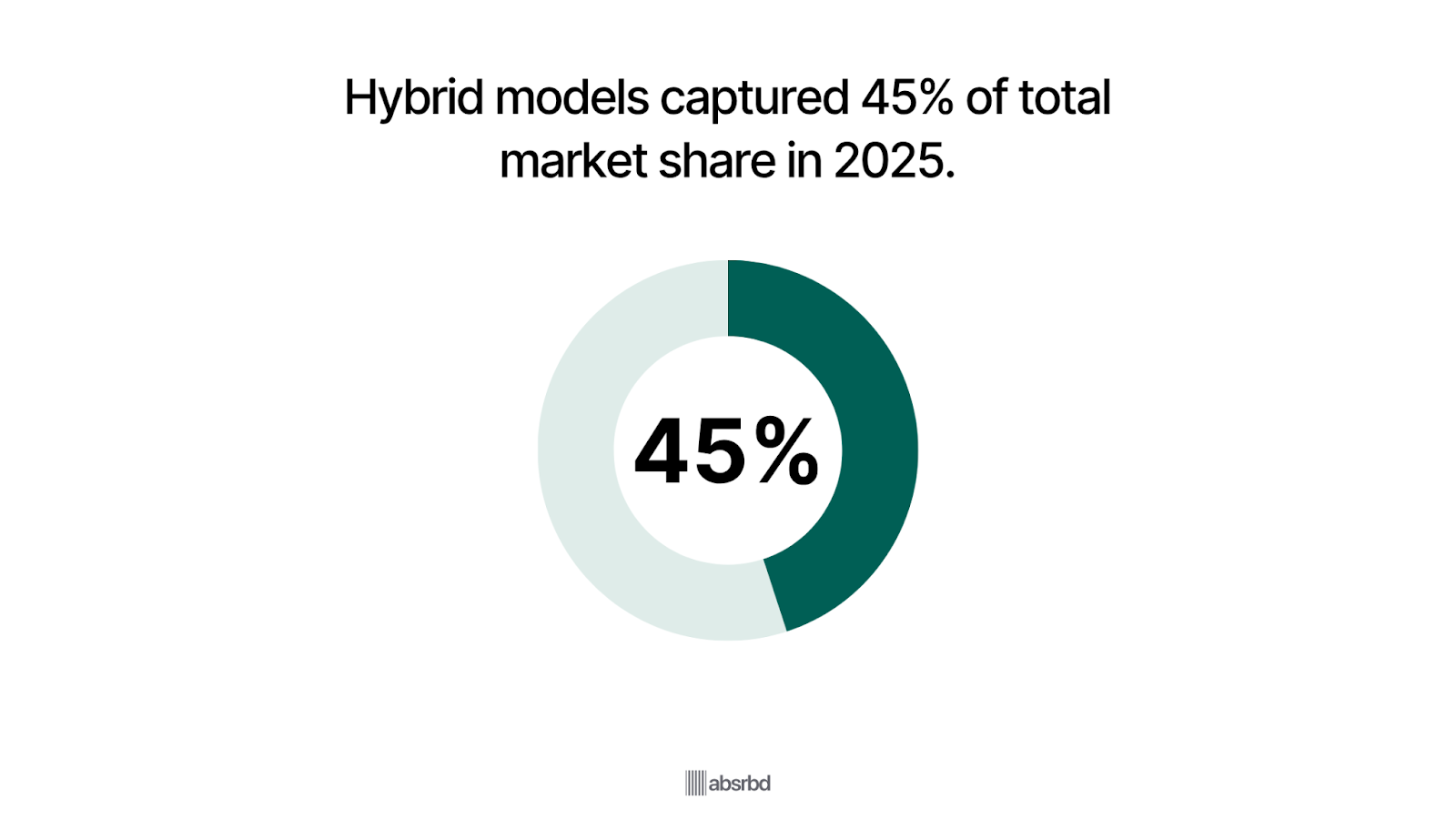

- In 2025, hybrid robo-advisors captured 45% of market share. CoinLaw

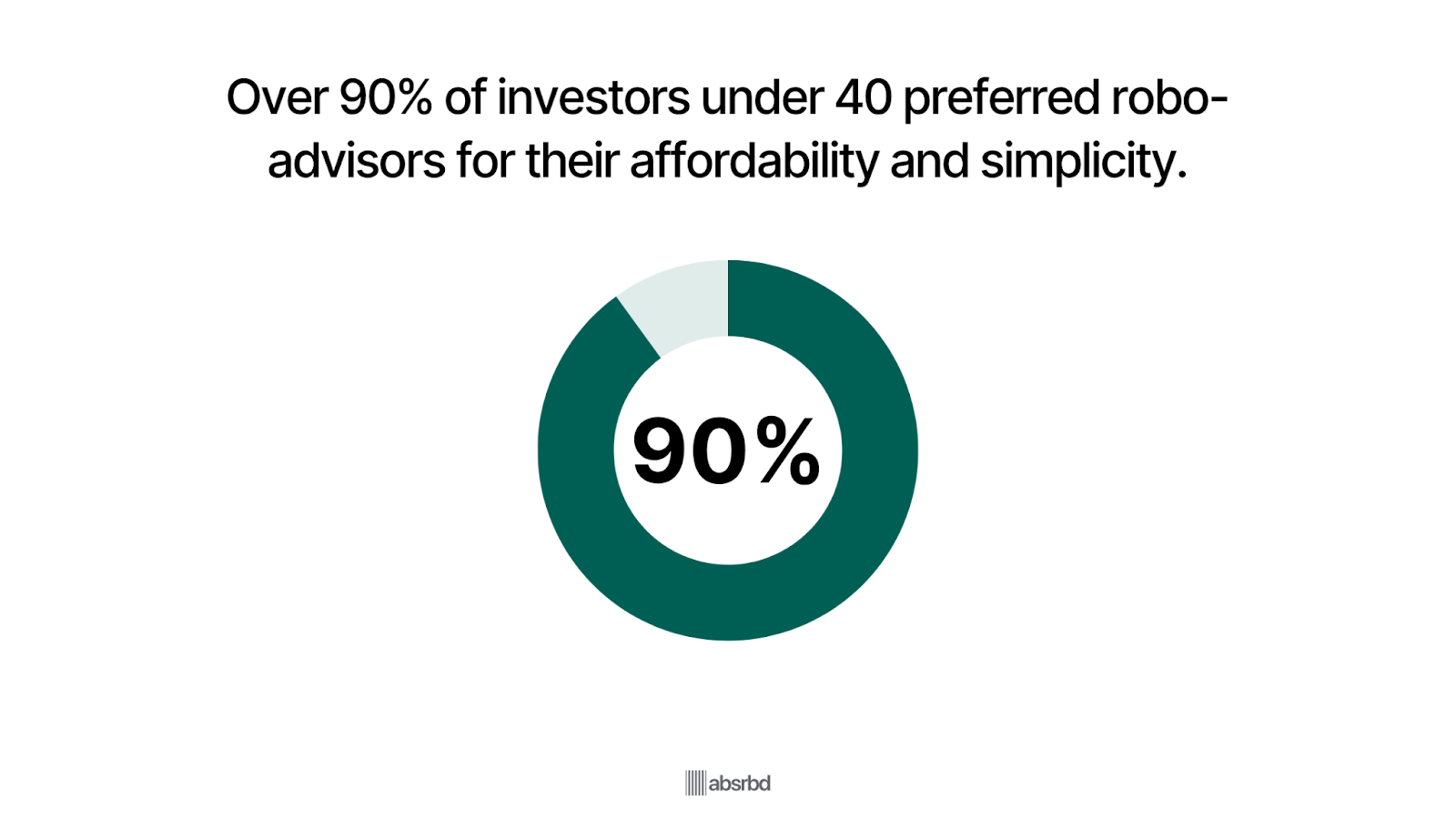

- More than 90% of users under 40 prefer robo-advisors due to their lower fees and ease of use in 2025. CoinLaw

