111 NE 1st ST

Miami, Florida 33132

USA

While it’s no news that the venture capital (VC) investments hype years are over, the trends in the sector offer a glimmer of hope with the recent stabilization.

A timid recovery began in Q2 2024 with the AI boom and the mega deals it attracted, especially ($1 billion+) deals making up for the decline in number of deals, but with an uneven global rebound.

According to Finance Magnates, the U.S. dominated global venture capital activity in the first three quarters of 2024, with over 55% share of high-value deals totaling $48.4 billion.

In this article, we’ll explore the trends shaping the venture capital sector in 2024, comparing North America, the global VC giant, with its distant but closest rival in the Asian Pacific region.

Data Sources and Methodology

This article combines open-access resources and proprietary data to present accurate, up-to-date statistics and relevant developments in the VC landscape.

Our methodology involves:

- Aggregating data from government databases, industry reports, and academic publications

- Incorporating exclusive insights from leading industry providers

- Regular updates to reflect the latest information

Key data providers include:

While we strive for accuracy, trends in the venture capital space are shifting rapidly.

These statistics reflect current patterns and should not be considered permanent facts.

Key Takeaways

- Asian funds return 40% less than their U.S. counterparts despite its rapidly growing ecosystem. (Wellington Management)

- Asian unicorn (startup worth $1 billion or more) list reached 594 this year, up from just nine in 2014.

- Globally, AI startups reached close to $19 billion, accounting for 28% of all venture dollars in Q3, 2024.

- In Q3, there were 479 M&A deals globally for VC-backed startups with 70 involving AI-related startups.

Venture Capital Trends: Asia VS North America

Despite Asia’s rapidly growing ecosystem, the performance of Asian venture capital and private equity funds has generally lagged behind their Western counterparts.

Although the global venture market saw a small uptick from Q1 of 2024, the Asia region continued to see declines in startup funding as late-stage and growth rounds remained dormant.

Here are the major trends in the 2024 VC market:

Capitalization

The surge in capital availability across Asia's venture ecosystem in 2024 presents a double-edged sword for startups.

For instance, a startup valued at $500 million after raising $250 million would need to reach a valuation of US$1.5 billion to ensure a successful IPO with sufficient float for its shareholders.

Whereas a company with a leaner capital table would have a much easier path to listing, even at the $500 million valuation. (Wellington)

The Asian capital influx, particularly from sovereign wealth funds and family offices, has led to a "growth at all costs" mindset among some startups, with burn rates in Asian tech companies averaging 2.3x higher than their North American counterparts. (Startup Genome)

In 2023, venture capital funding in Asia reached approximately $78.1 billion, despite a notable decrease from previous years, indicating a volatile but resilient investment environment. (Crunchbase News)

Many Asian VC funds may overestimate potential investment outcomes, leading to overcapitalization of startups.