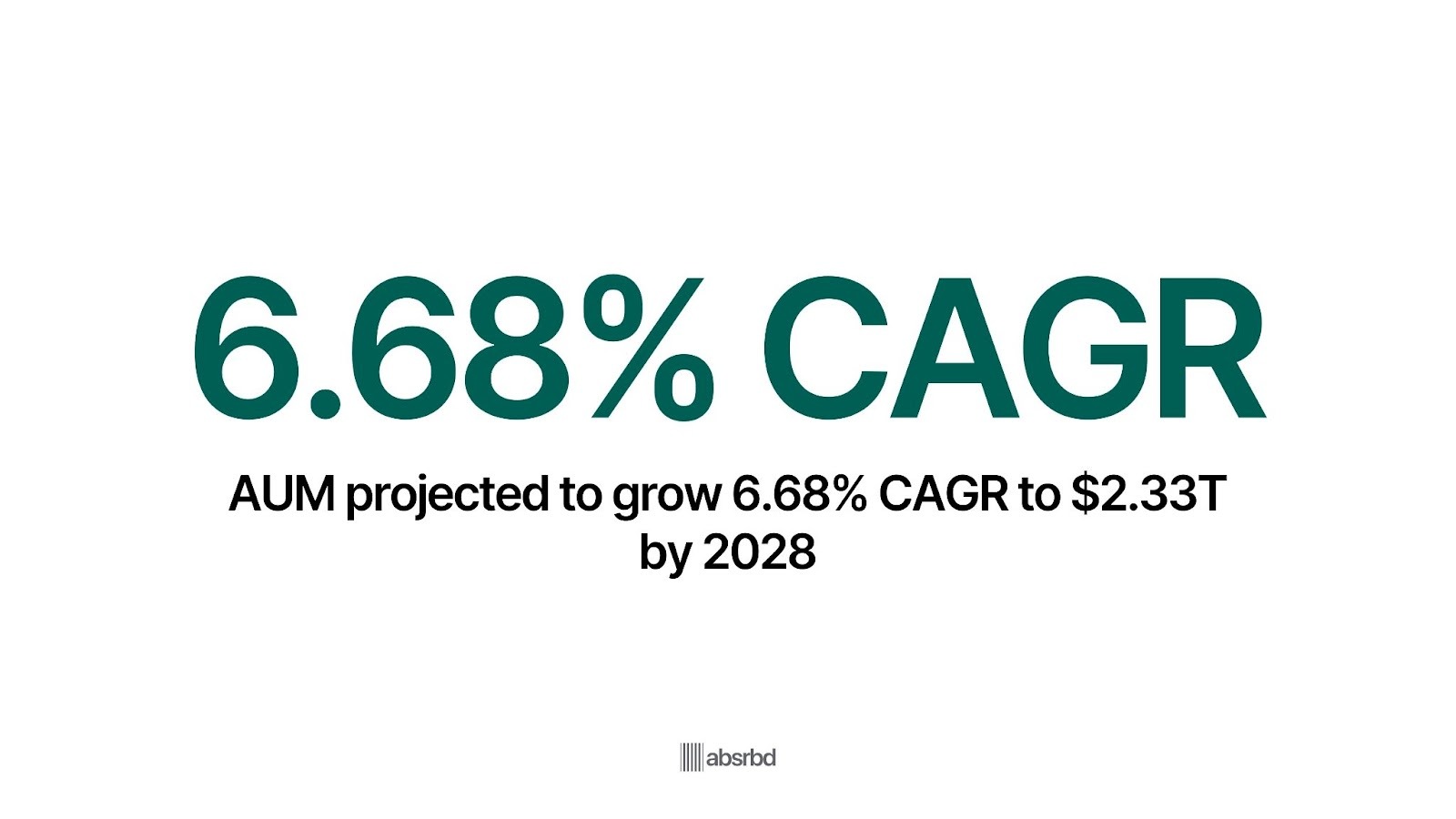

- Assets under management are expected to show an annual growth rate CAGR 2024-2028 of 6.68%, resulting in a projected total of $2.33 trillion by 2028. Statista