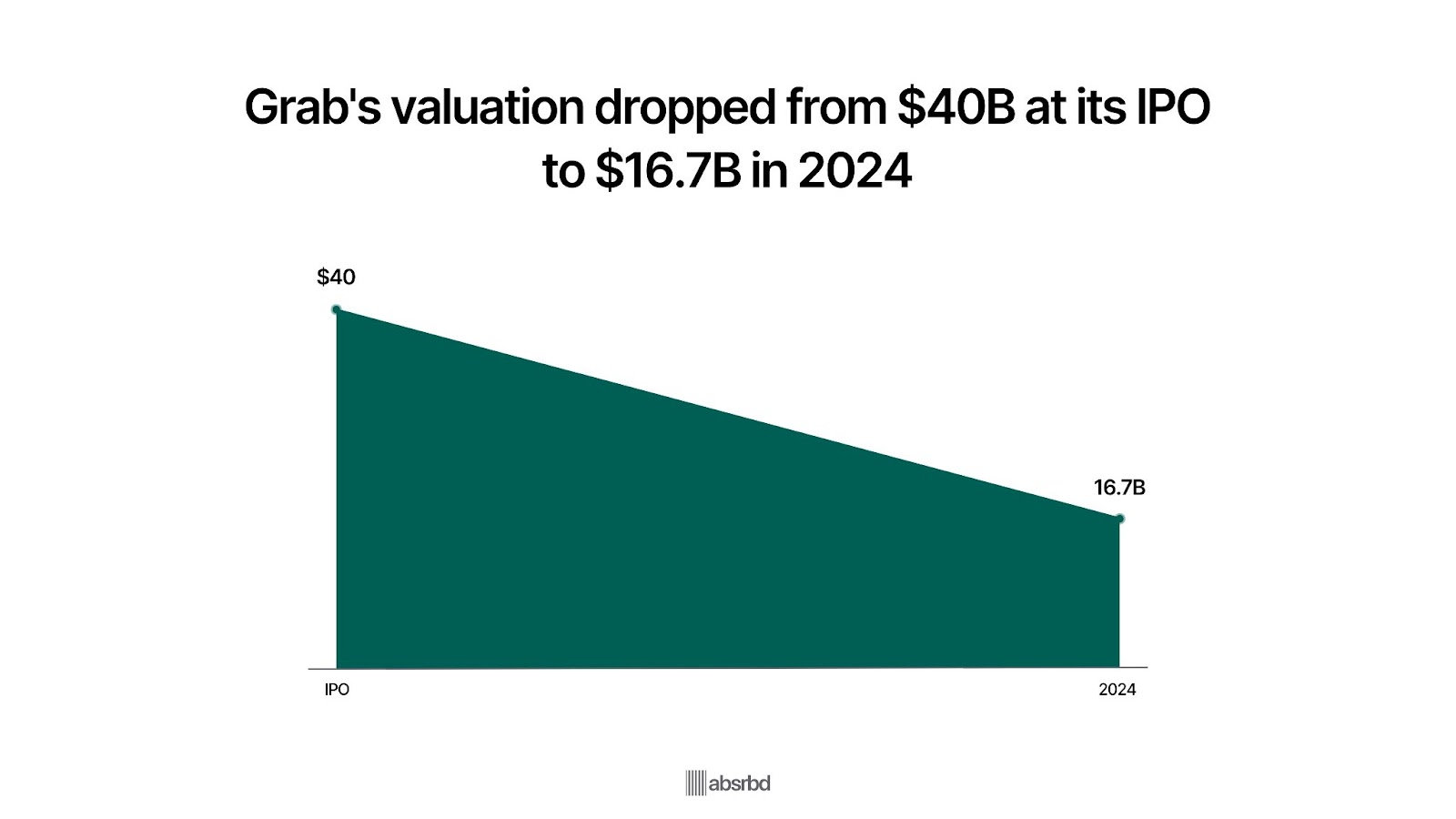

I should refrain from speculating about future outcomes, but the data indicates a stark contrast between overcapitalized Asian startups like Grab and North America’s Tesla.

Grab fell from a $40 billion IPO valuation to $16.7 billion in 2024, compared to the sustainable growth recorded by Tesla, which expanded from $2.2 billion to $1 trillion over the same period.

This mirrors the "too much water drowns the plant" principle, as evidenced by the higher failure rate among over-capitalized Asian startups versus those with moderate funding.

Scalability and Global Expansion

Historically, Asian funds have returned 40% less than their U.S. counterparts and 20% less than the European, despite its rapidly growing ecosystem. (Wellington Management)

The surge in available capital has been a driving force for innovation and entrepreneurship across Asia, fuelling the growth of 594 unicorns by 2024 from just nine in 2014.

Although some Asian companies are leaders in their respective regions, they often struggle to expand outside of them, resulting in smaller total addressable markets (TAMs).

Oftentimes, these startups face competition from global players even in their local markets, which in many cases limit or delay their market potential.

For example, Coupang and Amazon competed in the South Korean e-commerce market, though the former crushed Amazon in the region, we have not heard of or seen their impact outside of the region. (CNBC)

Scaling up in Asia generally takes longer, leading to extended times to liquidity events like an IPO and significantly affecting late-stage rounds.

According to Crunchbase News, Asia’s sinking venture funding fortunes remain late-stage growth rounds, in Q3 of 2024, such rounds totaled only $5.8 billion as against North America’s $23.8 billion across 246 rounds.

On the other hand, due to increased focus on scalability, the North American market saw a few large acquisitions announced during the quarter in sectors from cybersecurity to biotech.

Standouts include Recorded Future, a threat intelligence provider, acquired by Mastercard for $2.65 billion, Own Company, (a provider of data management tools) acquired by Salesforce for $1.9 billion and Nerio Therapeutics (drug discovery company) by Boehringer Ingelheim at $1.3 billion.

Asia’s Late-stage Rounds Struggle

Late-stage funding rounds are often intended to empower startups to scale, prepare for an IPO or acquisition, overcome challenges, and seize new market opportunities for growth and success.

But available data has shown that because of the inability of Asian startups to prioritize scalability, they often struggle to attract late-stage investment.

Despite the gold-rush-like investment in AI, VC dollars and the total number of deals in the region continue to drop quarter-over-quarter, from $18.9 billion across 2,305 deals in Q1 to $17.4 billion in Q2 and further decline to $13.2 billion in Q3 across 1,509 deals.

Reports from Crunchbase News show that while the AI buzz was ongoing in the U.S., with $16.8 billion in Q1, Asia, unlike every other region, struggled to attract only $2.5 billion.

Reports by Crunchbase News show that while early-stage startups in Asia received the biggest funding in Q1, 2024, with the total amount hitting $10.2 billion, (up 51% from Q4), late-stage and growth rounds made worse showing, with only $5.5 billion in 152 deals for the quarter.

By Q3, the late-stage growth rounds had not improved beyond $5.8 billion, making it the biggest culprit to Asia’s sinking venture funding fortunes.

North America on the other hand saw a total of $23.8 billion flow to late-stage and technology growth deals in Q3 of 2024 in a total of 246 rounds. (Crunchbase News)

However, early-stage investment saw a mild decline, with $13.5 billion in total funding which included a number of large early-stage deals.

In total, investors put $40.5 billion into startups across all stages in Q3 Known round counts across all stages totaled around 2,065 for the quarter. (Crunchbase News)

Mega Deals: Lazada $1.96B vs OpenAi $6.6B

Total venture funding in the Asia Pacific region fell to $17.3 billion in Q1, a drop of 4% from Q4 2023 and an 8% decline YoY, while the North American counterpart saw a total of $35.2 billion in Q1 of 2024.

The increasing number of startups in the Asian region leads to a corresponding increase in early-stage rounds but most of these startups end up remaining local champions which affects the number and value of late-stage and mega deals seen in the region.

Asian Pacific recorded a few $1 billion+ deals like $1.96 billion raised by Singapore-based Lazada, $1 billion raised by India-based Flipkart, $1.1 billion by China-based Zhiji Automobile, and $1 billion by Moonshot AI.

Mega-rounds were also down quarter over quarter in North America, according to Wtw, the number of all deals valued at over $100 million has seen a gradual decline from 188 deals closed in Q4 of 2023 to 157 in Q3 of 2024.

However, the rise in total investment was largely due to mega deals like Amazon’s $4 billion investment in Anthropic in March, xAi’s $6 billion in May, Alphabet’s $5.6 billion July investment in Waymo, and OpenAi’s $6.6 billion in ChatGPT in October among many other $1 billion+ deals.

The region did, however, also see some more traditional, large late-stage venture rounds in Q3, bringing the number to about 20 within the last ten months.

AI Boom

Investors’ appetite for artificial intelligence deals stayed strong in Q3, with nearly $15 billion invested in the space in North America alone. (Crunchbase News)

About 70 M&A deals were announced involving AI-related startups last quarter, down just a smidge from the 75 deals in Q2. (Crunchbase News)

Globally, artificial intelligence startups reached close to $19 billion, or 28% of all venture dollars in the third quarter.

However, Asia’s AI venture market seems to be left behind — with artificial intelligence-related companies making up only 16% of that region’s startup funding in Q3 and only 17% in Q2 according to Crunchbase report.

This means that while funding to AI startups seems to be covering up several lapses in the global venture market, Asia is not getting that same benefit.

Exits

Of course, venture investors don’t only put money into startups, they expect to get returns when those companies mature and go public or get acquired.

For the global VC sector in North America, 2024 started with signs of life, with the IPO market welcoming a few splashy debuts and acquirers writing some sizable checks, offering a glimmer of optimism.

Initial Public Offerings (IPOs)

California-based Astera, a developer of data center connectivity technology, made its splashy debut first on March 20 with a market cap of more than $11 billion. (Crunchbase News)

Bicara Therapeutics, a developer of cancer therapies, went public in September at an initial valuation of $828 million. (Reuters)

Zenas BioPharma, a developer of immunology-based therapies, went public on the Nasdaq in September and had a recent market cap of around $681 million. (MarketWatch)

One standout was data security firm Rubrik, which went public on NYSE in April, raising $752 million at an initial valuation of $5.6 billion. (CNBC)

In the first three quarters of this year, 77 companies chose to list overseas—which included cross-border deals within the Americas, Asia-Pacific, and EMEIA regions. (EY)

Merger and Acquisition (M&A)

On the software M&A front, the largest deal was in Q2, with software investor Hg’s $3 billion purchase of auditing platform provider AuditBoard.

In Q3, credit card giant Mastercard agreed to buy threat intelligence company Recorded Future for $2.65 billion and Salesforce bought data management tools developer Own Company for around $1.9 billion.

For biotech, Q2’s biggest acquisition was Merck’s acquisition of EyeBio, a developer of treatments for eye diseases, for $1.3 billion upfront and up to $1.7 billion in milestone-based payments. (Merck)

Conclusion

Despite the sovereign wealth capital flow to the Asian startups and the political tensions between China and the U.S., the region still lagged behind in their expected contribution to the global VC market.

Looking closely, overcapitalization may have been more poisonous to the region’s economic growth due to the lack of scalability and global expansion in the startup sector.

Consequently, investors fear putting money in late-stage rounds which impacts mega deals and stunts global expansion, making the businesses remain largely domesticated.

The need for global focus has never been more profound in the region than now.