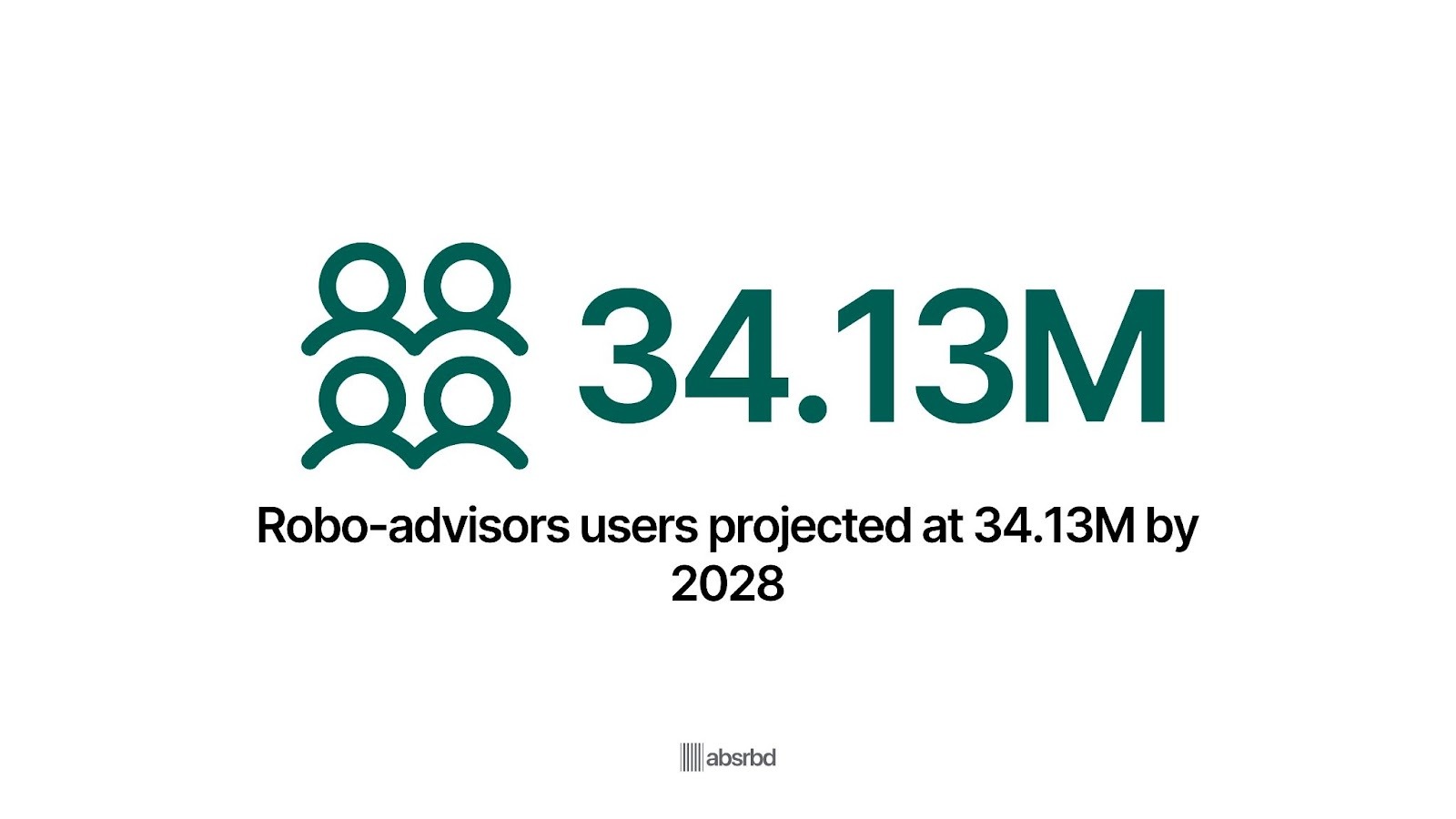

- In the Robo-Advisors market, the number of users is expected to amount to 34.130m users by 2028. Statista

- The United States takes the lead with the highest assets under management, projected to reach $1.46 trillion by 2024. Statista

- A survey by Investopedia states that 27% of male respondents use robo advisor versus 16% of women.

Key Trends

Robo-advisors are increasingly leveraging artificial intelligence, personalized financial planning, and hybrid advisory models to offer more customized, cost-efficient, and accessible investment solutions.

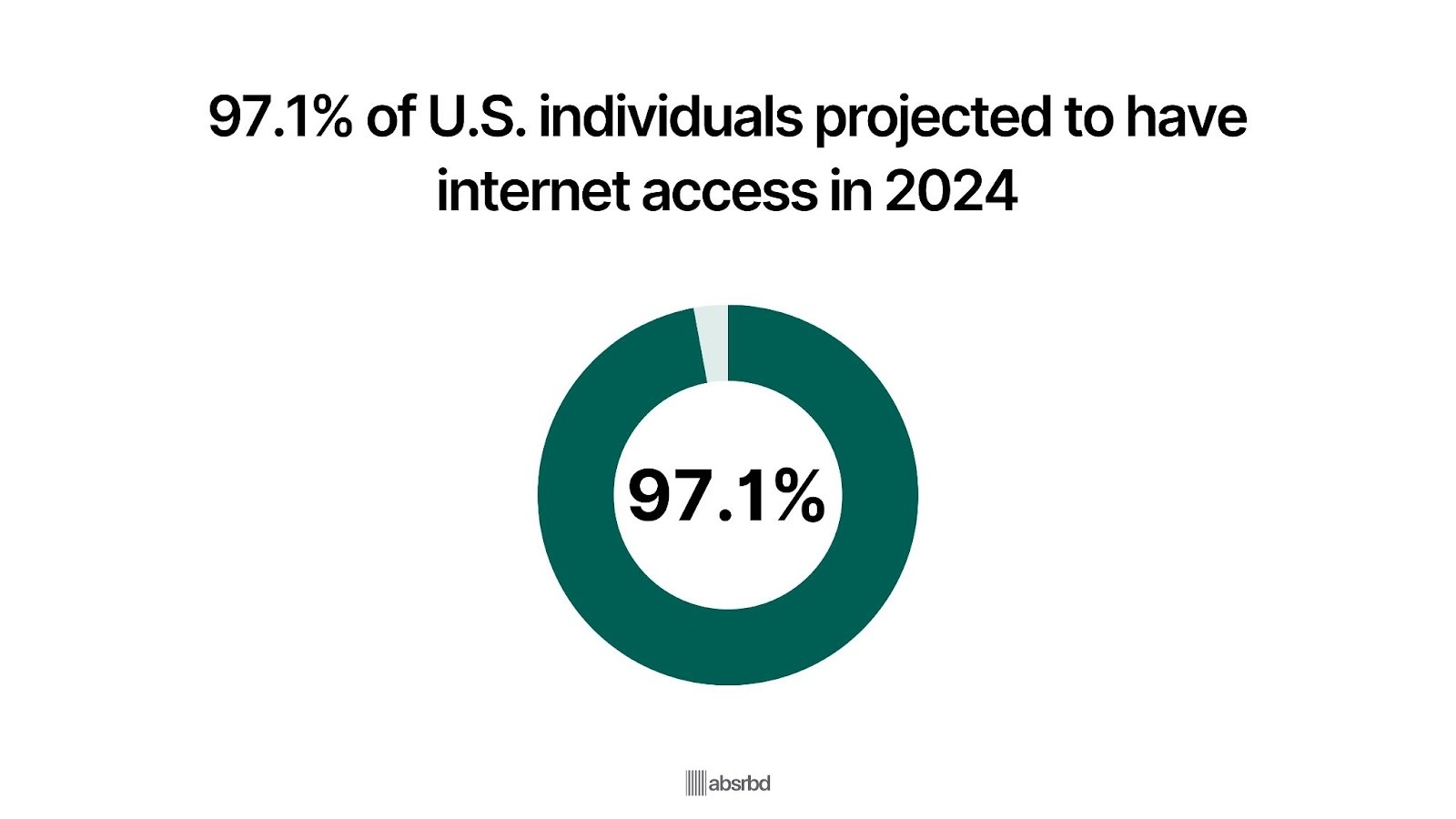

Increasing Internet Penetration With About 97.1% of Us Individuals Having Access to the Internet Data Report

The expansion of Internet connectivity has remarkably boosted the adoption of robo-advisors, with over 97.1% of US individuals accessing the Internet.

This shift is important because it democratizes financial advice, allowing individuals from various backgrounds to invest easily.

As a result, the robo-advisory market is projected to grow from $7.39 billion in 2023 to $72 billion by 2032, reflecting a compound annual growth rate CAGR of 28.8%. Polaris Market Research

This surge is driven by younger generations, particularly millennials and Gen Z, who prefer digital tools for financial management.

This highlights a shift in how financial services are consumed.

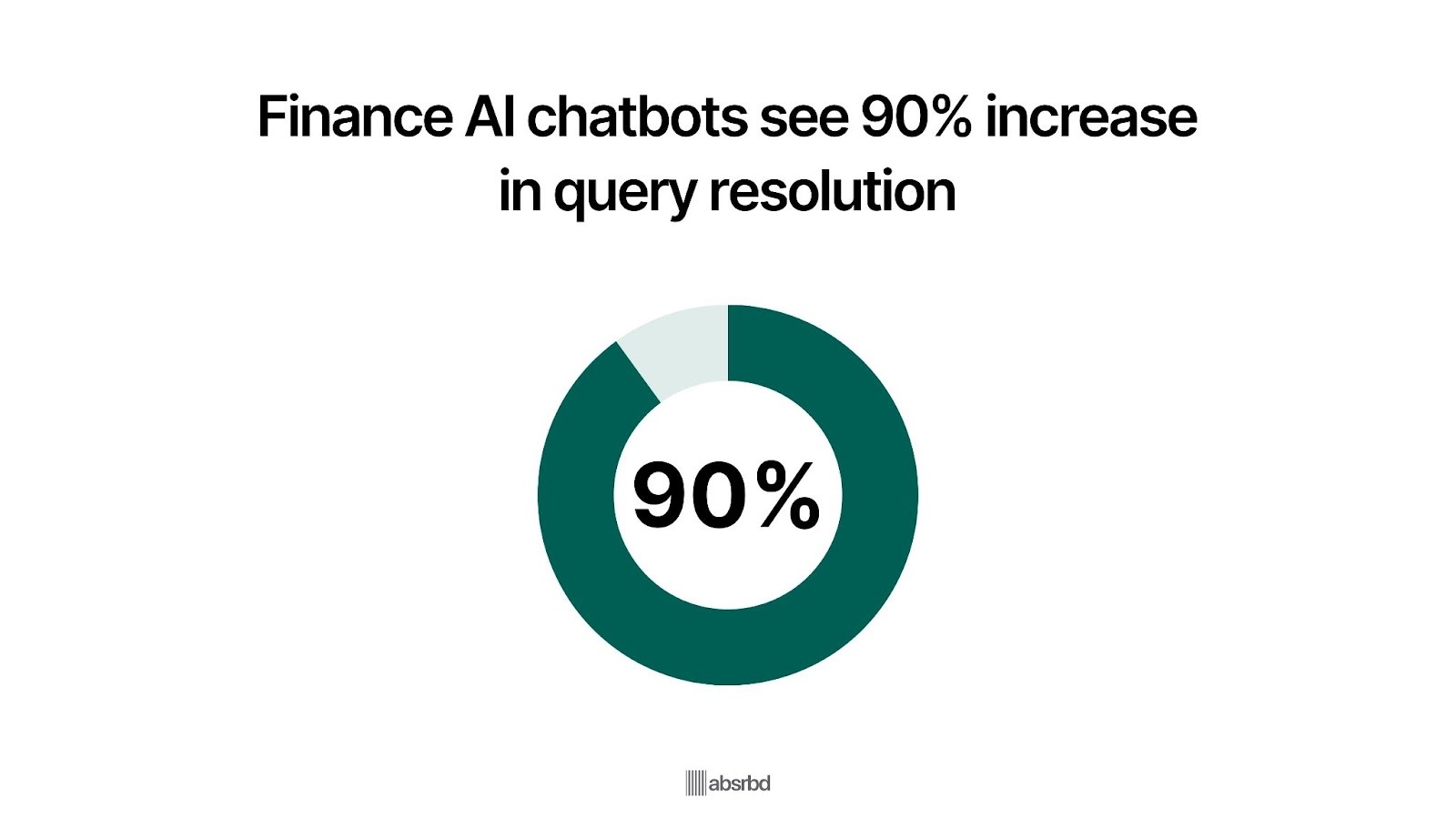

AI Chatbots in Finance Have Seen a 90% Increase in Customer Query Resolution Rates. Wifi Talent

The integration of AI and machine learning technologies is transforming the robo-advisor industry.

Robo-advisors now leverage sophisticated algorithms to analyze user data, providing personalized investment strategies that were previously the domain of human advisors.

This is crucial as it enhances the efficiency and accuracy of investment recommendations, making financial planning more accessible.

For instance, firms like Betterment and Wealthfront utilize AI to optimize portfolio management, leading to improved returns for users.

The market is expected to see an influx of AI-driven robo-advisors, with a notable increase in user engagement and satisfaction.

Hybrid Robo-Advisors Dominate the Market With 63.8% of the Global Revenue of Robo-Advisor Grand View research

The rise of hybrid robo-advisors, which combine automated services with human oversight, is reshaping the industry.

This caters to investors who seek the efficiency of automation but still value human interaction for complex financial decisions.

The hybrid model has gained traction, accounting for a large portion of the market share, as it addresses the limitations of fully automated services.

For example, Vanguard has successfully integrated human advisors into its robo-advisory platform, resulting in enhanced customer trust and retention.

This development reflects a broader trend of personalization in financial services, appealing to a diverse clientele.

Maturation of the Market, With the Global Market Reaching 7.39 Billion as of 2023 Polaris Market Research

As the robo-advisor industry matures, it is witnessing consolidation and the exit of less competitive firms.

Reports indicate that the industry surpassed $1 trillion in assets under management by late 2023, signaling its growth and stability. Statista

This maturation is important as it indicates a shift from rapid expansion to a more competitive environment, where firms must differentiate themselves through service quality and innovation.

For example, Goldman Sachs and JP Morgan Chase have exited the retail robo-advice space, emphasizing the challenges of maintaining profitability in a low-cost environment.

This trend highlights the need for robo-advisors to adapt their business models to sustain growth and meet changing consumer expectations.

Key Challenges Facing the Robo-Advisory Industry

The robo-advisory industry faces several key challenges that hinder its growth and effectiveness.

These challenges include regulatory compliance, personalization, data management, and competition with traditional financial advisors.

Regulatory Compliance

Robo-advisors must navigate a complex framework of regulations that vary by jurisdiction.

Compliance with fiduciary duties, anti-money laundering laws, and data protection regulations is essential.

For instance, the financial sector is heavily regulated, and robo-advisors must ensure their algorithms align with these standards.

A Deloitte report highlights that as robo-advisors grow, they face increasing regulatory scrutiny, which can complicate their operational frameworks and increase costs.

Personalization of Services

Despite robo-advisors' initial promise of tailor-made investment strategies, many platforms struggle to meet the growing demand for personalized services.

Investors increasingly expect solutions that cater to their unique financial goals and risk appetites.

A study by Investopedia indicated that while robo-advisors offer low fees and convenience, they often fail to deliver the nuanced, empathetic support that traditional advisors provide.

This disconnect can lead to low customer satisfaction and retention rates.

Data Management and Security

Data is at the core of robo-advisory services, yet managing and securing this data presents critical challenges.

Robo-advisors must ensure the accuracy and security of the data they collect, as breaches can undermine customer trust.

The need for robust data governance and compliance with privacy laws is paramount.

A report noted that the quality and security of data are critical for building user confidence, as clients are increasingly concerned about how their sensitive information is handled. Deloitte

Competition With Traditional Advisors

Robo-advisors face stiff competition from established financial institutions that offer hybrid models combining digital and human advisory services.

Traditional firms have the advantage of established trust and a broader range of services. For example, firms like Vanguard and Schwab have integrated robo-advisory features into their offerings, making it challenging for standalone robo-advisors to attract and retain clients.

Emerging Opportunities in Robo-Advisory

Growing demand for automated wealth management in emerging markets, integration with ESG investing, and AI-driven portfolio optimization are creating new opportunities for innovation and expansion in robo-advisory services.

Hybrid Robo-Advisors

Blending human financial advisors with AI-driven robo-advisors.

The hybrid robo-advisor market is expected to grow progressively, reaching $16 trillion in assets under management AUM by 2030. Deloitte

Companies like Vanguard Personal Advisor Services and Schwab Intelligent Portfolios offer clients a combination of automated services with access to human and financial advisors, catering to those who prefer some human touch in their investment strategies.

Personalized Investment Portfolios

Increasing demand for highly personalized investment portfolios using AI-driven analytics.

67% of North American and European eCommerce companies plan on investing more in personalization. Statista

Robo-advisors like Wealthfront are introducing tailored portfolios based on users' financial goals, risk tolerance, and even personal values, such as ESG Environmental, Social, and Governance investments.

Global Expansion

Increasing adoption of robo-advisors in emerging markets outside North America and Europe.

The global robo-advisor market asset under management is expected to reach 2.23 trillion by 2027, driven by expansion into Asia-Pacific and Latin American markets. Statista

Companies like StashAway and Syfe are expanding robo-advisory services across Southeast Asia, capitalizing on the growing demand for digital financial services.

Robo-Advisors for Niche Markets

Catering to specific demographics or investment preferences e.g., sustainable investing, women-focused platforms.

Sustainable investing via robo-advisors will surpass $50 billion in AUM by 2025. ARX

Ellevest, a robo-advisor focused on women investors, provides personalized portfolios to close gender wealth gaps, while platforms like OpenInvest focus on impact investing.

Impact on Stakeholders

Consumers:

- Robo-advisors make sophisticated portfolio management affordable and accessible to a wider range of individual investors, including those with smaller account balances.

- Robo-advisors use algorithms to provide customized investment recommendations and financial planning based on an individual's goals, risk tolerance, and investment timeline.

- Robo-advisor services typically have lower management fees than traditional human financial advisors, allowing consumers to keep more investment returns.

- Robo-advisors offer a seamless, online-based investment experience, enabling consumers to manage their finances anywhere with an internet connection.

Businesses:

- Traditional financial institutions are partnering with or developing their robo-advisor platforms, which allow them to offer automated investment services and generate additional revenue streams.

- The rise of robo-advisors has introduced new, tech-savvy competitors into the wealth management industry, forcing established firms to adapt their service offerings and pricing to remain competitive.

- The growth of robo-advisors has created a thriving market for fintech startups to develop innovative investment management solutions and disrupt the traditional financial services market.

Investors:

- Robo-advisors are making professional investment management accessible to a broader range of investors, including those with relatively small account balances.

- Robo-advisors use sophisticated algorithms to construct diversified portfolios and optimize asset allocation based on investors' risk profiles and financial goals.

- Robo-advisor platforms often give investors greater visibility into their portfolio holdings, performance, and fees, allowing for more informed decision-making.

- Robo-advisors' automated, data-driven approach may lead to improved investment outcomes compared to traditional human-based investment management, particularly for passive, long-term investors.

Regulators

- Regulators face challenges in evaluating robo-advisor platforms and determining how to assess their fiduciary responsibilities.

- Compliance with existing securities laws, such as SEC registration and FINRA regulations, is crucial for robo-advisors.

Conclusion

The trends in robo-advisor adoption have far-reaching implications for various stakeholders.

For individual investors, the growth of automated investment platforms has increased access to affordable, personalized financial management.

Meanwhile, traditional wealth management firms must contend with disrupting their business models as robo-advisors challenge the dominance of human financial advisors.

These shifts are driving a reevaluation of the investment management industry's value proposition and pricing structures.

As robo-advisors continue to gain momentum, leveraging sophisticated algorithms and data-driven insights, we're likely to see a further democratization of wealth management.

Investors of all income levels will have the opportunity to benefit from professional portfolio construction and optimization.

Moving forward, success in this space will hinge on the ability of robo-advisor providers to continuously enhance their technology, offer personalized financial planning, and maintain high levels of transparency and trust.

Robo-advisor platforms that seamlessly integrate with consumers' daily financial activities while delivering superior investment performance and a superior customer experience will be best positioned to thrive in the developing world of wealth management.

As the industry develops, the winners will be those who can strike the right balance between technology-driven efficiency and the human touch required to address the complex financial needs of diverse client segments.